Hosting the World Cup finals was always going to be a challenging and expensive endeavour for Qatar. When the finals begin in November 2022, the country will have invested more than $100 billion on infrastructure projects, ranging from power to stadia to sewage, and many others.

Hosting the World Cup finals was always going to be a challenging and expensive endeavour for Qatar. When the finals begin in November 2022, the country will have invested more than $100 billion on infrastructure projects, ranging from power to stadia to sewage, and many others.

Among the more complex investments has been the Barzan sour gas development, where the largest clad pipe in the world will be installed over the next 18 months. Originally scheduled to be onstream in 2013, the combined offshore and onshore development targeting the supergiant North Field has suffered badly leaking pipelines, forcing Qatar Petroleum (QP) to re-tender the $1 billion contract and pushing project completion back to early 2020.

In December 2017, the 90 kilotons of clad pipe were awarded to Germany’s EEW and Eisenbau Krämer mills, disappointing established producers in Japan and elsewhere. Original EPCI contractors Hyundai Heavy Industries were replaced with Europe’s Saipem and the first shipments of clad pipe left Germany earlier this month. QP and partners ExxonMobil will be closely monitoring how the pipe handles the sour gas, 20% of which is estimated to be Hydrogen Sulphide.

German capacity grows, clad plate brought into focus

By securing the Barzan contract, Eisenbau Krämer and EEW have expanded the clad pipe market share of German mills to over 50%, alongside their more established peer, Butting. Both mills will surely benefit from having a successful Barzan project on their resumé, and both are expected to compete more strongly for oil & gas pipe contracts after the Barzan project is complete.

The impact of a more active German presence will be felt beyond the clad pipe market itself. Unlike the world’s largest clad pipe producer, JSW, none of the German mills are fully integrated, all therefore are required to purchase clad plates prior to pipe rolling. As a sector with few major manufacturers that focus on oil & gas applications, the outlook for the larger clad plate suppliers appears positive.

Price outlook directed by Barzan

A project requiring 90 kilotons of clad pipe has a direct impact on prevailing prices, particularly relating to the Nickel grade 825 required and wider group of high Nickel materials.

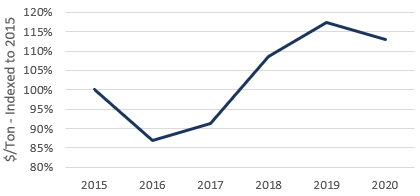

Figure 1: Nickel Clad Pipe Price ($/Ton, FOB – Indexed to 2015 Price) Source: Metal Bulletin Research, Westwood Global Energy Group

With both contracted mills operating a high base load and a reduced ability to compete for multiple upcoming opportunities, the per ton price of Nickel clad pipe has grown smartly and is expected to reach c.117% of the 2015 price in mid-2019, exceeding 2014 levels. Nickel lined pipe and clad plate prices similarly benefit from tightness in the clad pipe market offering suppliers a rare opportunity to return pricing pressure to project operators.

Clad pipe here to stay

The clad pipe manufacturing sector has remained remarkably resilient throughout the oil price downturn – supported by a diversity of product applications and the awarding of major projects, most notably Barzan. Benefiting from the twin value proposition of reducing costs compared to solid CRA material and maintaining key resistance attributes, customers appear to be gaining confidence in commercial benefits of the technology.

The World Cup finals in Qatar relies on additional sources of power and electricity coming onstream prior to the tournament in 2022. In the case of the largest clad pipe contract in the world, unlike in Russia 2018, the Germans have already won.

Westwood Global Energy, alongside Metal Bulletin Research, will launch a new study exploring the global corrosion resistant alloy sector in July, with a focus on clad & lined pipe.

Matt Loffman, Associate Director, Energy Analytics

[email protected] or +44 (0)20 3794 5393