Upstream Investment Outlook Q1 2018 – The Outlook Following 12 Months of Change

The oil market has shifted dramatically over the last 12 months. Brent crude prices have hit levels not seen for over three years. OPEC has executed a successful and disciplined intervention, particularly so in the latter half of 2017.

Offshore ordering showed a particularly strong improvement through the year, with many high-profile projects being sanctioned. Westwood’s recent addition of Floating Production System (FPS) data into the SECTORS online platform highlights this, with a total of 15 new FPS orders being placed last year, compared to zero the year previous.

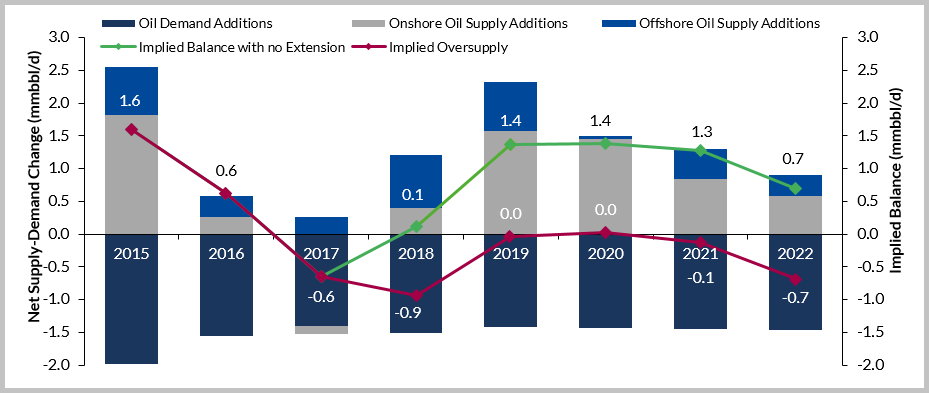

Oil Supply Demand Balance 2015-2022

Looking further forward however, the lack of sanctioning activity since the downturn will likely result in a shortfall in project executions early next decade. Current data suggests the oil market will transition into a sustained undersupply from 2021, which is likely to be met by high oil prices and a wave of new, fast-tracked projects being sanctioned. Despite electric vehicles, renewables and battery technologies having improved substantially in recent years, growth in these markets is unlikely to meet the oil supply shortfall.

Over the longer-term, however, threats from these technologies will only strengthen and the oil & gas market will have to continue to adapt, to a changing energy landscape.

Key Conclusions Include:

- A further -0.9 mmbbl/d oil market correction is expected in 2018.

- Saudi Arabia’s production strategy after the ~5% IPO of Saudi Aramco remains unclear.

- US shale production is already over 10mbpd and expected to hit 11mpd by 2019.

- A further 16 FPS units which are expected to be ordered this year, in addition to the one already ordered.

- Brent prices are outperforming industry consensus so far this year ($60/bbl 2018 average).

- $1.7tn of upstream Capex is expected over 2018-2022.

Westwood publishes the Upstream Investment Outlook on a quarterly basis, to provide its independent view on the current, and future, state of the upstream oil & gas market – to educate investors and guide businesses through the coming months and years.