The global energy crisis has been brewing since the last quarter of 2021, caused by a mix of factors, including resurgent demand after the lifting of lockdown, bad weather, and disruptions to supply chains. It is impacting all areas of the energy market and all geographies. Russia’s invasion of Ukraine has added further flames to the fire with volatility across the global oil, gas, LNG, coal, and power markets. The impact has been felt most in Europe, partly due to its exposure to Russian gas.

While oil prices have shown volatility and reached their highest level since 2014, the relative volatility has been weaker in comparison to the power and gas markets, which has shown massive swings in pricing in Europe this year.

Higher prices drive a resurgent oil and gas industry

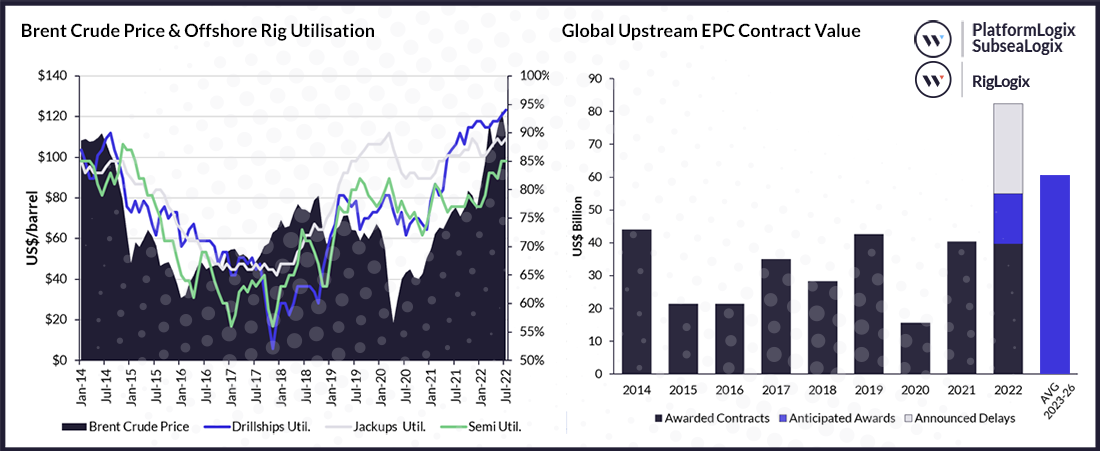

This year’s higher commodity prices have given the oil and gas sector renewed vigour. Offshore drilling rig fleet utilisation is at highs following the rise in crude prices. At the same time global upstream engineering, procurement, and construction (EPC) contract award value has returned to pre-pandemic levels amidst higher commodity prices. The outlook, based on what we can see from operators, is also very strong, with the average EPC spend over the next five years elevated compared to previous years.

Offshore Rig & Upstream EPC Sector Growth

Source: RigLogix, PlatformLogix, SubseaLogix, Westwood Analysis

Data from end 3Q 2022

The issue now is whether the industry can deliver these projects due to issues around supply chain disruption, inflation, commodity price volatility etc., which is making the final investment decision (FID) harder to make, as highlighted by Equinor’s recent postponement of the Wisting project.

Despite doubts on the delivery of these projects, this is still an incredible turnaround for an industry that has been questioning the future of its core business. Oil and gas companies are looking for more hydrocarbons, and they are confident enough in the demand outlook to bet large amounts of shareholder money on it.

Supermajors: What to do with all the cash

What we are essentially seeing is an industry that is being flooded with cash – more than it knows what to do with.

When comparing the cash profiles of the Supermajors (BP, Chevron, Exxon, Shell, and TotalEnergies) in the first nine months of last year against the same period this year, a couple of interesting factors emerge. Operating cash flow has increased by 70% and Capex has increased by over 25%. However, shareholder pay-outs have more than doubled at the same time, therefore the focus is not just about spending more but also about rewarding shareholders.

Of note is that the supermajors had a surplus of US$65 billion in the first nine months of 2022. Therefore, these companies have considerable scope to increase Capex, shareholder pay-outs and/or debt repayments at faster rates than has been seen over the past twelve months. On current trends, the supermajors in aggregate could have zero net debt by the end of 2023 if cash continues to build-up on their balance sheets at current rates.

Supermajor Cashflow Highlights, H1 2021 vs H1 2022

Source: Wildcat, Westwood Analysis

Supermajors are BP, Chevron, ExxonMobil, Shell and TotalEnergies

With the oil and gas pipeline already theoretically ‘full’, the question is whether the supermajors can realistically spend more money here or should these businesses instead be pivoting faster towards the Energy Transition, now they have the cash?

At the same time the scale of the cashflow surplus has attracted the attention of politicians. Windfall taxes have already been imposed in some countries such as the UK, and there is the potential that more countries will follow.

However, an issue that has been highlighted by the Supermajors is that there are limited sizable investment opportunities available in the Energy Transition. Projects related to hydrogen and carbon capture and storage (CCS) – key growth areas for these companies – are at a nascent stage of their development. Acquisitions might be the way to bridge the gap. BP’s US$4.1 billion take-over of the bioenergy business Archaea last month is a good example of this.

Return of the Energy Trilemma

There is another dilemma that has come back to haunt the world, and that is the Energy Trilemma. This envisions creating an energy system that provides energy that is sustainable, secure, and affordable. The Great Energy Crisis has shown us that this Trilemma has perhaps been out of balance, certainly in Europe. That conversation is now changing but it is also leaving governments with some difficult choices.

Looking at the UK for example. Proudly the first major economy to commit in law to net zero by 2050. And the UK has some pretty big ambitions in the medium term; reduce upstream O&G emissions by 50%, bring 50GW of offshore wind and 10GW of hydrogen online, and capture 20-30mtCO₂ per year by 2030.

In theory what should be happening is that hydrocarbon supply and demand declines, while the gap between the two is filled with imports – at least this has been the case since around 2008. However, that reliance on imports has meant exposure to a volatile gas market, which in turn is impacting electricity and gas prices to consumers. It has required one of the largest subsidy regimes to protect customers and businesses from going under.

At the same time, the government has launched a new oil and gas licencing round. Better to plug the import gap with your own oil and gas and produce it in a lower emissions way. Perfect, is it not?

The reality of course is that you need to find new oil and gas in the first place, and in the last decade it has taken five years from discovery to first production. That is way too late to help consumers. The UK, and other countries in Europe, will need to import oil and in particular gas for the foreseeable future.

The question going forward is, what will governments do, to provide that secure, affordable, and sustainable energy their economies need? Certainly, in the case of the UK, Rishi Sunak – the UK’s latest Prime Minister – went to COP27 and “promised to speed up the UK’s transition to renewable energy”. That is arguably the quickest way to transition and to meet the criteria of the Energy Trilemma.

Is the Energy Transition speeding up or slowing down?

So, we have a global energy crisis and governments reacting to it in different ways. Where does that leave the Energy Transition? There are some factors slowing it down and others speeding it up.

First the factors putting the brakes on the transition. As nations have struggled to meet energy demand, the spending on fossil fuels has increased (including for countries that have net zero targets), as the desire for energy security has become an overriding factor. Following the invasion of Ukraine by Russia, geopolitical rifts have been deepened at a time when global co-operation has become more essential to tackling climate change – the world is not on target to meet the Paris Agreement goals. A worsening macroeconomic picture and rampant inflation, raising the cost of deployment and creating uncertainty in demand, could also styme the necessary investments and risk-taking needed to accelerate the new technology build-out. The cost of some renewables has risen for the first time after a long downward trajectory.

On the other hand, there are also several positive signs. The EU has been doubling down on the transition, both through its Fit for 55 and Re-Power EU initiatives, that have a central aim of decoupling from Russian gas and accelerating the adoption of renewables (and other clean energies such as green hydrogen). The US Inflation Reduction Act, passed into law this August, is set to boost a whole range of clean energies through a $391 billion funding plan. Emerging economies and large future polluters are also continuing to commit to climate action, with India publishing its long-term emissions strategy to reach net zero by 2070 at the COP27 conference. COP27 itself has also had a more positive tone (at the time of writing) than commentators had expected. Corporations continue to pursue their net zero goals with ever greater vigour, with corporate power purchase agreements for renewable power at record highs.

The overarching driver for the transition is how governments are going to react to today’s crisis, setting the policy framework for investment going forward. More change is to be expected as the crisis unfolds, but what are policies being implemented today set to do for the future energy mix?

‘Stated policies’ are favouring renewables

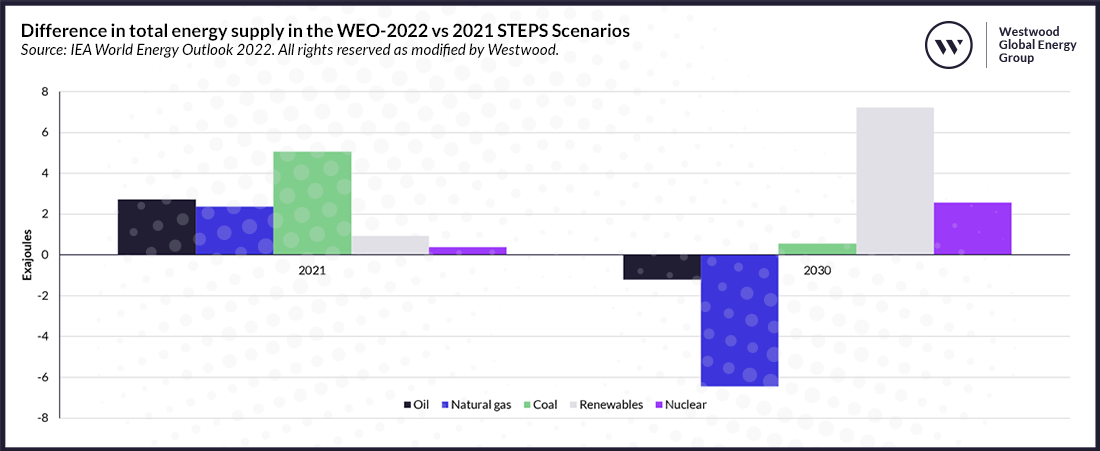

The latest IEA Stated Policies Scenario (STEPS), published October 2022, shows the impact of recent policy changes on global energy supply. This scenario does not indicate a full paradigm shift to make net zero by 2050 imaginable but shows how quickly things are changing. If governments are in the driving seat, is what they are doing now having an impact on the trajectory of the world? The short answer is yes.

The STEPS scenario – one of the IEA’s more conservative ones – considers existing policies and ones under development right now (rather than grand future goals), to see what this would mean for the global energy mix. It’s considered a realistic way of looking at the market and provides, in our opinion, a useful reality check.

Difference in total energy supply in the WEO, 2022 vs 2021 STEPS

Source: IEA World Energy Outlook 2022. All rights reserved as modified by Westwood.

The IEA explain that STEPS “provides a more conservative benchmark for the future, because it does not take it for granted that governments will reach all announced goals”.

While all fossil fuels (coal in particular) are near term winners, this is reversed in the coming eight years. By 2030 a little less oil is needed than had initially been forecast back in the World Energy Outlook of 2021. More importantly, natural gas is hit significantly with supply peaking by the end of this decade. Instead, renewables play a much bigger role globally.

Governments are looking to reduce their exposure to natural gas and favour renewables in their place. There are a lot of regional nuances to this story, with great declines in the US and Europe while in emerging economies gas demand continues to rise, but as a global picture it is stark. This scenario won’t get you to net zero, but it does say one thing: watch out for the further acceleration of renewables.

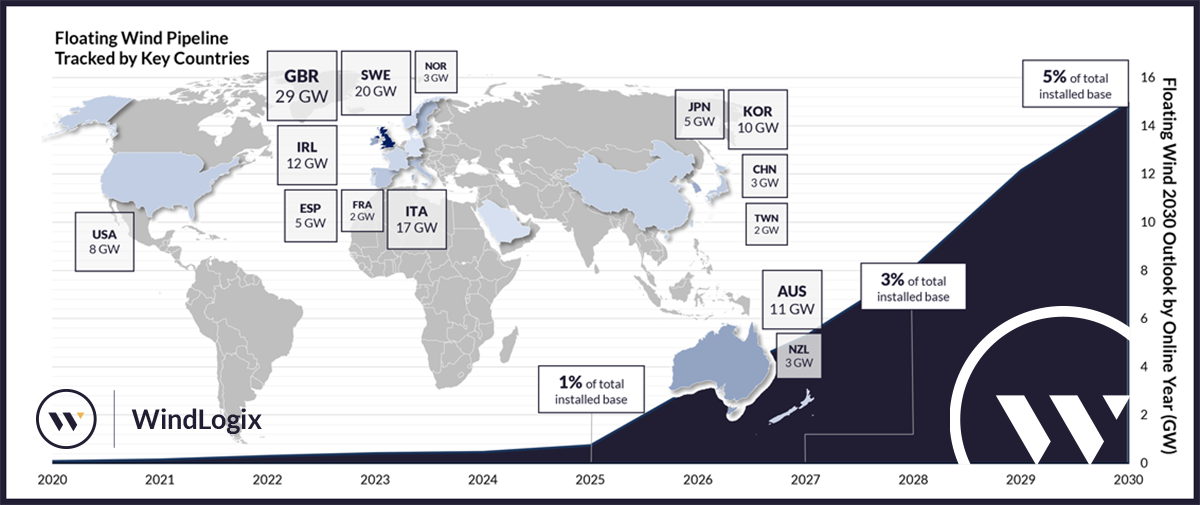

Spotlight on floating offshore wind

To support this acceleration, there are several renewable technologies set for growth. Some, like solar, are well established, competitive, and growing fast. Others are still in their infancy, including floating offshore wind. This technology has the potential to democratise offshore power for the entire world and be the foundation of an ocean industrial revolution, but right now operational capacity stands at 130MW, which is just enough to power a village.

That being said, Westwood is currently tracking 127GW of projects being developed or have plans announced. From an industry with almost nothing, this is an incredible outlook and represents around $335 billion EPC value opportunity (turbines, foundations, cables etc,). That is $100 billion more than what has been spent on the entire Offshore wind industry to date.

Floating Offshore Wind Outlook

Source: WindLogix, Westwood Analysis

In the coming years, the offshore floating wind industry is expected to grow fast. Initially in places like South Korea, the UK, Spain, and China. But it faces many challenges, notably that it’s more expensive than traditional fixed bottom wind, there are still over 80 different technology designs whose technical limits are untested, and a new supply chain needs building out. Will technologies such as this flourish or forever be a niche?

In the midst of every crisis, lies great opportunity

The first true global energy crisis is having a profound impact on the trajectory of the energy industry. It has brought the concept of the Energy Trilemma back into the frame, with governments and corporates – and the resurgent oil and gas sector in particular – confronted with difficult choices on how to react.

With an increased level of uncertainty, the Energy Transition faces several barriers in the short term. But decisions governments are making today favour a speeding up of the transition, to the benefit of the deployment of renewables (at the expense of natural gas). This is not a paradigm shift to allow the world to reach net zero by 2050, but the crisis is certainly helping to put things in the right direction.