In September 2025, Westwood hosted a seminar series exploring offshore energy in a volatile global and UK market. Despite cost pressures and uncertainty, the sessions revealed a resilient outlook, with offshore investment expected to rebound and strategic shifts already underway. Here are the key takeaways:

Global Oil and Gas: A Balancing Act

2025 has been a turbulent year for global oil markets. Consumption has underperformed, prompting repeated downward revisions in demand forecasts. Meanwhile, the rollback of voluntary OPEC+ production cuts has added nearly 3 million barrels of oil equivalent per day (mmboepd) to global supply.

Combined with seasonally soft demand and rising output from the Americas, this influx risks tipping the market into oversupply over the next 12 months. European supermajors are recalibrating their strategies – while decarbonisation remains central, there’s renewed emphasis on disciplined oil and gas investment and cost efficiency.

Despite headwinds, the offshore engineering, procurement, construction and installation (EPCI) investment outlook remains strong. After a dip in 2025, offshore oil and gas investment is expected to average $57 billion annually between 2026 and 2029. Offshore wind will continue to dominate EPCI spend, but lower oil prices and inflated supply chain costs are squeezing upstream cash flow and margins, driving a renewed focus on cost control.

Aging offshore fleets present a critical challenge. Lower dayrates are making it difficult to replace rigs and vessels, potentially impacting project efficiency and emissions management.

Global Offshore Energy EPCI Investment

Source: Westwood Analysis

Exploration: Fewer Players, Smaller Plays

Global volatility and long-term uncertainty around hydrocarbon demand have led high-impact explorers to maintain activity levels to preserve future optionality. However, discovered resource volumes are declining, and the number of companies engaged in high-impact exploration has halved.

National Oil Companies (NOCs) and supermajors now dominate the landscape. In 2024, NOCs accounted for 51% of high-impact well equity and 67% of discovered resources. Yet, opportunities to bring new barrels to market are shrinking due to smaller play sizes and reduced acquisition of 3D seismic data, which is essential for maturing prospects.

To sustain long-term growth, Exploration & Production (E&P) companies may need to diversify – leveraging conventional exploration, accessing discovered resource opportunities (DROs), pursuing M&A, and exploring unconventional plays. This will be crucial as markets continue to favour short-term returns.

Offshore Services: Facing Cost Pressures

Rising supply chain costs have delayed Final Investment Decisions (FIDs), as operators seek price reductions in response to lower-than-expected oil prices. A rebound in FID activity is anticipated in 2026.

Rig contracting has slowed since 2024, leading to reduced utilisation and dayrates. Offshore Support Vessel (OSV) utilisation has also declined, except in the resilient Gulf Cooperation Council (GCC) region. Demand for deepwater rigs is expected to increase from the second half of 2026 as postponed projects resume. The jackup market may also recover, although much depends on Saudi Aramco’s plans.

Despite aging fleets, current market dynamics do not support a newbuild cycle. Instead, operators and service providers must extend asset life and improve operational efficiency. Key growth markets for Offshore Energy Services (OES) between 2025 and 2029 include Saudi Arabia, Qatar and Brazil, with additional prospects in East and West Africa, Southeast Asia, and the Mediterranean.

Offshore Wind: Growing Pains in Maturing Sector

Offshore wind has grown rapidly over the past decade, but 2025 marks the first time the sector has faced significant challenges. Forecasts have been downgraded, and many government targets are now unlikely to be met.

The focus has shifted from rapid expansion to delivery, de-risking, and positioning for future growth. Higher-risk ventures, such as floating wind, are losing momentum. Developers must adopt strategies that manage uncertainty more effectively.

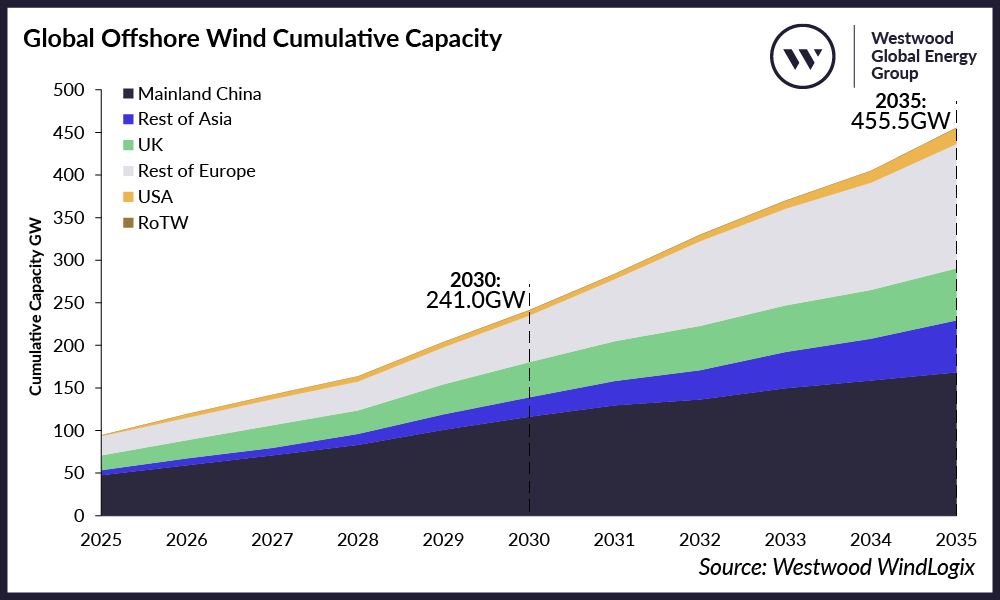

Outside mainland China, Europe is expected to lead offshore wind growth, achieving more than fivefold expansion over the next decade. Asia also represents a key future market. Investment is set to ramp up significantly across geographies and developers, despite current setbacks.

Global Offshore Wind Cumulative Capacity (incl. Mainland China)

Source: Westwood WindLogix

UK Outlook: Energy Strategy and Transition

The UK’s offshore energy sector is at a pivotal moment. Investment levels directly influence the rate of production decline, yet oil and gas projects, development drilling, and exploration have largely paused. While opportunities remain, time is running out.

Oil and gas have become political battlegrounds, and swift decisions are needed to unlock potential. Decommissioning presents a major opportunity, with efficient abandonment key to controlling costs. Crucially, oil and gas must be recognised as integral to the UK’s energy mix – not as an alternative to renewables. Many of the barriers to unlocking the North Sea’s potential are policy-driven and solvable.

The UK’s energy transition is ambitious, but many targets are at risk. Offshore wind remains a global strength, but delivery has been hampered by global headwinds, policy missteps, and overreaching ambition. Significant investment is expected over the next decade, though long-term growth hinges on the uncertain outcome of the Allocation Round 7 (AR7) process.

Hydrogen and Carbon Capture and Storage (CCS) have made notable progress, with the UK showing leadership. However, development has been slower than expected, largely due to delays in government processes and commitments. Scaling these emerging industries will be challenging in a shifting political and energy landscape. A long ‘to-do’ list remains to create the certainty needed for investment.

Conclusion: Opportunity Amid Uncertainty

The offshore energy sector is navigating a complex and volatile environment. Opportunities exist across oil, gas, renewables and CCS, but aging infrastructure, fiscal constraints, and regulatory hurdles must be addressed.

Offshore wind is poised for significant growth, while hydrogen and CCS require accelerated government action. Strategic investment, policy reform, and industry collaboration will be essential to unlocking the full potential of offshore energy in the UK and globally.

Watch the full Offshore Energy Outlook: Finding Opportunity in Volatile Times Video On Demand, here.

Presented by Westwood’s senior research team:

Thom Payne, Head of Consulting

[email protected]

Graeme Bagley, Head of Global E&A

[email protected]

Teresa Wilkie, Research Director – RigLogix

[email protected]

David Linden, Head of Energy Transition

[email protected]

Yvonne Telford, Research Director – Atlas

[email protected]