Originally published in E&P Magazine’s Hydraulic Fracturing Techbook

The modest increase in rig activity is a positive sign that the market is coming back and welcomed by the industry. June 2016 started with level rig activity only to have the largest increase in rig counts that the market has seen in a year, adding rigs week over week. Completion activity continues to fall as operators wait for higher sustainable oil prices.

Source: Energent Group

Bearish scenario at $48 and below: returns industry to 2015

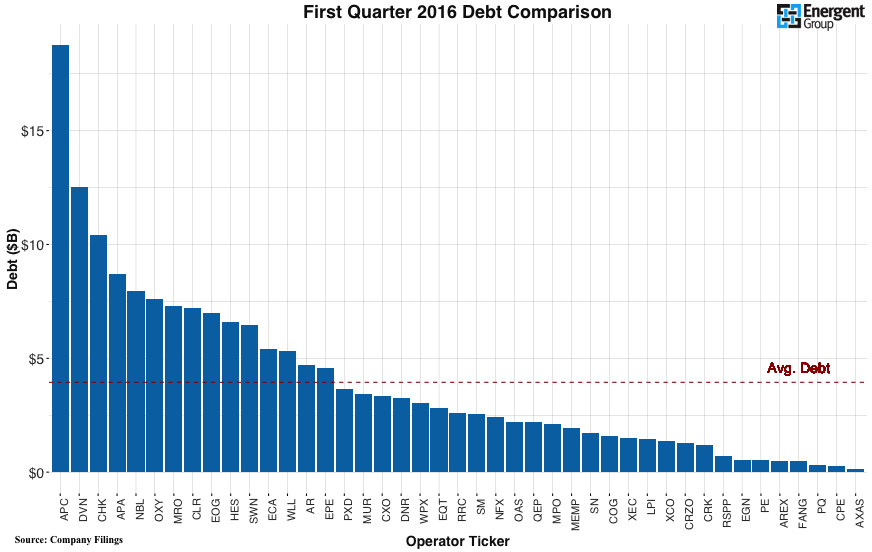

If oil prices hold in the $40 range, expect completion activity to continue to decline with depressed drilling activity. Operator budgets reflect the minimal activity as many would be under large debt loads that require payments. Figure 2 below displays the total debt of selected operators after the first quarter of 2016.

Expect more asset and lease sales from operators with heavy debt loads. In this bearish scenario, operators apply even more pressure on service pricing for well service and supply companies. Memorial Production Partners (NASDAQ: MEMP) announced the divestiture of non-core Permian assets on June 2016. This pressure put on by the operators will continue to drive pricing down for frac crews and day rates for drilling contractors. It is in the best interest for the E&P’s to keep the smaller, regional service companies afloat to keep the E&P’s buying power greater than the larger global service companies.

Expect more asset and lease sales from operators with heavy debt loads. In this bearish scenario, operators apply even more pressure on service pricing for well service and supply companies. Memorial Production Partners (NASDAQ: MEMP) announced the divestiture of non-core Permian assets on June 2016. This pressure put on by the operators will continue to drive pricing down for frac crews and day rates for drilling contractors. It is in the best interest for the E&P’s to keep the smaller, regional service companies afloat to keep the E&P’s buying power greater than the larger global service companies.

Also, many transload facilities will remain full of frac sand as demand and consumption slow. Even with higher intensity fracs and longer laterals, the total demand for frac sand will decrease. Pressure pumpers continue to fight for work, waiting and hoping for higher oil prices.

Lower activity does not help stimulate the Upstream job sector. According to Graves & Company, 350,000 jobs were lost globally due to the falling oil prices. Rig and frac crews remained sidelined with little to no work. Drilling contractors limit hiring and focus on acquiring longer term contracts. Similarly, frac crews in each of the tight oil plays find little relief at these prices. As of May 2016, there are approximately 12-15 frac crews in North Dakota.

The market dichotomy is taking shape. The large public, global pressure pumpers continue to operate crews on razor thin margins or bundle frac services with other services while the smaller, regional pressure pumpers can no longer provide the service at the lower oil prices. E&Ps are trying to keep the smaller regional service companies afloat to maintain their buyer power over larger service company’s supplier power.

Base scenario at $48 to $50: industry fights to find stability

Seeing oil prices improve provides a glimmer of hope for the industry, but it will need to hold for activity as a whole to come back. Just as in May of 2015 when oil pricing improved it very quickly took a turn and continued to dive. In this scenario, if prices can hold for several of weeks, operators will start to complete the backlog of uncompleted wells and possibly look to add rigs to maintain production levels.

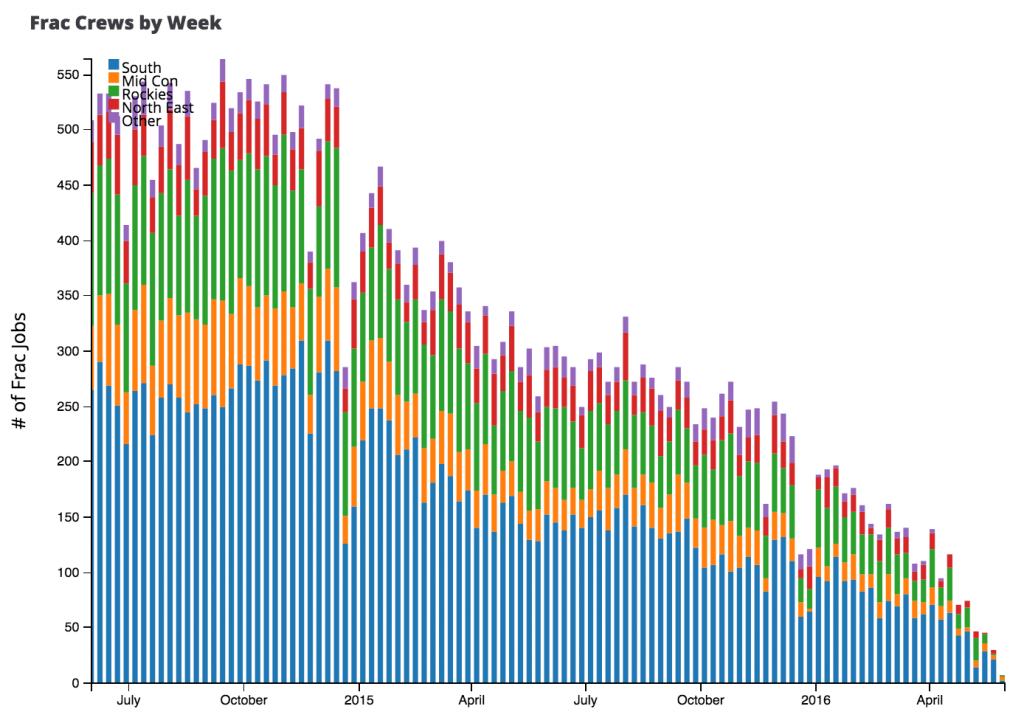

Many operators are profitable in the $40 to $50 range with some able to see attractive rate of return on completing new wells. Other operators will continue to tread water as they try to keep up with the debt loads looking for other alternatives like sales of non-core acreage. This oil price scenario holds activity steady and allow operators to continue with their planned budgets for the year. Figure 3 shows the number of frac jobs across basins.

Source: Energent Group (as of May 2016)

Suppliers and service companies alike start to prepare for increased activity at this level. How will the suppliers ramp up activity? Will there be enough crews and where will they be added? These are essential questions to ask if the pressure pumpers are ready when operators give the green light. At the same time, operators try to lock in today’s service prices before pressure pumpers see increased demand.

Bull scenario at $51 and above: services see new demand

Continental Resources (NYSE: CLR) made headlines in June 2016 when Harold Hamm stated the company is devoting frac crews to their uncompleted Bakken wells. According to Energent Group DUC data, Continental Resources has added 146 uncompleted wells in the last two years. The rush to bring activity back will happen when prices increase $50 and above. Many operators might look to slightly increase budgets and add drilling rigs. Operators with strong balance sheets have already built in room for ramping up activity in 2016. Completion activity will jump as operators look to open the valve and increase production while service pricing is still depressed.

Additional activity and commitments will improve the Upstream labor market. EOG Resources Chief Executive Officer Bill Thomas told investors that $60 oil is required to restart the growth cycle. This growth cycle will require additional frac crews, but it is not clear at this point how quickly crews can be brought back.

Hydraulic fracturing horsepower is available across all basins; however, the limiting factor will be the availability of people and crews. Higher oil prices bring stronger service demand and will likely bring talent back to the industry. Operators and service companies want to see sustained oil prices before making commitments to personnel and equipment.

Proppant market implications

The well services market will react differently to each pricing scenario. At one end of the spectrum, oil prices remain low and pressure pumpers will fight to stay afloat. On the other side, pressure pumpers will struggle to meet the demand of increase activity quick enough with a higher price environment.

The proppant market in the bearish scenario will be over supplied with pressure to reduce costs amid already low frac sand costs. Many customers are looking to buy in-basin to reduce transportation costs forcing companies like Hi-Crush Partners and Fairmount Santrol to move about 5,630 railcars into storage and delay delivery of new rail cars as they are not needed at this time. Hi-Crush has idled their Augusta facility, only running their lowest cost plants.

Source: Energent Group (as of April 2016)

With oil being in the $48 to $51 range proppant suppliers will continue to work with operators to reduce costs and manage their railcar fleets. Operators have moved away from using more expensive products like the ceramic or resin coated proppants still using high quality white sand, some operators have even moved to using lower quality brown sand to reduce costs where they believe it will not hurt production.

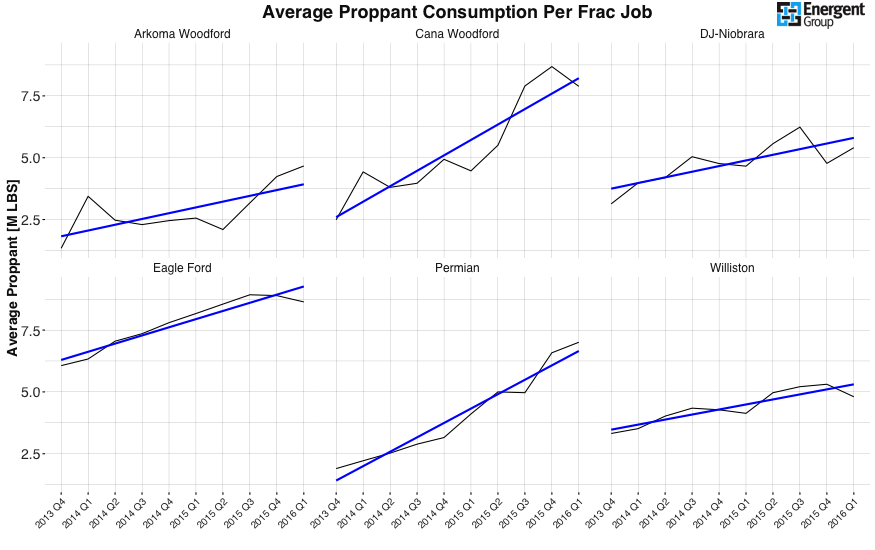

As oil prices improve, the demand will increase substantially due to the increase in proppant used per well which is now on average over 3000 tons per job. The longer laterals and increased proppant per well has likely softened the impact of increased DUCs and lower well completion counts across the U.S.

Source: Energent Group (as of April 2016)

When will operators complete more wells?

Continental Resources’ CEO Harold Hamm stated publicly that the market will see $60 oil by the end of 2016. At that point Continental will complete their DUC inventory waiting for more stability in oil prices before bringing rigs back to work. Pioneer Natural Resources (NYSE: PXD) announced the addition of five rigs in the second half of 2016 adding $100 million to their budget for the year. The two different outlooks by operators show that there is not a clear answer to when well completion activity returns. Each operator looks at these oil price scenarios through their financial, asset, and company lens.

Source: Energent Group (as of April 2016)

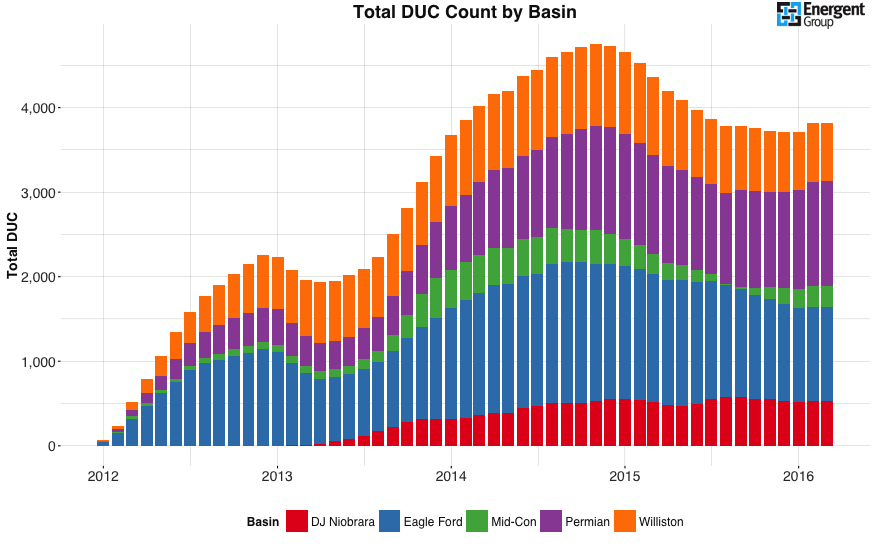

Drilled but uncompleted (DUCs) wells have been a highly debated topic during 2015 and into 2016. Many operators have grown a large inventory of uncompleted wells that still need to be completed. Some wonder if those wells will be completed first and if they will even have a substantial impact to production once they are brought online.

If operators look to draw down the DUC inventories it could fast track completion activity to catch up with an improved oil price environment assuming the crews and capital are there. This stresses the importance of supplier and frac crew readiness during a rebound in oil prices.