Since Westwood’s last Asia Pacific (APAC) offshore drilling rig insight, the market – as predicted – has reached utilisation levels not seen since the oil price crash of 2014 and dayrates have gone up across most rig types. Due to prolonged procurement processes, there has been a series of missed opportunities for operators to secure rigs at lower dayrates. Units continue to leave the region for greener pastures other than the Middle East. Additionally, utilisation and dayrates have gone up significantly, despite Brent Crude oil price decreasing ~25% between May 2022 and May 2023.

Supply shrinking and newbuilds unlikely in near term

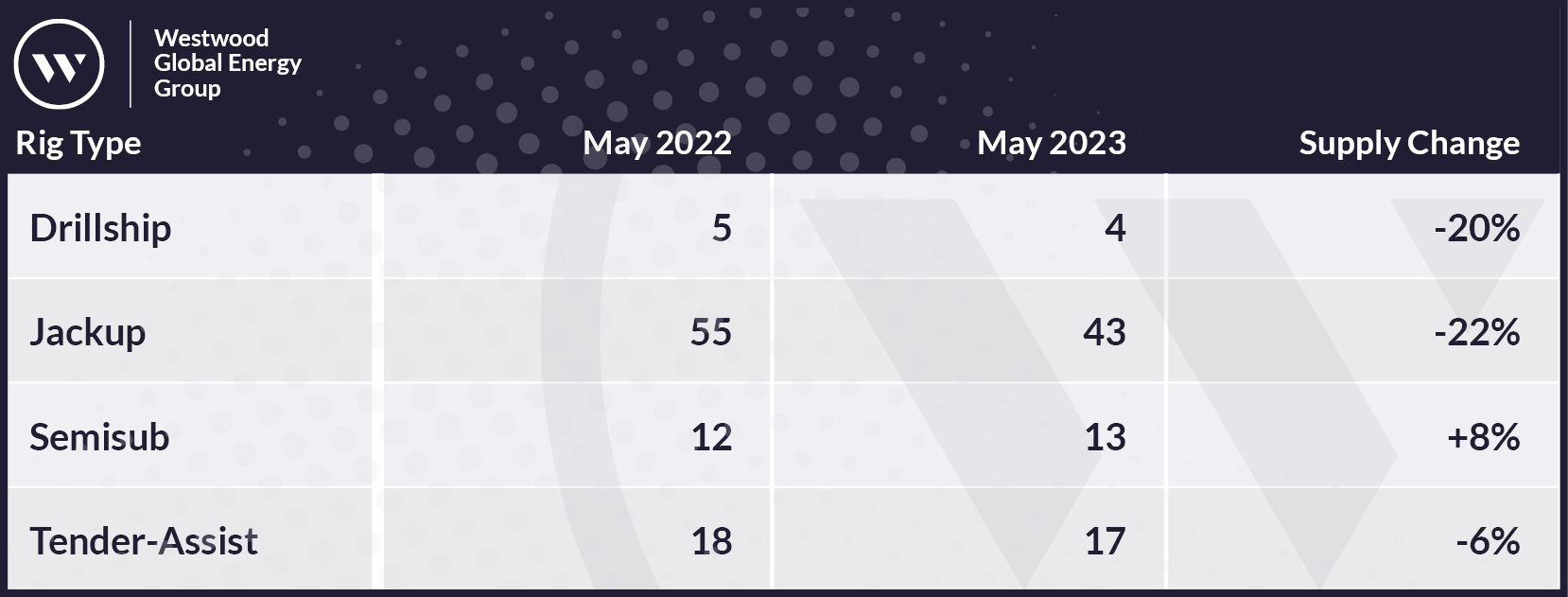

Supply across the fleet has shrunk year-on-year, especially within the jackup, drillship and tender-assist rig segments where 14 units in total have exited the region. Semisubmersibles (semis) recorded a slight increase of just one more rig than in the same period last year.

APAC Offshore Rig Supply Changes May 2022 Vs May 2023

Source: Westwood RigLogix

The exodus of jackups to the Middle East has slowed but is not quite over. In Singapore, only six jackups remain (Admarine 687, Admarine 689, Arabdrill 150, Tivar, Heidrun and Huldra) all bound for the Persian Gulf.

Prospects for rig construction often loom when availability becomes limited, however this time there are several factors preventing a mad rush of orders, as seen in the last industry upturn. Financing is likely be more difficult to obtain as banks and financial institutions distance themselves from fossil fuel-related investments. Construction costs may be prohibitive as the expected return on investment is not what it used to be. Rig builders will be looking for favourable payment terms so that in the event of a crash, they are not left with massive debts and more stranded assets. As of January, there were still 19 jackups, four semis, five drillships and four tender-assist rigs available in Chinese shipyards for those that may be looking.

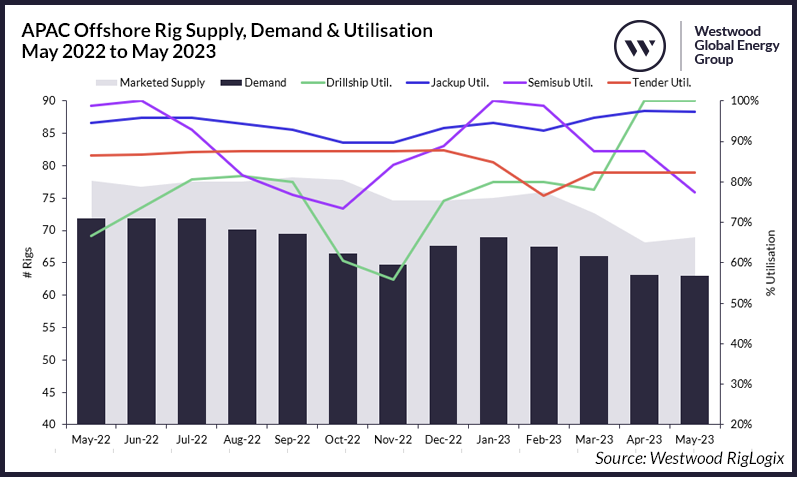

APAC Offshore Rig Supply, Demand & Utilisation May 2022-May 2023

Source: Westwood RigLogix

This lower supply, especially in the jackup and drillship segments, has aided utilisation recovery across most rig types over the year. The jackup segment is now close to sold out at 97%, while drillships are fully utilised. Tender-assist utilisation dropped five percentage points year-on-year, while increased supply and lower demand in the semi segment has resulted in decreased utilisation of around 22 percentage points compared with a year earlier.

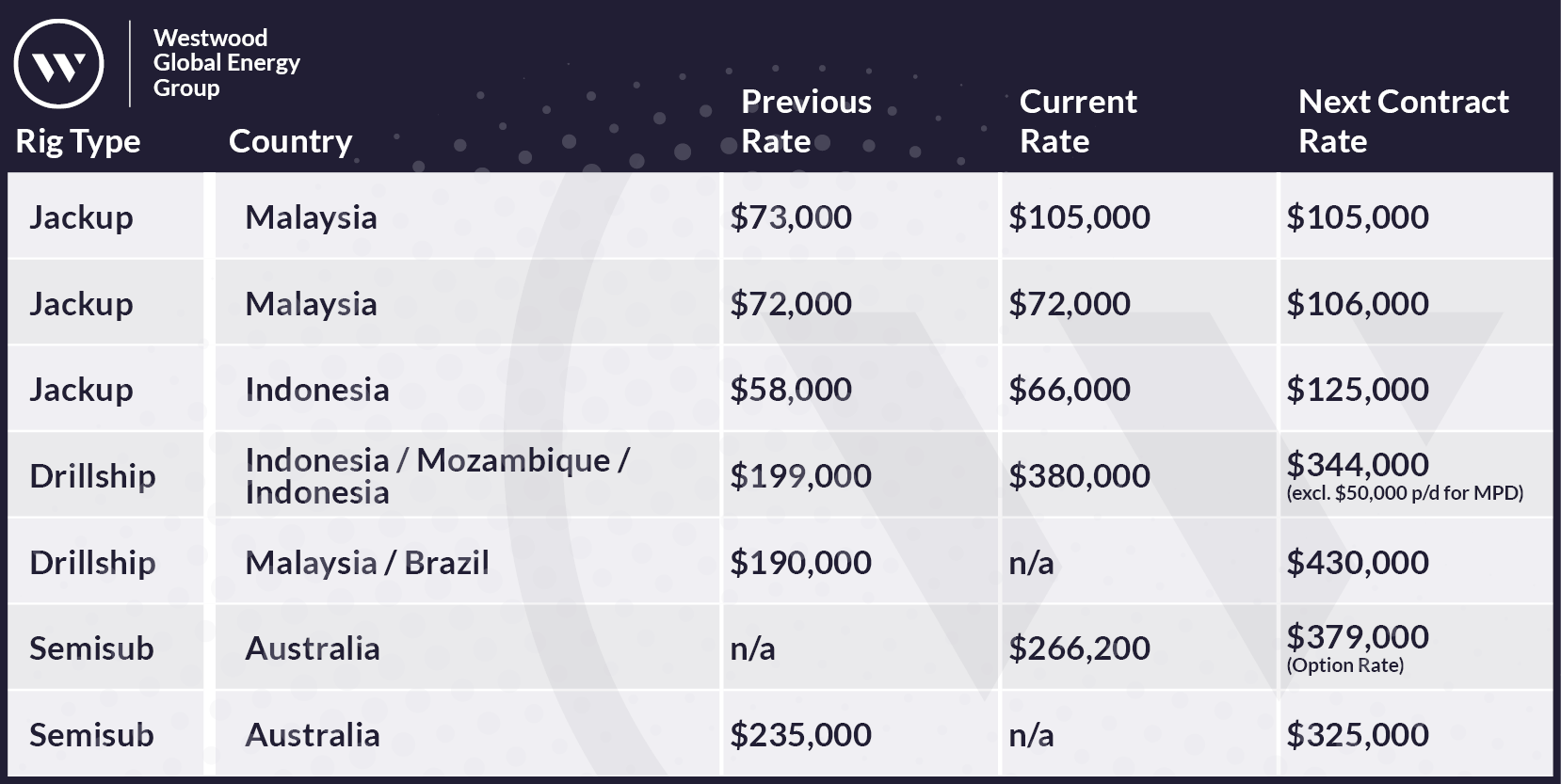

Off the back of higher utilisation as well as ample outstanding demand, dayrates have been trending upward over the year. Rigs are typically being secured at higher rates than their previous commitments, as can be seen from a selection of fixtures made during the period in the table below. Jackups have been fixed at as much as $67,000 per day more than their previous or current deals, while one drillship was fixed at a whopping $240,000 per day more than its previous contract. Semis have also witnessed the same trend with new fixtures being secured at up to $113,000 per day more than prior deals.

APAC Sample Past, Present & Future Dayrates (Non-Exhaustive)

Source: Westwood RigLogix

Meanwhile, between May 2022 and May 2023, Westwood recorded a 10% increase in average rolling jackup dayrates, 28% increase in drillship dayrates and a 7% increase in tender-assist rig dayrates.

Contract award activity slows down

Another indicator that market dynamics have changed is reduced contract award activity. Between January 2022 and May 2022 there were 34 contract awards in the APAC region for all rig types, however for the same period in 2023 there have been only 13 awards. This reduced pace naturally occurs when there is less availability and operators want to lock in rigs on longer deals before prices rise further. National Oil Companies (NOCs) are known to set a ceiling price they will pay for different categories of rigs, and these are adjusted periodically. With such stringent parameters in place, contracts often cannot be awarded because the rate is higher than anticipated.

Future demand looks healthy but challenges remain

RigLogix currently holds a total of 21 requirements in Southeast Asia or Australia already at a tender stage, totalling over 14 years of potential demand. Of this total, 73% is for jackup campaigns and the remaining tenders out in the market are for semis. Included in these requirements are Petronas Carigali Indonesia and Pertamina OSES & ONWJ’s joint tender for a jackup. VietSovPetro is still searching for a jackup for an eight-month programme, scheduled to start in 3Q. Additionally, Petronas Carigali Malaysia requires a jackup to carry out plug and abandonment duties, starting between 3Q and 4Q, with an anticipated duration of 700 days. The operator is still evaluating proposals for its HPHT floater programme expected to commence in 4Q 2023.

Despite the favourable demand outlook, the challenge of rising costs persists. However, Westwood expects current utilisation levels to hold steady or rise further in the next 12 months. Dayrates have not plateaued just yet, but the push back on rates from operators will continue. In this environment, operators will be considering further rig sharing campaigns and more direct negotiations.

Paul Ezekiel, Senior Rig Analyst

[email protected]

If you are interested in a comprehensive review of Asia Pacific’s offshore drilling market every month, you can subscribe to Westwood’s Asia Pacific Offshore Report. For more information on how to access the report, click here or contact [email protected].