27th November 2017

In the recent Autumn Budget, the UK Chancellor announced the introduction of Transferrable Tax History (TTH) mechanism from November 2018, in an effort to narrow the value gap between sellers and buyers of late life assets in the UKCS. This policy has been widely welcomed by the industry as a potential driver for renewed interest and capital investments into an ageing basin, amidst a volatile commodity price environment.

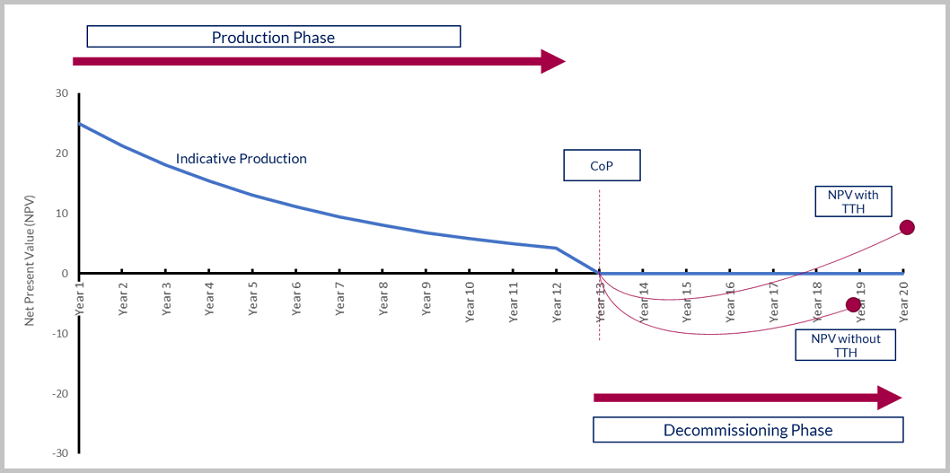

Under the current fiscal regime, the buyer of a late life asset is unable to successfully capitalise on the tax relief associated with decommissioning costs without an adequate tax payment history. While the quantum of TTH to be transferred is subject to commercial negotiations, Westwood believes it is nevertheless a constructive mechanism which should help in bridging the valuation gap and therefore in principle lead to more transactions in the UKCS. However, it is worth mentioning that TTH: (i) is not a mechanism for the buyer to claim greater tax relief than the seller, and (ii) should allow the seller to achieve a comparatively better valuation as demonstrated in the NPV illustration below.

Indicative Net Present Value (discounted at 10%) of a late life field

Indicative Net Present Value (discounted at 10%) of a late life field

Of late, a number of late life asset buyers in the UKCS have been smaller operators with lower overheads and often backed by financial sponsors with a defined investment horizon. Considering the near to medium term outlook for commodity prices, Westwood believes the key challenge in the UKCS is for mature fields to successfully operate on their own or as a hub for smaller fields. In the current oil price environment, incremental production volumes from mature fields are minimal whilst the ongoing operating and maintenance costs are significant. Buyers and new entrants into the basin will need to add new volumes and /or reduce costs by deploying innovative approaches. An example of which has been Wintershall’s approach of operating its SNS facilities remotely from onshore in the Netherlands.

The number of private equity backed E&P vehicles in the UKCS can only be a handful, as capital is fungible and will pursue the best risk / reward opportunities across a number of geographies. Accessing capital markets for the vast majority of E&P companies will continue to be challenging in the current environment, which is a key deterrent to M&A transactions.

Whilst Westwood acknowledges the importance of TTH in bridging valuation gaps, it doesn’t expect a flurry of UKCS transactions to consummate in the near to medium term, as the underlying commodity price environment continues to be challenging.

Yvonne Telford, Senior Analyst, Northwest Europe Research

[email protected] or +44 (0)1224 502783

Ian McDonald, Consulting Manager, EMEA Consulting

[email protected] or +44 (0)1224 502644