It is a well-known fact that modern high-specification[1] (high-spec) or ‘heavy-duty’ jackups are the future of the Northwest Europe shallow-water drilling market, but for the first time the supply of such units has surpassed that of its traditional 1980s-built standard jackup counterparts. Furthermore, utilisation and day rates, as well as the volume of future demand for high-spec units is now also surpassing that of standard units.

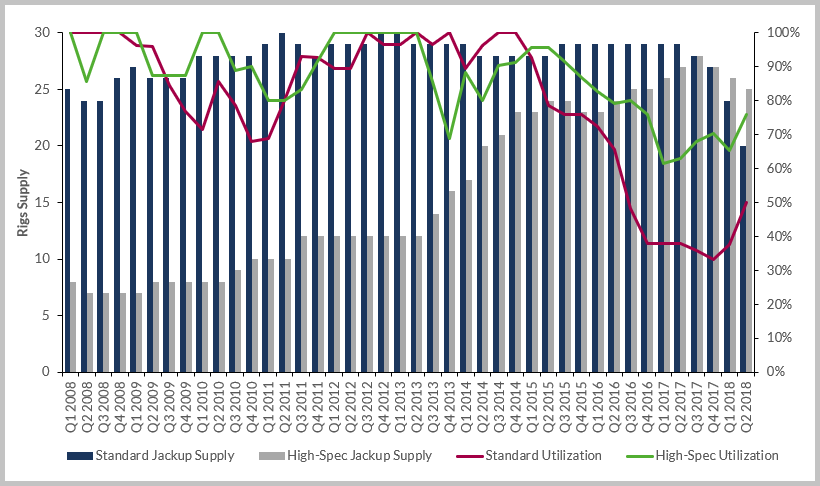

As shown in the graph below, Northwest Europe standard jackup supply in the first quarter of 2008 totalled 25, while high-spec units accounted for a meagre eight units. At its peak in late 2012, the standard fleet consisted of 30 units and had 100% utilisation. Over the same period, the high-spec segment grew by four units and then between late 2013 to early 2015, it swelled by another eight units, reaching a high of 24 and utilization of 96%. This was the result of drilling contractors upgrading their fleets with newbuilds ordered in 2012 and 2013. Fast forward to second quarter of 2018 and high-spec jackup supply is little changed at 25, but the number of standard units had declined to 20.

Northwest Europe Standard Jackup vs High-Specification Jackup Supply & Utilisation

Demand for rigs with the capability to drill in deeper waters, in harsher conditions and targeting wells with more complex reservoirs (i.e. high-pressure high-temperature) was always inevitable in a mature region such as the North Sea, as resources in benign and easier to drill areas dry up. As operators continue to move into new and often more challenging areas to discover and develop hydrocarbon resources, the drilling technology must keep up with this expansion.

The jackup fleet has suffered an overall lack of demand over the past two years, and as a result the standard fleet has had to endure added competition from the high-spec fleet, forced to compete for work that in better times those rig owners might not be interested in. The result has been an oversupply of standard jackups and utilization falling from a high of 100% in late 2014 to only 33% by late 2017. Since then, utilization has risen to 50% thanks primarily to the retirement/divestment of several older units from the fleet. However, there are still five cold-stacked and six ready-stacked jackups in this segment, and we believe anywhere from three to six of these units are circling the drain due to several factors such as age, lack of demand, high reactivation costs, etc. As a result, we believe this segment of the fleet is likely to shrink further over the next 12 months. This will undoubtedly cause an increase in utilization, albeit not one primarily driven by a demand increase.

As of mid-July 2018, supply and demand of the high-spec jackup fleet is tight, with utilization just shy of 80%. This segment consists of 25 units, including one that is cold stacked and unlikely to drill again. Three jackups are ready stacked, while another three are in shipyards (one of which is undergoing a major modification program in preparation for a contract starting in late 2019). Sixteen of these units are currently on contract, three more will begin work over the next two months and one will roll off hire. This leaves only three high-spec rigs available for work in the short term and, assuming all existing contract options are exercised, there is no remaining high-spec jackup availability until at least the second quarter of 2019.

Because of the tight market, drilling contractors with high-spec, North Sea-capable assets outside of the region have realized an opportunity and are taking action. Noble has already won two contracts to bring jackups into the UK sector – one for a rig currently in Southeast Asia and another for one in the Middle East. As the market continues to constrict there could very well be additional units moved to the area.

Though there are only a handful of high-spec requirements left that are scheduled to begin in 2018, next year is a very different story. RigLogix currently records 14 separate tenders or Requests for Information (RFI) issued for jackup programs starting in 2019 in the UK Norway, Denmark and the Netherlands – the majority of which is for high-spec work. The few planned P&A campaigns will likely be handled by standard jackups at lower day rates as this work provides no financial return to operators.

As high-spec demand has risen, drilling contractors are beginning to test pricing. Though very few values have been revealed on new fixtures, it is understood some of the largest high-spec units are being bid on UK work (where most of demand is currently stemming from) in the $100,000 to $130,000 range with rig owners able to charge a premium due to limited availability. In comparison, standard jackups in the UK sector are being secured around the $60,000 mark, with work in the Dutch North Sea understood to be at even lower rates.

Over the past year, the recovery in the North Sea harsh-environment semisubmersible market has made the most headlines, but the region’s shallow-water counterpart has also made progress as demand for the largest and most modern jackups quickly increases. These high-spec units will continue to push out the older and less capable tonnage, and it seems likely that the North Sea, with its increasing demand, utilisation and day rates, will continue to be an attractive destination for top of the line jackups in the coming years.

Teresa Wilkie, Senior Rig Market Analyst

[1] * High-spec defined as those jackups with a 2 million pound or greater hookload capacity. These rigs will also generally have a rated drilling depth of at least 30,000-ft and a rated water depth of 375-ft or more.