The onshore land rig market is now just over two years into the current cycle. North American activity continues to grab the headlines but elsewhere there is plenty of notable market development. Within the supply chain it was evident that rig contractors and service companies benefited early in the cycle from an uptick in activity levels but OEMs struggled with an overhang in supply of rigs and saw new orders stagnate at minimal levels. In recent months we have seen that the fortunes of OEMs in this cycle are now looking much more favourable and reporting of Q2 results in late July and early August has confirmed this view.

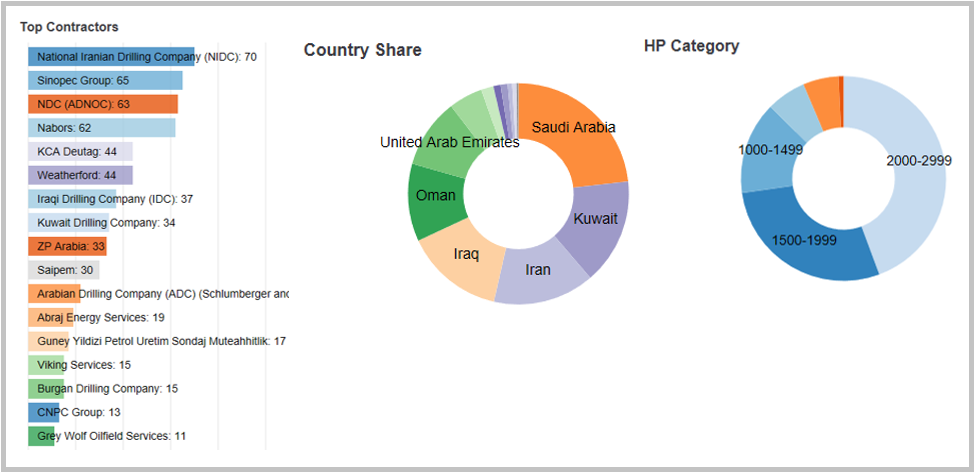

As with other sectors in the oil & gas industry, the land rig market has witnessed a significant amount of merger and acquisition (M&A) activity since the oil price downturn, with contractors and equipment manufacturers aiming to consolidate their presence in regions with strong prospects for growth. The Middle East has emerged as a core area of focus in this respect. Notably, KCA Deutag completed its acquisition of Dalma Energy LLC’s Omani and Saudi Arabian assets in April 2018. Following the acquisition, the company’s land drilling rig fleet has increased to 83 units, of which 44 are located in the Middle East (approximately 53%). More recently, it was reported that Weatherford has entered into an agreement to sell its land drilling assets in Algeria, Iraq, Kuwait, and Saudi Arabia to ADES International Holding, with the latter company aiming to consolidate its presence within the Middle East and North Africa (MENA) region.

Middle East Land Rig Market Top Contractors, Country Share, Fleet HP Category

Middle East Land Rig Market Top Contractors, Country Share, Fleet HP Category

Source: Westwood Global Energy

Nabors Industries Ltd announced back in October 2016 that it had signed a joint venture (JV) agreement with Saudi Aramco to own, manage, and operate land drilling rigs in Saudi Arabia. The JV, known as Saudi Aramco Nabors Drilling Company (SANAD), commenced operations in December 2017, with the two companies having agreed to purchase and operate 50 newbuild rigs over a ten-year period. The JV with Nabors forms a key element of Saudi Aramco’s strategy to develop a local base for world-class industry technology and services and, as such, the rigs acquired by SANAD will be constructed locally. Notably, Saudi Aramco also signed a JV agreement with leading manufacturer and equipment provider NOV to establish a manufacturing and aftermarket facility for land rigs in Saudi Arabia. The facility is scheduled to become operational in 2020 and will have the capacity to manufacture ten newbuild land rigs per year, with the first unit scheduled to be delivered in 2021. In addition to manufacturing newbuild units, it will also offer repair and recertification services for a range of equipment.

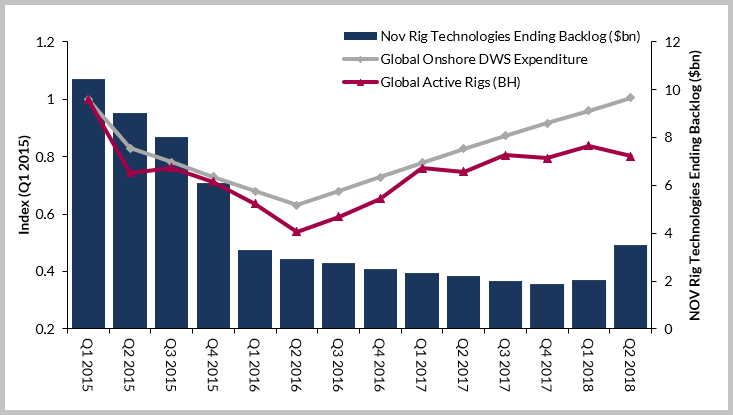

Thus, the NOV-Saudi Aramco JV is indicative of the drive not only to develop a localised set of skills and technology base, but also to ensure that this base covers the full spectrum of the supply chain and rig life, from construction to repair and maintenance. The Nabors and NOV JVs with Saudi Aramco also highlight the important role of the Middle East in terms of supporting growth in the global land drilling rig market over the next few years. The order for fifty land rigs placed by Saudi Aramco in Q2 2018 constituted the largest land rig order ever placed and was sufficient to replenish NOV’s Rig Technologies order backlog to $3.5bn (this was the highest level seen since 2015).

This trend in terms of NOV’s reported backlog is indicative of the wider lag within the market, with rig contractors and service companies being among the first to benefit from the uptick in drilling activity from mid-2016, whilst equipment manufacturers have seen newbuild orders remain stagnant due to the oversupply of rigs within the market. However, as this oversupply begins to be absorbed, and demand emerges for new capabilities in terms of rig technology, the outlook for equipment manufacturers is becoming more positive.

NOV Rig Technologies Ending Backlog ($bn), Global Onshore Drilling & Well Services Expenditure (indexed to Q1 2015, Westwood Global Energy), and Global Active Rigs (indexed to Q1 2015, Baker Hughes), Q1 2015-Q2 2018

Source: Baker Hughes, NOV Segmented Financial Data, Westwood Global Energy

In terms of rig technologies, the Middle East is also becoming a key region for the adoption of drilling technologies already being deployed in the US shale plays, as the focus of Middle Eastern NOCs turns to exploiting the region’s unconventional reserves. Notably, combined output from the System A and B shale gas development in Saudi Arabia is expected to reach just under 50 kboe/d by 2019. Outside of Saudi Arabia, projects such as the development of the Jurassic tight gas fields in Kuwait, involving high pressure, high temperature (HPHT) reservoirs, will also require the use of high-specification, high-horsepower units.

Key technologies within the Middle East will include the use of extended reach drilling, which is already being deployed in the development of the giant offshore Kish field in Iran, as well as multi-stage hydraulic fracture completion and stimulation. As such, contractors within the region are likely to focus on upgrading the existing rig population in order maximise the production and efficiency gains provided by these technologies.

Katy Smith, Westwood Global Energy

[email protected]