Higher oil prices in the first half of 2022 and its impact on oil market fundamentals is already showing a material uptick in offshore exploration and production (E&P) investment and rig count. This will drive considerable demand for Offshore Support Vessels (OSVs) over the next two years, encouraging owners to reactivate their idle fleets.

Brent crude oil price hit $100/bbl in early 2022 – the first time since 2014 – and prices remain elevated driven by the tightening supply/demand for oil, which has been exacerbated by uncertainty around the Ukraine crisis. Higher oil prices are driving a bumper year for offshore investment, with upstream engineering, procurement and construction (EPC) spend projected to reach $75 billion for 2022, representing a massive 80% increase year-on-year. The Middle East will be the largest contributor with final investment decision (FID) on projects such as QatarEnergy’s North Field Expansion Phase 1 and Saudi Aramco’s Zuluf Incremental, followed by Latin America, for projects such as Shell’s Gato do Mato offshore Brazil.

Global rig count also continues to climb. Contracted jackups hit a six-year high, with effective utilisation, which excludes cold stacked rigs, reaching 82%. The Kingdom of Saudi Arabia (KSA) jackup market was already very robust, and drilling activity will ramp up further following Saudi Aramco’s tender for an additional 30 rigs to support aforementioned projects. Meanwhile, global drillship effective utilisation reached 79%, its highest level since 2014. Dayrates improved for this segment, largely underpinned by activity in the US Gulf of Mexico (GoM), where rates are now routinely in excess of $200,000/day. Bearing in mind it’s not exactly like-for-like since some of the higher US GoM rates have been associated with 20,000 psi deepwater drilling programmes.

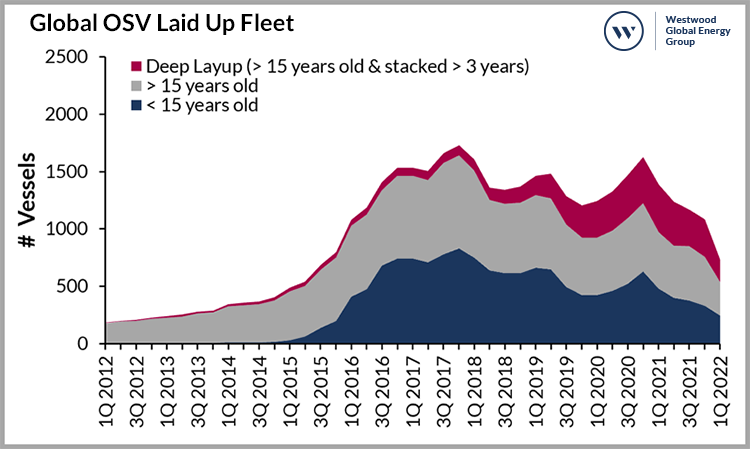

With oil prices settling above $100/bbl, vessel owners have been scrambling to reactivate their fleet to take advantage of the increased levels in offshore activity, especially following the surge of stacking that occurred during the pandemic. By the end of the first quarter, the total layup fleet fell by 32%, the lowest since 2016, with 321 vessels either reactivated, scrapped or written-off (i.e., considered commercially inactive).

Figure 1: Global OSV Laid Up Fleet

Source: Braemar ACM, Westwood Analysis

Only 33% of the current global laid up fleet consists of “premium” vessels i.e., those less than 15 years old. The majority (67%) of laid up OSVs are over 15 years old and essentially represent an ageing fleet. Many operators have age restrictions for their chartered tonnage and would not consider vessels of this age during the tendering process. OSVs in “deep layup” are over 15 years old and have been stacked for longer than three years. These are deemed highly unlikely to re-enter service and therefore not included in Westwood’s total utilisation calculation.

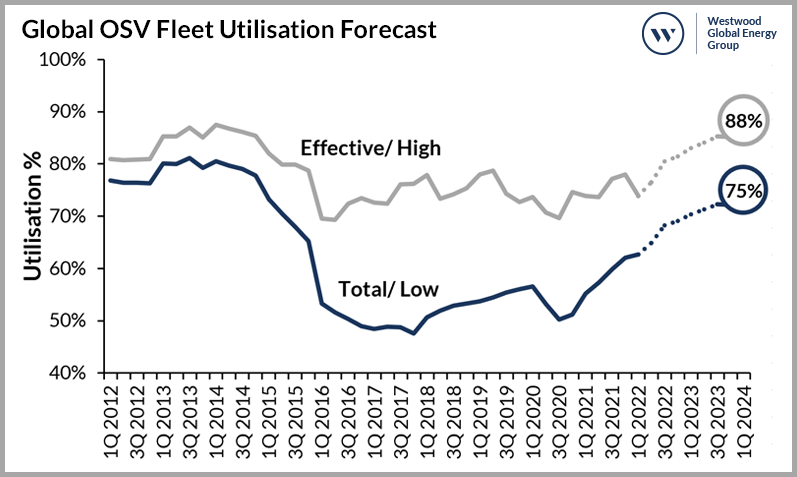

Utilisation forecast to hit 80% by 2024

The tightening global OSV market is driving improvements in utilisation. The Middle East in particular, has near 90% effective utilisation, likely resulting in a “sold out” market by the end of the year. There has been a significant uptick in rates for new tenders in the region, which in turn is encouraging mass reactivations as well as opportunistic sale and purchase (S&P) activity.

Total utilisation for the global OSV fleet currently stands at around 63%, which is a 7% increase from 2021. Effective utilisation had a quarter-on-quarter drop to 74%, which is not surprising given the sizeable number of reactivations registered during this period. The anticipated rise in rig demand is expected to see a sharp correction in this utilisation figure over the course of the year.

Figure 2: Global OSV Fleet Utilisation Forecast

Source: Braemar ACM, Westwood Analysis

Future utilisation will be contingent on continued fleet rationalisation. In Westwood’s low case scenario, which assumes no further scrapping, improved demand alone would increase utilisation to 75% by 2024. In the high case, utilisation could reach 88% should the entire laid up fleet be removed from the market. A mid-case outlook on the other hand, assuming scrapping of the >15-year-old laid up fleet, would result in 84% utilisation by 2024.

Growing demand, improved utilisation and higher dayrates, are all good indicators for vessel owners. Complying with local content, age restrictions and low emission requirements from operators, however, will put increasing pressure on owners with ageing fleets.

The total orderbook of registered International Maritime Organization (IMO) newbuilds now stands at 215, however only 67 are considered “Tier 1” vessels and likely to be delivered in the next 12-24 months. Further analysis shows that over the next two years, 430 vessels will pass the 15-year age mark and be considered “non-premium”. With only 67 vessels in the Tier 1 orderbook, this suggests that the premium fleet will shrink significantly over the next few years without substantial newbuild orders.

It wasn’t all that long ago there was a heavy oversupply issue in the OSV market, however the issue facing owners today is not the sheer number of OSVs but the age and quality of available tonnage and whether owners can raise the capital to invest in newer, cleaner vessels for future offshore operations as E&Ps continue to focus on age restrictions and lowering their overall emissions.

The Global Offshore Navigator is a collaborative quarterly market report written by Braemar ACM Shipbroking and Westwood Global Energy Group. For more information on how to access the full report click here.