8th January 2018

A ten year low in oil discoveries in Norway in 2017 doesn’t deter an expected increase in drilling in 2018, whilst performance continues to improve in the UK with the focus switching to gas for 2018.

In 2017, there was a shift towards high impact exploration drilling in both the UK and Norway. Norway saw a concerted effort of 10 exploration wells in the Arctic Barents Sea region and there were also five high impact tests in the UK North Sea, which is unusual for such a mature basin.

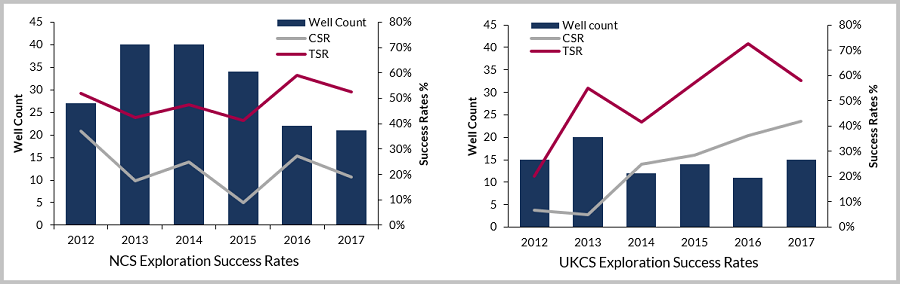

Results from these high impact prospects, testing prospective volumes greater than 100 million barrels of oil equivalent (boe) were disappointing, with just one commercial success so far announced in the UK with most likely resources of <100 million barrels. Despite this in the UK, high success rates in infrastructure-led exploration wells near production hubs in 2017 meant commercial success rates have now increased year-on-year since 2013 to reach over 40% with the highest oil volumes discovered since 2009, with three results still pending.

Commercial success rates in Norway and the UK, based on exploration wells that completed 2012 – 2017 with results known. Note three wells have results pending in the UK

Commercial success rates in Norway and the UK, based on exploration wells that completed 2012 – 2017 with results known. Note three wells have results pending in the UK

In Norway, drilling in the Barents Sea failed to make a single standalone commercial discovery and overall in Norway commercial success rates dropped to 20%, half that of the UK and the discovered commercial oil volume was at a 10-year low.

The level of drilling in the UK in 2018 is expected to be similar to 2017, with around 15 exploration wells planned and the high impact drilling programme switching focus to gas. Total unrisked pre-drill prospective resources for the UK are estimated by Westwood at 1 bnboe, of which c.750 million boe is gas. Exploration tests at the Lyon gas prospect West of Shetlands, and Isabella and Rowallan gas condensate prospects in the Central North Sea, all have the potential to be over 100 million boe. By the end of 2018 there will be very few commitment wells remaining to be drilled in the UK and as a result drilling activity will be largely discretionary and may be more difficult to sustain.

In Norway, the disappointing 2017 results have not deterred plans for 2018. Statoil has already reported plans to operate five high impact exploration tests in the Barents Sea this year, in addition to participating in 20 – 25 further E&A wells across the NCS. Overall, Westwood expects 35 – 40 exploration and appraisal wells to drill in Norway this year a significant increase on 2016.

Elsewhere in Northwest Europe, Ireland saw a frontier play test at Druid/Drombeg in the Porcupine Basin in 2017, which was dry. A Woodside operated exploration well on the Beaufort/Ventry gas prospect is likely to be the next well to drill in the basin. In the Netherlands, Hansa Hydrocarbons had a significant success with the Ruby discovery in 2017, and follow up appraisal and exploration drilling in the Ruby area is expected.

Dave Moseley, Northwest Europe Research

[email protected] or +44 (0)20 3794 5373