The U.S. frac sand market has heated up in 2016 even with depressed oil prices. Many operators have increased proppant intensities in their frac designs and are testing upwards of 5,000 pounds per lateral foot while increasing the size of their laterals. Some of the these operators are Devon Energy (NYSE: DVN) and Chesapeake Energy (NYSE: CHK) who have tested in the SCOOP and Haynesville.

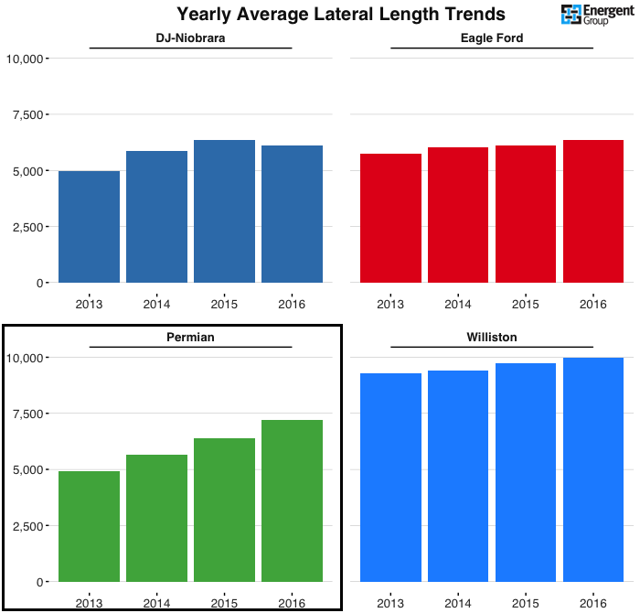

Horizontal wells in the Permian basin average 7,500 foot laterals and 11 million pounds of proppant on average. In 2017, expect laterals to grow slightly as companies test out 2 mile laterals in some areas. With the price of oil coming back are operators ready to ramp up activity how will this impact sand companies in 2017?

Source: Energent Group

Highlights from major sand producers

In July of 2016 US Silica (NYSE: SLCA) announced the acquisition of NBR Sand to provide to focus on Eagle Ford, Eaglebine and Haynesville markets to handle regional sand demand growth. The company believes that regional sand volumes will grow by 68% in 2017. Recently added Sandbox Logistics is expecting to double market share within the next 12 to 18 months showing the importance of last mile logistics as operators increase activity

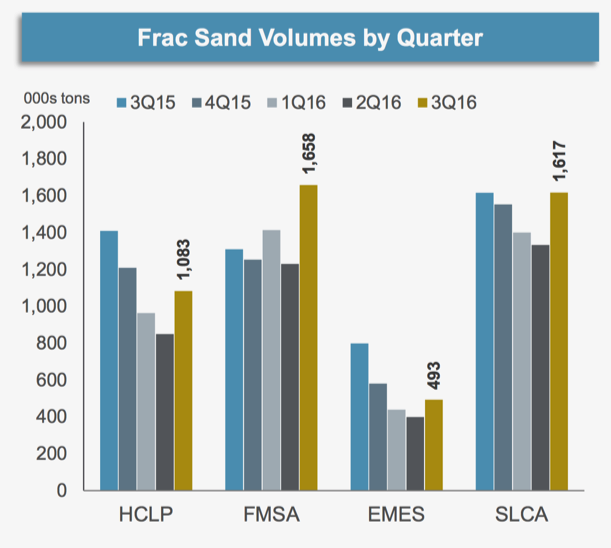

Emerge Energy Services (NYSE: EMES) subsidiary Superior Silica operates 16 transload facilities with 6 being unit train capable and the company is expanding those capabilities in the future. The company has 50% of the railcar fleet active and is continuing to look into last mile logistics solutions to compete with the other large sand providers.

Fairmount Santrol (NYSE: FMSA) highlighted that 70% of Northern White sand was shipped via unit train in Q3’16 showing the demand for unit train capable facilities moving into the new year. According to FMSA more than 65% of frac sand is sold in-basin. The sand providers are thinking ahead and moving product to the Delaware, Midland, SCOOP and Stack areas anticipating demand and reducing the time it takes to get to the wellsite.

Hi-Crush (NYSE: HCLP) announced the launch of PropStream integrated delivery solutions and investment in PropX to provide last mile logistics. The company’s sand volumes increased by 28% from Q2’16 to Q3’16 compared to FM Santrol who increased volumes by 35% during the same period and that trend is anticipated to continue as the price of oil recovers and operators put frac crews back to work.

Source: Hi-Crush Partners January 2017 IR Presentation

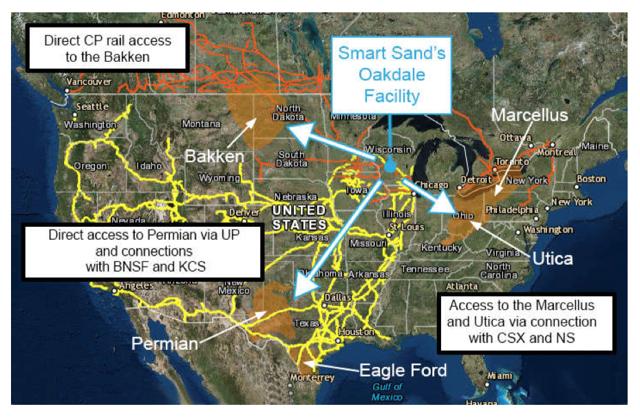

Smart Sand (NASDAQ: SND) filed for an IPO in October of 2016 and operates a sand mine and processing facility in Oakdale, Wisconsin with access to all major basins. Of the company’s current reserve mix at the Oakdale facility; 81% is comprised of 40/70 and 100 mesh Northern White sand. The company expects to develop in-basin transload facilities to reduce delivery costs and have more reliable delivery times.

Source: Smart Sand IR Presentation

Operator demand will strain Permian logistics in 2017

Some key trends in the proppant market going into 2017:

- Pad sizes, lateral lengths, and proppant intensities increase frac sand demand

- Last mile logistics will be a focus for sand companies trying to provide integrated delivery solutions to their customers

- In-basin sales continue to meet short term operator demand

- Regional sand use is expected to play a big role as operators supplement for Northern White to keep costs down

- Longer term sand contracts will become more prevalent as operators try to secure volumes for increased activity, lock in pricing, and

- work directly with frac sand suppliers.

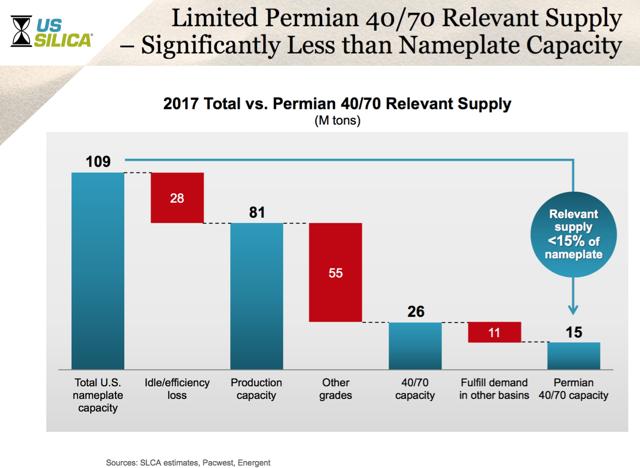

- Pricing dynamics continue with short-term demand spikes similar to current 40/70 shortages and expectations of Q1’17 pricing to increase from $20 to $30 per ton of frac sand

Source: US Silica IR Presentation

Frac Sand companies prepare for 2017 volumes

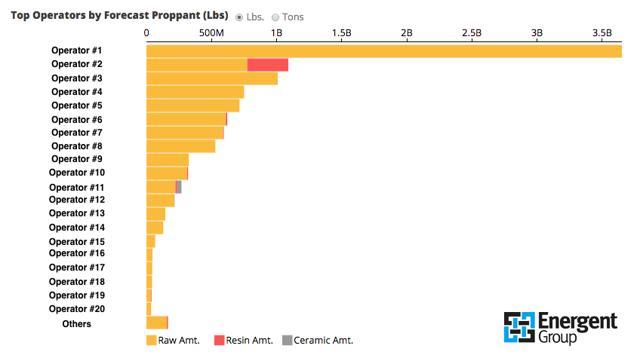

As highlighted earlier sand providers have seen greater volumes being sold in basin which means they need to look ahead. The chart below shows the market potential for one of the most active areas in the Permian where four competing sand providers have transload facilities within a few miles of each other.

All of which will have the same target market of about 35 to 50 miles out from the facilities to profitability deliver sand to the well site. The market potential is comprised from a nine-month trend by operator and the proppant usage along with the assumption that the number of well completions will increase by 50% in the next year. For the focus area in the Permian it is expected that 10.8 billion pounds of proppant will be needed within the next 8 to 12 months. The top three operators will account for about 60% of the proppant needed in the next year.

Source: Energent Group

Overall the frac sand market will be very competitive in 2017 with sand companies making a push for integrated logistics. Demand will continue to be high as sand providers are already seeing shortages due to increased activity but this will balance out. Investors should seek companies that have solid transload networks with last mile logistics solutions as these companies will be become more and more attractive to operators who want to self source. Along with mastering logistics; companies who can create good relationships with service companies and operators alike and deliver product on schedule will fare well in the future.