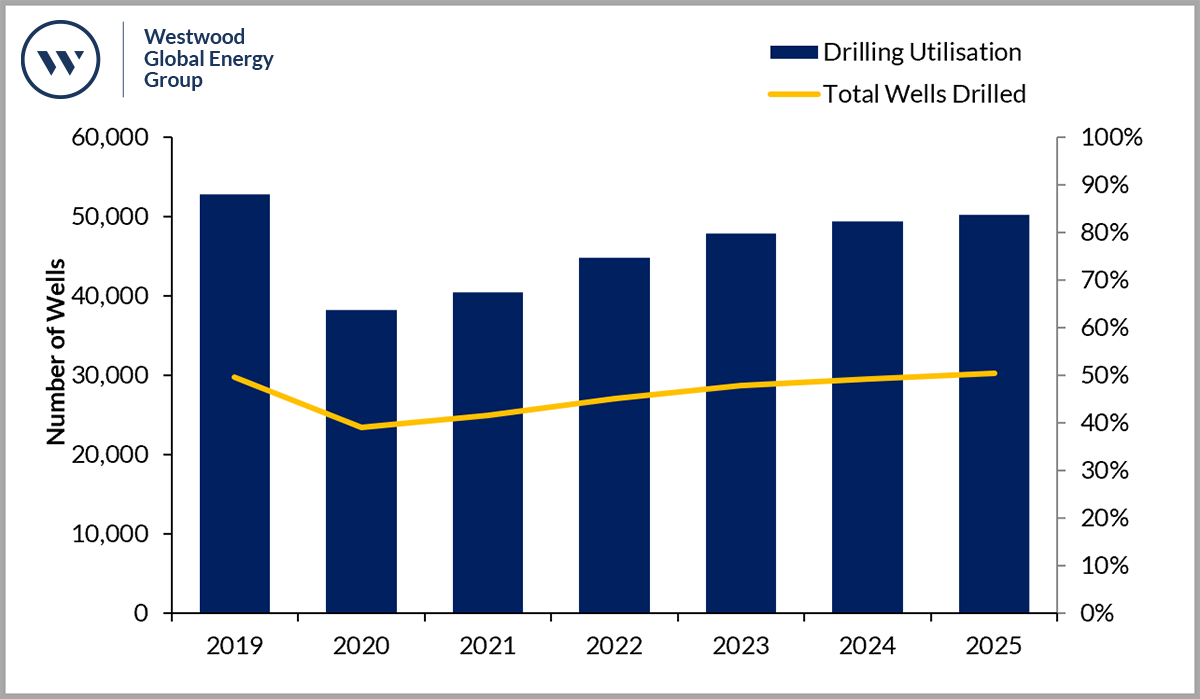

2020 was a catastrophic year for rig demand, with drilling activity plummeting across the globe and reversing the improvement in activity levels witnessed following the previous downturn. Overall, the number of operational rigs is estimated to have fallen c. 25%, contracting from c. 4,570 units to c. 3,530 one year later. This drop in drilling activity caused utilisation levels to fall to an estimated c. 40%, similar to levels seen at the low point of the previous downturn (2016).

In this tenth edition of the ‘World Land Drilling Rig Market Forecast’ report, Westwood assesses the current landscape of the industry following such a catastrophic downturn and provides an outlook on future onshore rig demand. Overall, the outlook for land rigs is starting to improve as stronger commodity prices (a function of strict OPEC+ cut quotas) spur increased drilling activity (from the lows of 2020). However, Westwood expects operators to remain cautious throughout the forecast 2021 – 2025 period, with industry fundamentals remaining sensitive to a number of factors (e.g. demand recovery, the Energy Transition, geopolitics etc.).

The report presents Westwood’s in-depth outlook for the global land drilling rig market over the 2021-2025 period, with a focus on addressing the following key questions:

- What is the market outlook, in terms of the volume of rigs operational and rig utilisation, across different regions and countries? Specifically, which jurisdictions are likely to drive demand for rigs in the coming years, and the underlying drivers.

- What are the key factors worth highlighting within specific countries or regions –basins, plays, E&P companies, national production targets (if appropriate)?

- What does the competitive landscape look like within specific markets –key rig contractors and the size and horsepower distribution of their fleet?

- What are the potential upsides to our forecast – regions, countries and drivers?

Wells Drilled and Drilling Utilisation, 2019-2025

1. Introduction

1.1.1 Oil Prices

1.1.2 Select E&P Company 2021 Capex Outlook

1.1.3 Upstream Access to Capital Markets

1.1.4 Energy Transition and Net Zero Ambitions

2. Global Analysis

2.1 Global Outlook

2.2 Regional Rig Fleets

3. Asia-Pacific Analysis

3.1 Asia-Pacific Rig Supply and Demand

3.2 Asia-Pacific Identified Rigs

3.3 Australia

3.4 China

3.5 India

3.5 Indonesia

3.6 Pakistan

3.7 Thailand

4. Eastern Europe & FSU Analysis

4.1 Eastern Europe Rig Supply and Demand

4.2 Eastern Europe & FSU Identified Rigs

4.3 Azerbaijan

4.4 Kazakhstan

4.5 Russia

5. Latin America Analysis

5.1 Latin America Supply and Demand

5.2 Latin America Identified Rigs

5.3 Argentina

5.4 Brazil

5.5 Colombia

5.6 Ecuador

5.7 Mexico

5.8 Peru

6. MENA Analysis

6.1 MENA Rig Supply and Demand

6.2 MENA Identified Rigs

6.3 Algeria

6.4 Egypt

6.5 Iraq

6.6 Kuwait

6.7 Oman

6.8 Saudi Arabia

6.9 United Arab Emirates

7. North America Analysis

7.1 North America Rig Supply and Demand

7.2 North America Identified Rigs

7.3 Canada

7.4 USA

8. Sub-Saharan Analysis

8.1 Sub-Saharan Rig Supply and Demand

8.2 Sub-Saharan Identified Rigs

8.3 Chad

8.4 Gabon

8.5 Nigeria

9. Western Europe Analysis

9.1 Western Europe Rig Supply and Demand

9.2 Western Europe Identified Rigs

10. Conclusions

Appendices

Appendix 1: Methodology

Appendix 2: Rig Equipment Landscape

Appendix 3: Glossary

Please contact our Sales team for more information and questions regarding the report.