After four plus years of low rig utilization and day rates, company layoffs, operator spending declines, just to name a few, it appears that the offshore rig market may finally be able to at least see the light at the end of the tunnel. Although the recovery that is often reported within the industry is not here yet, it is closer than it has ever been, and for once the sense of optimism felt throughout every segment of the industry is not just wishful thinking. Of course, all of the predicted improvement assumes that there is no oil price or global energy demand collapse, or that no political or issues of that ilk that will disrupt the momentum that is building. The October 2018 RigOutlook, which forecasts rig supply, demand and utilization for the next year, details how activity in the market will fare during the next year through September 2019.

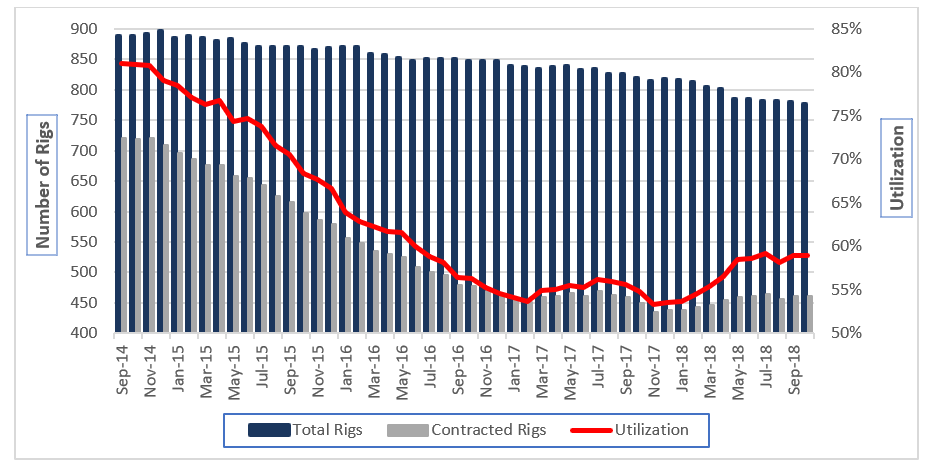

In the current rig fleet, there is a 316-rig gap between supply and demand, and that number excludes 118 rigs that are under construction and cannot find their way into the fleet. Even though attrition has accelerated in the past four years, the market is still far out of balance as attrition alone cannot solve the oversupply problem. Since September 2014, generally recognized as when the current downturn began, there have been 220 rigs removed from the fleet, but utilization during the same period fell from 81% to 59%. Figure 1 shows that rig demand and utilization fell consistently through February 2017, since then utilization has only improved by 6% in the past 15 months. Overall, supply fell by 119 units from its high in December 2014, while demand dropped by 259 units during the same period.

Figure 1: Worldwide Competitive Rig Supply, Demand, and Utilization (September 2014 – October 2018)

Figure 1: Worldwide Competitive Rig Supply, Demand, and Utilization (September 2014 – October 2018)

Source: RigLogix

The October 2018 RigOutlook, a forecast of rig supply, demand and utilization, calls for a slowed rate of attrition for the next year compared to the past few years. The rigs retired to date were what has been termed “low hanging fruit” and easy decisions to make, and while there are likely some of those remaining, an expected improving market makes it a bit more difficult for rig owners to dispose of some rigs if they believe there could ultimately be a chance to work them.

As of November 2018, there were 118 rigs on order or under construction. Although these rigs are maintained, many have been essentially finished for two or more years. In the past few years, some shipyards have ended up owning rigs after construction contracts were cancelled and they have finally begun to sell some of the units. Most notably, Borr Drilling spent a total of $2 billion to purchase 14 jackups from Singapore’s PPL Shipyard and KeppelFELS, five of which have been delivered to Borr. So far, the company has received only Letters of Intent (LOI) for a few of these rigs, but formalized contracts for at least two are anticipated any day now. Outside of these units, only four others have contracts in place, three harsh-environment semis and one jackup – all destined for the North Sea. In the meantime, even though most rig owners will continue to not take delivery of any newbuild units until a contract is secured, it would likely come as a surprise to most that since 2016 there have been 58 rig deliveries. We believe the next year will be no exception, and we expect around 20 newbuilds to enter the fleet.

The good news is that rig demand during the forecast period that runs through September 2019 will improve substantially for both jackups and floating rigs, although the increases increases will not begin to accelerate until late in the forecast period. According to RigLogix data, there are currently over 250 rig requirements worldwide where an expression of interest or market survey has been issued to pre-tender or an outstanding rig tender pending award. We expect that this work, along with other requirements that materialize during the next year, coupled with rig owners extending contracts for already contracted rigs, will result in a significant increase in the number of contracted jackups and floating rigs through September 2019.

Rig day rates have seen little, or in some cases, no improvement, and even though rig owners are reporting smaller losses on their earnings calls, they have yet to return to profitability. However, there have been a few isolated rig markets where high demand has enabled day rates to grow substantially the past year or so. One of these areas is in Norway, where the most recent fixtures for harsh-environment semis have been at or over $300,000, which in some cases represents a doubling from earlier in 2018. Several contracts signed this year have been for work starting in 2019 or even 2020, a clear sign that operators believe waiting until later will result in paying well above $300,000.

Another region where rig owners have experienced noticeable day rate increases the past year has been the U.S. Gulf of Mexico jackup market. Fixtures for long-legged jackups (375 ft and greater) that one year ago were routinely set in the $60,000-65,000 range were most recently in the $80,000-85,000 range, a 23.5% increase on the high end. Shallower-rated units have also fared well, with rates increasing from $50,000-55,000 to $65,000-70,000 in October 2018. At the end of October there were 11 of 12 marketed units, with the lone idle unit undergoing its Special Periodic Survey (SPS). However, it is expected to return to work for owner Arena Offshore around mid-November. Otherwise, in a market where most contracts historically have been 1-2 wells, eight of the 11 contracted units have at least 90 days of backlog, and six of the eight have contracts that will keep them working past mid-2019. We expect at least one currently cold stacked jackup to be reactivated in the first half of 2019, and between one and three units will be mobilized into the region from international locations.

Assuming the market fundamentals that drive the rig market remain in place or even improve, the recovery, which is still in its early stages, will occur, but there still remains some time before it makes it all the way back.

Terry Childs, Head of RigLogix

[email protected] or +1 (713) 929-3324

For a demonstration of the RigLogix service, please click here.