19th February 2018

Corrosion resistant alloys (CRAs) are back in demand. The supply chain is preparing for an uptick in deliveries as a growing proportion of field developments require high quality downhole tubulars. Sour gas fields and high pressure high temperature (HPHT) wells typically require stainless, duplex or Nickel alloys to reliably transport production from reservoir to surface facilities, and these field developments are growing as a proportion across the industry.

From Buckskin in the US Gulf of Mexico to Dongfang in the South China Sea, the backlog of projects under construction that will drive higher quality steel demand is growing. These are combined with major project expansions, such as Tengiz, and tens of other sour gas projects approaching the final investment decision (FID) stage in the next three years, all expected to require substantial volumes of high quality oil country tubular goods (OCTG).

Shortage in the North Sea?

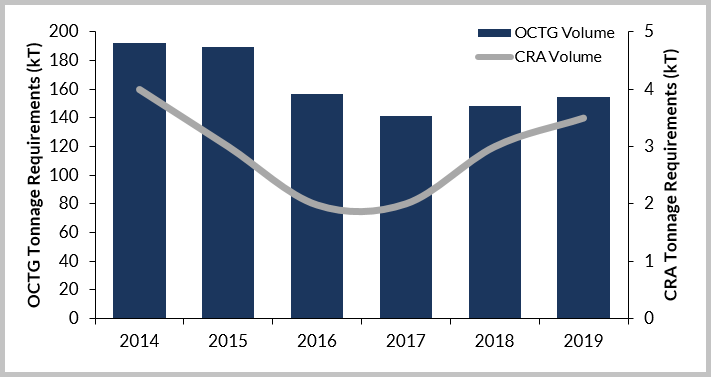

The North Sea CRA sector is estimated to have suffered more substantial losses in percentage terms than any other major region since the commodity price downturn – 2016 demand at 2,000 tonnes representing less than 50% of the equivalent 2014 market. This has led to anecdotal reports of a widespread reduction in inventories across the region as suppliers have incrementally reduced regional production and imports.

Having worked through an extremely challenging three-year period, a cautious optimism is beginning to return to the market, however. Westwood expects a minimum of 11 North Sea fields to pass the FID stage this year, supporting a near-term boost to production volumes. Of these, at least five appear to be strong candidates for CRA tubulars, including Blythe and Apache’s Seagull, in particular. Beyond the new field development sanctions, Maersk Oil’s Culzean HPHT and BP’s Rhum gas field are expected to require additional volumes of CRA OCTG.

As the broader downhole tubulars sector increases modestly in volume terms, supported by a more positive oil price outlook and sanctioning of drilling activity, the CRA tubular segment is set for faster growth. Coupled with a potentially significant reduction in held inventories, we anticipate upward pressure on pricing for the required grades as new projects pass FID.

North Sea OCTG & CRA Volume Demand, 2014-2019

North Sea OCTG & CRA Volume Demand, 2014-2019

Source: Westwood, Metal Bulletin Research

No Shortage in the Middle East

While the relative strength of the North Sea market may have caught the supply chain by surprise, good visibility of major developments in the Middle East has attracted the attention of all the major CRA suppliers. As the largest global market, the race to supply high value Nickel alloys to sour gas field developments in the region has intensified.

In addition to requirements in the more established tubular markets, E&P operators in Egypt, Libya and Iran have placed confidence in projects that are likely to need among the highest quality alloys on the market. In more established countries, such as Saudi Arabia and the UAE, gaining qualification for the required grades will likely be a focus for those suppliers not yet qualified with a more limited pool of suppliers currently active (compared with elsewhere in the region).

Middle East OCTG CRA Volume Demand, 2014-2019

Middle East OCTG CRA Volume Demand, 2014-2019

Source: Westwood, Metal Bulletin Research

The Beginning of a New Cycle

Historically, the use of CRAs has correlated closely with the development of offshore fields, albeit with a bias towards the regions producing higher Sulphur content hydrocarbons. At this stage of the industry cycle there are signals that there may be a change in the typical regional relationships between well footage drilled and CRA requirements due to the relative prevalence of sour gas and higher temperature projects.

Westwood Global Energy is working on an upcoming study with Metal Bulletin Research to explore the global CRA sector in depth, with a focus on OCTG.

Matt Loffman, Associate Director

[email protected] or +44 (0)20 3794 5393