Geothermal energy is rapidly evolving from a niche technology into a strategic component of global decarbonisation efforts. Its ability to deliver firm, low-carbon heat, cooling and baseload electricity makes it an essential complement to intermittent renewable energy sources. For onshore drilling rig owners and the wider oilfield equipment space, this shift offers a significant opportunity to diversify operations and capture additional downhole value, particularly in regions where geology, policy and demand converge.

Market momentum

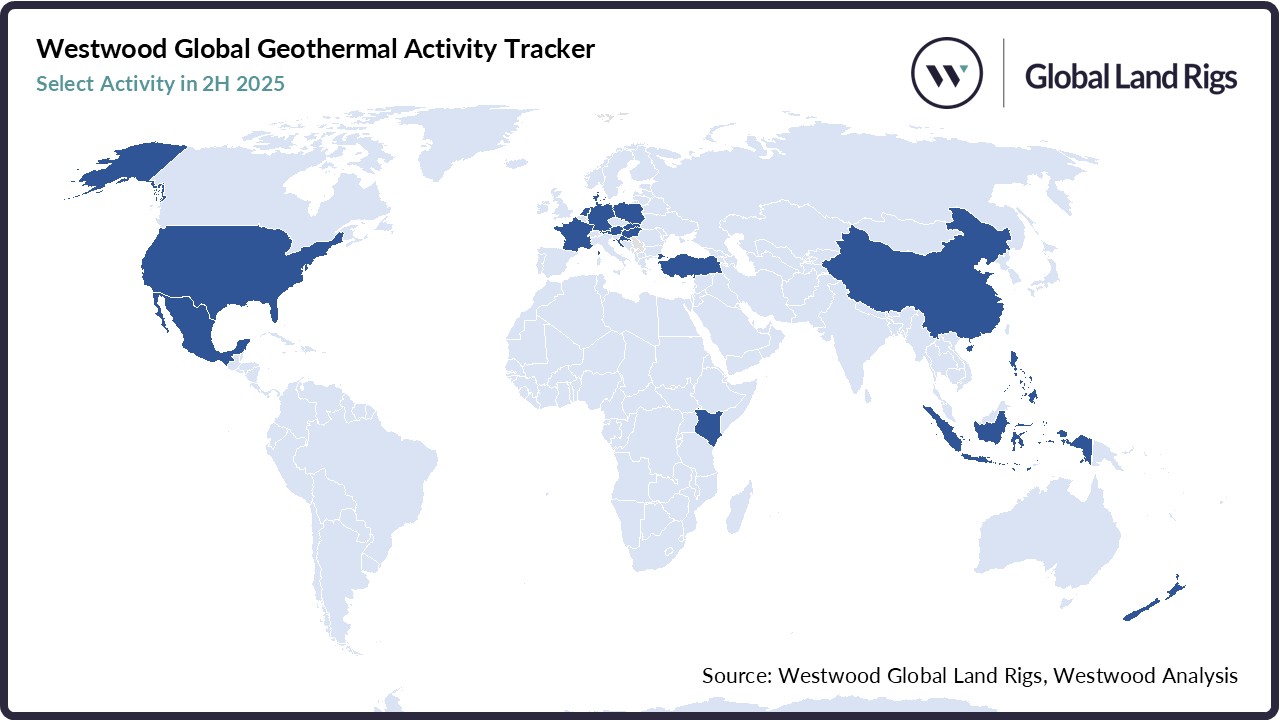

Geothermal energy markets have historically been dominated by Indonesia, Iceland and, more recently, Turkey. However, the geothermal sector is now gaining momentum worldwide as governments and investors recognise its potential to provide much needed reliable, clean, heating, cooling and power generation in transitioning markets.

In the United States, long-dated federal tax credits, state-level incentives, dedicated research and development funding, and growing interest from new demand centres (including data centres) have accelerated deployment. Similar progress is now visible in Europe, particularly in Germany’s Upper Rhine Valley, where projects led by Vulcan Energy are among the most promising geothermal developments, combining different revenue streams with strong policy and funding support. Germany’s Geretsried project, located in Bavaria, uses a novel closed-loop system, and further illustrates strong backing for next-generation technologies, while projects in both France and the Netherlands highlight growing interest beyond traditional markets. The usage of geothermal on islands such as the Canary Islands and New Zealand, which typically rely 100% on high-cost imports, is also growing.

Expanding use cases

Geothermal’s expanding use case is supported by new system designs but enabled primarily by advances in drilling. Modern drilling technology – such as directional drilling, high temperature drill-bits and real-time downhole sensing – allow access to deeper, hotter rock with greater precision and at lower cost. Systems such as Enhanced Geothermal Systems (EGS) and Advanced or closed-loop Geothermal Systems (AGS) then build on this capability by making heat extraction more predictable and repeatable, reducing geological risk and improving scalability. Together, improved drilling and system design transform geothermal from a location-specific resource into a scalable, infrastructure-style energy technology. Our geothermal explainer explores this further.

Beyond technological innovation, the value proposition for geothermal energy is broadening beyond electricity, cooling and heat generation. Some projects are integrating direct lithium extraction from geothermal brines, creating dual revenue streams from both power and critical minerals essential for batteries. Geothermal is also being paired with carbon management initiatives, sharing subsurface data and powering capture technologies such as Direct Air Capture (DAC), and is attracting high-load customers like data centres that require firm, low-carbon power and heat management.

Where it works and where it doesn’t

Geothermal projects succeed where four critical factors align – favourable geology and temperature gradients, supportive regulation and incentives, infrastructure and market access, and stable offtake demand for heat, power, or minerals.

Regions such as the US West demonstrate this alignment, with high heat flow, improved permitting timelines, and proximity to transmission infrastructure driving a robust project pipeline. Conversely, countries like Indonesia, despite vast geothermal potential, have only developed a fraction of their resources due to persistent policy and infrastructure challenges. Effectively dealing with these shortcomings will unlock significant potential.

Implications for onshore rigs

The rise of geothermal energy has direct implications for onshore rig contractors. With global land rig utilisation currently around 46%, geothermal could provide a vital boost to the sector, particularly in regions with surplus rigs such as Asia Pacific and Western Europe.

Rig owners ought to evaluate fleet capabilities and consider upgrades to meet geothermal drilling requirements, which often include higher hook loads, mud cooling systems, and HPHT-rated equipment than in conventional oil and gas wells. Similarly, geothermal drilling in cities for district heating systems and industrial uses like hospitals, often has further requirements, including grid-connectivity and greater soundproofing. This could lead to some markets, such as Western Europe, being undersupplied in rigs capable of drilling geothermal wells, despite a surplus of unutilised rigs.

While some existing rigs can be upgraded – as demonstrated by UGS Rig 110 in Germany following a six-month modernisation campaign – many units in the global rig fleet are over 20 years old and require re-activation from their current cold-stacked status. Drilling campaigns targeting deep, high temperature wells may therefore justify purpose-built units in place of upgrades. Recent examples include Arverne Drillings Rig BO18 in France and Star Energy’s Star Antasena Rig in Indonesia. Last year also saw construction of the City Rig 500, built specifically for drilling in urban environments, with a three-year framework agreement signed for drilling 20 geothermal wells across Denmark and Germany. The solution depends on target depth, location, casing weights, temperature/pressure envelope, and expected well count per field.

Another option is to move rigs into locations where demand outweighs supply. While this may be a solution for certain areas, rigs must also be certified for use in each jurisdiction. For example, rigs in Western Europe are required to have a series of different certifications enabling them to work across the EU, something that rigs from outside of the region may not have. Obtaining recertification for rigs that are already in operation can be a challenging process and, in many cases, will not be possible, especially for rigs where all construction information is not available.

Strategic opportunity

Geothermal energy represents a growth avenue with new momentum for rig contractors seeking diversification. Advances in technology, the value proposition and supportive policy frameworks are opening existing regions and expanding the range of viable geographies, creating new opportunities for those prepared to adapt. Rig owners marketing units are required to have the correct certification for these diverse geographies and should appropriately consider potential upgrades or commissioning purpose-built units to position themselves to capture demand in this emerging market.

Westwood has supported the drilling contractor community for decades and has recent experience advising the wider value chain on the geothermal energy industry.

David Linden, Executive Director & Head of Energy Transition

[email protected]

Nick Patience, Senior Consulting Manager

[email protected]

Ben Wilby, Manager – Onshore

[email protected]

Ben Clark, Senior Analyst – Energy Transition