Downstream maintenance expenditure returns to growth

As highlighted in the most recent edition of Westwood’s World Downstream Maintenance Market Forecast, significant price pressure during the oil price downturn has heavily impacted the downstream maintenance market. Global downstream maintenance spend bottomed out in 2016, after falling 26% compared to 2014 levels. Westwood believes that the downstream maintenance market is at the beginning of a recovery cycle. 2017 saw improvements which will be sustained over the forecast with year-on-year growth expected over 2018-2022.

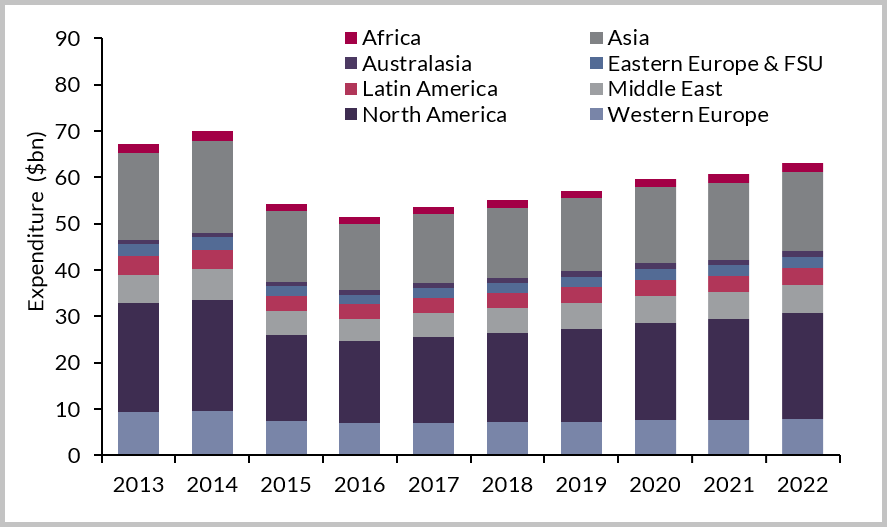

Global Downstream Maintenance Expenditure ($bn), 2013-2022

- Global downstream maintenance expenditure declined by 26% over 2014-2016.

- Westwood expects to see a recovery in the market in 2017, with global expenditure forecast to rise by 4% compared to 2016, reaching $54bn.

- Growth in the market is expected to be sustained over 2018-2022, with global expenditure forecast to rise at a 3.5% CAGR over the next five years.

- Petrochemical facilities will account for the largest proportion of downstream maintenance expenditure over 2018-2022, with a market share of 42%.

- The asset services sector is forecast to account for 72% of downstream maintenance expenditure over the next five years, with asset integrity representing the remaining 28% of the market.

- North America will continue to represent the largest share of the downstream maintenance market over 2018-2022, with regional expenditure over this period forecast to reach $105bn.

Westwood’s report features detailed analysis of the fundamental drivers for facility maintenance expenditure, including commodity prices, downstream facility population, refining margins, policies and regulations, as well as key trends influencing maintenance expenditure within the refining, gas processing, petrochemical, and LNG sectors. The report contains service line analysis for the downstream asset services and asset integrity markets, split out by service line, facility type, and region. Comprehensive regional analysis is also provided for Africa, Asia, Australasia, Eastern Europe & FSU, Latin America, Middle East, North America, and Western Europe, including an expenditure forecast by service line. The report is therefore essential for equipment providers, operations and maintenance contractors, and facility operators, in addition to government departments aiming to make more informed investment decisions.

With a large installed base, petrochemical facilities will continue to account for the largest proportion of expenditure over 2018-2022, despite having a lower maintenance cost per facility relative to refineries. The share of expenditure allocated to LNG facilities is set to increase through to 2022, with significant additional capacity forecast to come onstream in Asia, Australasia, and North America. North America accounted for the largest proportion of downstream maintenance expenditure over the hindcast, and will marginally increase its market share over 2018-2022. Large and ageing facilities are expected to support increased maintenance expenditure in order to sustain production levels and reduce downtime. A number of LNG export facilities within the region are also due to become operational, as the USA moves from being a net importer to a net exporter of natural gas. In the long-term, rising demand for refined products and natural gas, in line with population growth and economic development, in addition to an ageing population of assets, will act as robust long-term drivers for downstream maintenance expenditure.