The geology has not changed – just the mindset. While political rhetoric paints UK production in terminal decline, the subsurface still holds untapped potential. What is needed is a new perspective.

In 2019, the NSTA projected that 6.5 billion boe could be recovered from the UK North Sea between 2025 and 2050. At the time its strategic theme was maximising economic recovery from the basin, with a challenge for the sector to achieve 1.3 million boepd in 2030. Since then, that projection has been revised down to 0.6 million boepd in 2030, and 3.8 billion boe recovery. This is only 25% of the 15 billion boe oil and gas demand estimated by the Climate Change Committee, in a balanced pathway to Net Zero by 2050. The UK is set to import the majority of this.

What has changed since 2019?

The geology has not changed. Opportunities which existed in 2019 still exist today. Commodity price volatility has always been a challenge. Instead, the fiscal, regulatory and political environment has led to companies deferring or cancelling plans for both short and long-term investments. The downgrade from 2019 estimates reflects investor confidence not a reassessment of the basin’s geological potential.

There is no escaping the fact that the UK North Sea is a mature basin which is in production decline. While the decline ultimately cannot be prevented, there is still a substantial prize available to companies and the government, if the investment environment allows it.

The Prize

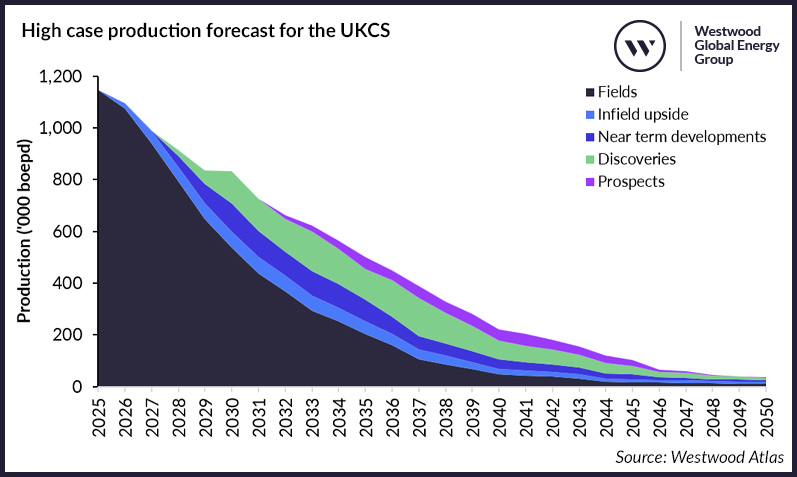

Westwood estimates that in a high case, the UK Continental Shelf (UKCS) could produce 4.3 billion boe (Figure 1). However, in a substantially improved market environment, including significant changes to tax, licensing and regulatory approvals, and favourable commodity prices, the UK could unlock up to 7.5 billion boe[1].

A major shift in investor sentiment would also be required to achieve this, built on:

- A stable and globally competitive fiscal policy

- Supportive investment environment

- Long-term commitment to ongoing licensing

- Faster approvals process for new developments and licence awards

- Pragmatic decarbonisation policy that supports project viability and encourages investment

Figure 1: High case production forecast for the UKCS, including upside from infill drilling, near-term developments, discoveries and prospectivity

Source: Westwood Atlas

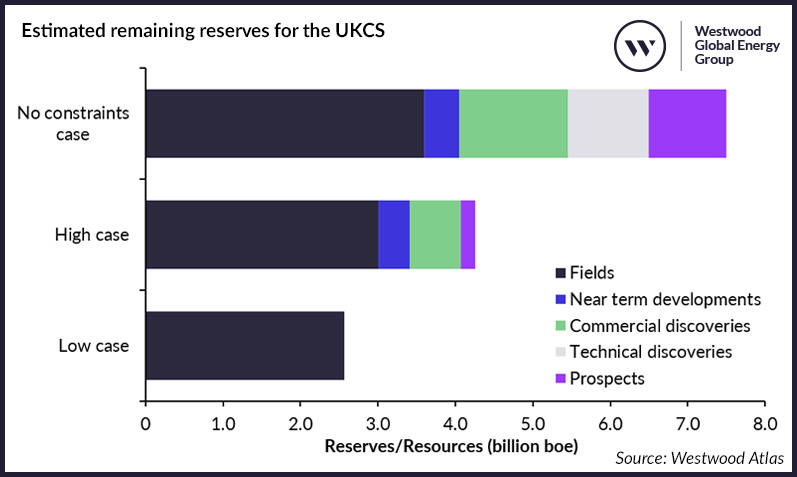

While the shift in investor sentiment to reach 7.5 billion boe would need to be significant, it demonstrates the prize on offer with the correct support for the industry. Conversely, if investor sentiment were to deteriorate further, there is a risk that recovery could be as low as 2.6 billion boe (Figure 2).

Figure 2: Estimated remaining reserves for the UKCS in three scenarios

Source: Westwood Atlas

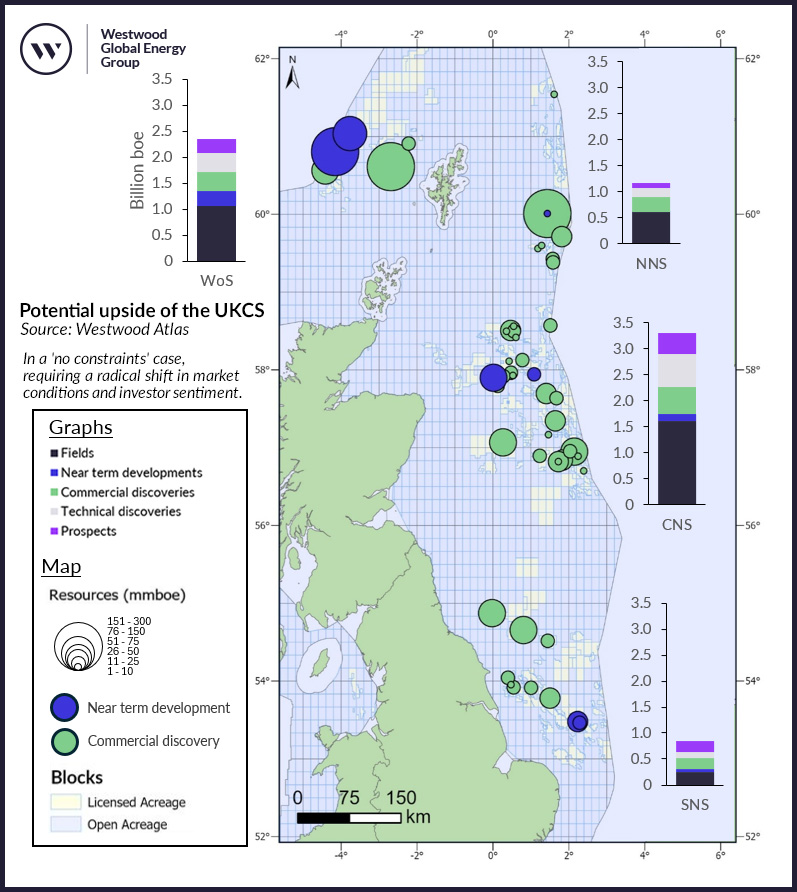

Substantial potential exists in advanced pre-sanction opportunities. Of the 7.5 billion boe identified, c. 0.5 billion boe is found in near term developments (NTDs) – opportunities where technical and commercial plans for development are well advanced. An additional 1.4 billion boe is associated with discoveries that Westwood deems to be potentially commercial for development (Figure 3), representing a sizeable opportunity that could be unlocked, given a supportive investment climate.

Westwood also holds c. 20 ‘drill-ready’ exploration and appraisal (E&A) opportunities. In many cases, operators are only waiting for the right investment environment to commit to drilling them. In recent years, while E&A drilling numbers have reached record lows, the success rates have been high. With a focus on the potential for future gas developments, there are tangible E&A opportunities particularly in the Southern North Sea, West of Shetland and Quad 9 of the Northern North Sea.

Of the 7.5 billion boe potential, c. 7.3 billion boe is located within 50 km of existing hubs. Developing future fields as tiebacks to existing infrastructure can reduce development costs, lower emissions intensity and enable development of resources that would otherwise be uneconomic. New tiebacks also help to extend hub life. Supporting hub longevity is essential to realising the potential of the North Sea and helping to deliver cost-effective, lower-carbon developments. A high number of fields and hubs could cease production before the EPL ends in 2030. Once these facilities cease, it will be too late to unlock many tie-back opportunities and therefore the time for an investment re-set is now.

Figure 3: Potential upside of the UKCS in the ‘no constraints’ scenario

Source: Westwood Atlas

The government has stated its intention to “not award new licences to explore new fields”. However, substantial volumes of contingent and prospective resources exist in unlicensed acreage. The Westwood Atlas database holds 9.7 billion boe of risked prospective resources within 50 km of a producing hub, c. 76% of this is currently unlicensed. In addition, 2.3 billion boe of discovered contingent resources lie unlicensed within 50 km of a production hub. Allowing appropriate new licence awards provides an opportunity to examine and potentially develop some of this resource.

A key element of continuing new licence awards is the need for ‘licence churn’. The NSTA is responsible for ensuring licences are held by companies best placed to move the opportunities forward, facilitated by regular relinquishment and relicensing of acreage. Without new licence awards, it becomes more difficult for the right company to take opportunities forward. Perhaps most importantly, preventing new licence awards would further damage investor sentiment and send a political message that the UK is a closed shop to global investors.

Conclusion

Many of the barriers to unlocking the UK North Sea’s potential are not technical, they are policy driven and solvable. A constructive outcome from the recent government consultations on the Future of the North Sea and the fiscal regime, combined with pragmatic policy change, could unlock significant value. This would boost tax revenues, protect jobs, support lower emissions intensity production and help fund the energy transition.

This is not an exercise in nostalgia – it is about building a balanced and secure future. The geology is unchanged. The skills remain, for now. With timely decisions, the North Sea can continue to contribute meaningfully to the UK’s energy system as it transitions to net zero.

Download the Summary Report, here.

Matthew Belshaw, Senior Analyst – Northwest Europe

[email protected]

Alyson Harding, Technical Manager – Northwest Europe

[email protected]

[1] The analysis considers prospects and discoveries held in the Westwood Atlas database and assesses the geological opportunity at a basin scale. It does not assess project-level commercial viability of all opportunities.