The Glengorm gas condensate discovery announced last week could be the biggest in the UKCS since 2008. It will reignite interest in the high temperature, high pressure plays in the North Sea and heralds a mini renaissance in UK exploration.

The Chinese national oil company CNOOC (formerly Nexen CNOOC) with 50% equity and Joint Venture (JV) partners Total (25%) and Edison (25%) have announced the results of the 22/21c-13 Glengorm well in 28th Round licence P2215. The well encountered gas condensate in 37.6m of net pay, interpreted to be in Upper Jurassic aged turbidite reservoirs.

Total has reported recoverable resources of ‘close to 250 mmboe’, which would make this the largest discovery on the UKCS since the Culzean discovery in 2008 with resources of 250 mmboe. The only larger discoveries made in the last 20 years are the 1.1 billion-barrel Buzzard field in the North Sea discovered in 2001 and the 292 mmboe Rosebank discovery in 2004, West of Shetlands. So, this is a significant discovery for the UKCS. Note that neither CNOOC nor Edison has commented on discovered volumes.

The result is at the extreme upper end of pre-drill expectations and the geology in the discovery well must have delivered some pleasant surprises, but it is not clear yet what these were. Upper Jurassic turbidites are highly variable in terms of both thickness and quality across the Central North Sea.

Total did not specify whether 250 mmboe was a probable or possible estimate and Westwood is assuming the latter for now given the limited information. The JV will now appraise the structure which is likely to be compartmentalised like many HPHT fields in the Central Graben to confirm the potentially developable resources. There are follow up Upper Jurassic prospects mapped on the block to test.

Glengorm lies 24 km northwest of Elgin-Franklin and 44 km west of Culzean, so there could be long subsea tie-backs to either installation. Total holds 25% equity in Glengorm and operates both installations. The timing of a development could align with capacity availability at Culzean, due to start production this year, which Westwood estimate to come off plateau around 2023.

The other option would be a subsea tie-back to the BP-operated ETAP infrastructure, which lies 35 km NW of Glengorm. CNOOC may prefer a standalone development. If the discovery be confirmed as c. 250 mmboe following appraisal, this should be an economic option given current development costs.

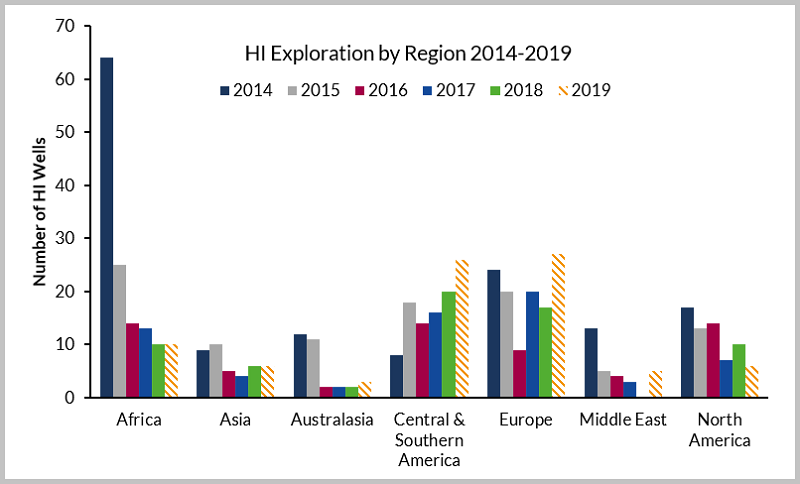

2019 is the most significant year for high impact[i] exploration in NW Europe in a decade. 27 high impact prospects are planned to be drilled, on par with central and south America. The total of over 60 wildcat wells planned in the region is double 2018 and the highest number since 2014. Glengorm shows that high impact discoveries are possible in the UK North Sea, and not just by drilling prospects deemed high impact pre-drill. The unexpected upside can happen.

High impact wells by region by year

Source: Westwood Wildcat Service

Dr Keith Myers, President, Research

[email protected] or +44 (0)20 3794 5383

[i] Westwood define a high impact well as either a frontier play test or a prospect over 100 mmboe of a 1 tcf of gas