An Introduction to the Report

January 2022 marks the launch of Westwood Global Energy’s much anticipated Global Offshore Rig Market Report, offering an in-depth look into the jackup, semisubmersible (semi) and drillship sectors across the globe every quarter. We highlight historic and current market trends with informed insight for the three months prior, along with a market outlook for the year ahead. The report delves into upcoming offshore drilling programmes and assesses rig demand and dayrates in the major drilling regions of North America, South America, North Sea, Africa, Middle East, Southeast Asia, and Australia.

Every quarter Westwood will address a topical theme, with the first one being the announcement in November 2021 of the merger between Noble Corporation and Maersk Drilling. We evaluated several offshore drilling contractor fleets, including Noble and Maersk, to see how the proposed new company will stack up against its peers.

Essentially the report provides readers with context behind the data contained in the RigLogix database and addresses key questions on the rig market. Benefitting from Westwood’s comprehensive suite of offshore platforms, we discuss several demand indicators that drive drilling activity, including operator rig requirements. In addition, offshore exploration drilling from the Wildcat database and offshore field development plans from the PlatformLogix and SubseaLogix databases. Subscribers to RigLogix do not ordinally have access to this extended level of data and analysis.

The Global Offshore Rig Market Report is one of several new insights and tools only available in RigLogix Advanced – an optional upgrade to RigLogix. In addition to the insights offered in the quarterly report, there is also now three new tools available to subscribers of RigLogix Advanced. Our Supply & Demand Scenarios matches requirements and rig availability, whilst Private Requirements allows individual users to add their own requirements or duplicate and amend a RigLogix database entry. Used together, a powerful time saving, competitor analysis, rig selection and opportunity identification toolset. Further to this, Custom Notes brings additional knowledge sharing and collaborative functions to RigLogix, with notes attached to specific rigs, operators, drillers, contracts, or requirements. Private Requirements and Custom Notes will not be viewable by anyone outside of a user’s company, including Westwood. To find out more about RigLogix Advanced, click here.

Key Insights From 4Q 2021

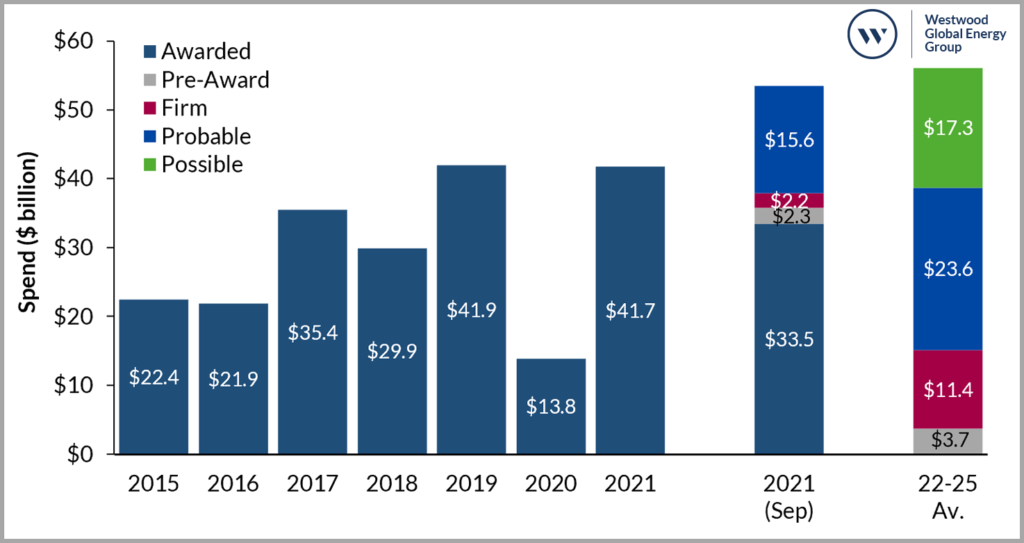

Offshore investment bounced back in 2021 and recovered to pre-pandemic levels, which is encouraging for the offshore drilling industry going forward. Engineering, procurement, and construction (EPC) spend in 2021 totalled $41.7bn, with the last quarter recording $8bn. Year-on-year (YoY) growth was recorded at a 200% increase from 2020.

Figure 1: Offshore Upstream EPC Spend

Source: PlatformLogix, SubseaLogix, Westwood Analysis

As seen in Figure 1, annual EPC spend 2022-25 is anticipated to average $57bn per year. 2022 is estimated to hit above $70bn in EPC spend, the highest since 2013. High profile projects such as Saudi Aramco’s North Dome and QatarEnergy’s North fields in the Middle East, Petrobras’ Buzios, BHP’s Perdido and ExxonMobil’s Yellowtail projects in Latin America, Equinor’s Wisting and Aker BP/Equinor’s NOAKA projects in the North Sea, and PetroVietnam’s Block B project in Southeast Asia, have an anticipated combined spend of $29bn (40% of total spend).

Overall, it was an optimistic end to the year for the global offshore rig market. Global rig contract fixtures, including exercised options, totalled 142 in 4Q 2021, representing 54,829 contracted rig days. This is a 155% increase compared to the previous quarter, which totalled 21,516 rig days awarded.

Global jackup fleet utilization showed a small but steady climb throughout 2021, from 76% marketed utilization in the first quarter to 81% in the final quarter of 2021. Global semi utilization had rebounded until the last few months of 2021. Despite a sharp supply reduction since early 2020, semi demand also fell, finishing the year at 64% marketed utilization, much lower than that of the drillship fleet. Contracted utilization for the marketed drillship fleet averaged 75% in 4Q 2021, representing a near 10% increase compared to the same period last year.

New rig deliveries remain dormant, and the attrition rate has room for improvement. We expect to see more units taken out of service, with the only question being when. Attrition in 2021 was at its lowest level since 2014, with just 33 rigs removed from the fleet, far below the 46 units taken out of service in 2020. With 66 cold stacked jackups still in the fleet, plenty of retirement candidates remain.

What is evident from 2021 is that several major drilling regions appear to have weathered the Covid storm with little fallout, while other markets suffered more significantly. Drilling demand in North America, South America and the Middle East has remained strong since 2019 and they exited 2021 in good shape, and in the case of South America, in even better shape. Offshore drilling in the North Sea, Africa and Southeast Asia has taken a knock, with demand on a downward trajectory since the start of 2020 and hitting rock bottom at the close of 2020. These regions have been on the road to recovery in 2021, although there is still a way to go for Africa. The North Sea and Southeast Asian rig markets look to be back at pre-pandemic levels of rig demand.

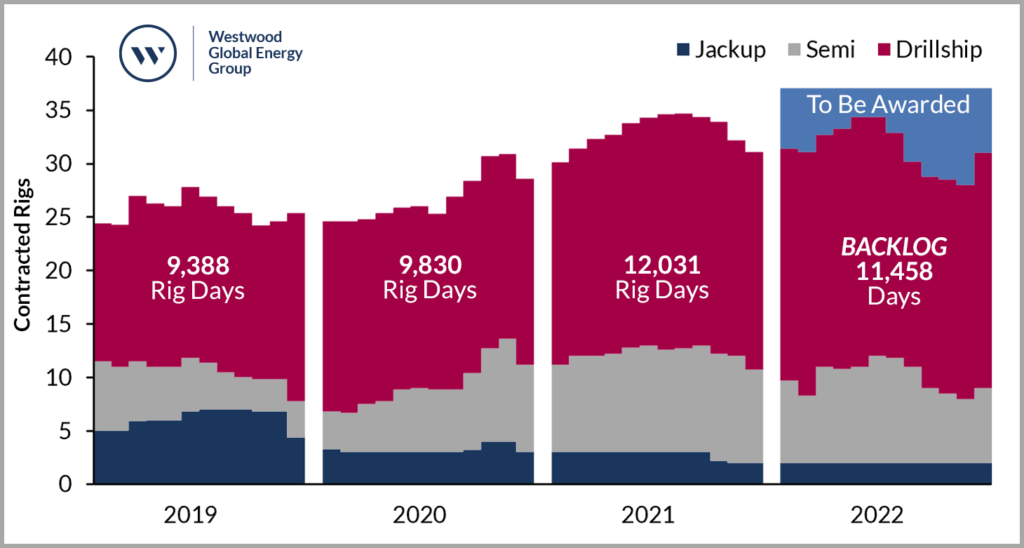

Figure 2: South America Rig Demand Outlook

Source: RigLogix, Westwood Analysis

As seen in Figure 2, South American offshore rig demand remained buoyant throughout the pandemic, with 9,830 rig days in 2020 and an upward trend of contracted rigs compared to 2019. The focus in this region is the floater fleet. Growing demand levels continued in 2021, with 12,031 rig days accumulated by the end of the year, the bulk of which will be covered by drillship contracts. Westwood anticipates further increased demand in 2022, with a yearly average of 37 rigs working and a healthy contract backlog of 11,458 rig days already in place.

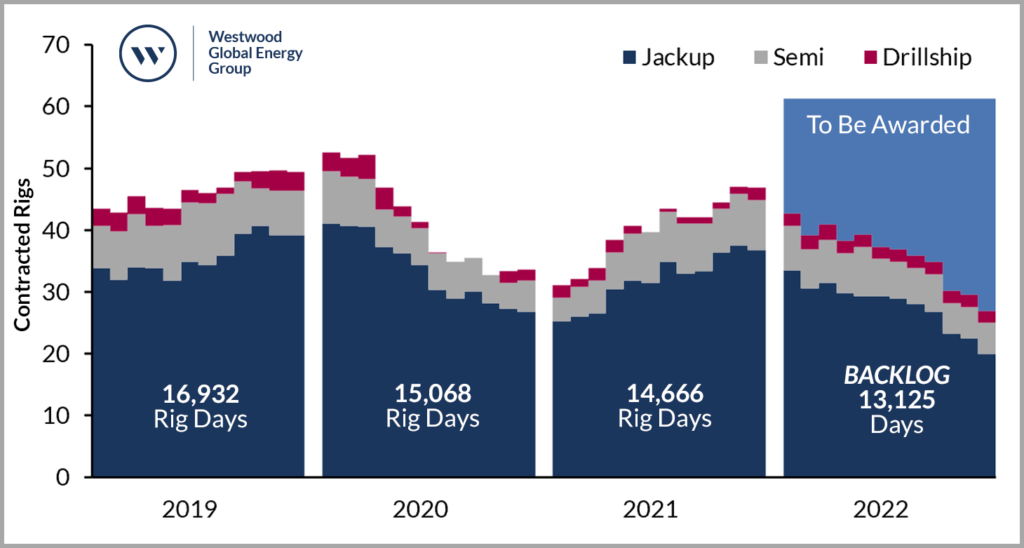

Figure 3: SE Asia & Australia Rig Demand Outlook

Source: RigLogix, Westwood Analysis

As highlighted earlier and seen in Figure 3, offshore drilling demand in Southeast Asia and Australia plummeted in the last couple of years. A total of 15,068 rig days were accumulated last year, dipping to a low in late 2020/early 2021. Activity gained momentum in 2021 with a continued rise in demand through the year. Westwood forecasts this momentum to continue for the year ahead, with 13,125 days backlog in place and a considerable number of prospects in the pipeline, with a substantial number of rig contracts to be awarded.

There is plenty of potential drilling work on the horizon for 2022, and Southeast Asia accounts for the majority of outstanding jackup requirements globally. Drilling campaign start dates are moving targets though, and the numbers presented will change throughout the year as these plans take shape.

Alex Middleton, Senior Rig Analyst

[email protected]