Introduction

On 3 July 2023, the UK Government announced a package of reforms by the UK Emissions Trading Scheme (UK ETS) Authority – the joint body that runs the scheme and comprises the UK Government, Scottish Government, Welsh Government and the Department of Agriculture, Environment and Rural Affairs in Northern Ireland. The UK ETS was launched in 2021 to replace the UK’s participation in the EU ETS, which it had participated in since its inception. In March 2022, the UK ETS Authority consulted on proposals to further develop the UK ETS, including aligning the scheme with the country’s Net Zero ambitions. The consultation resulted in the recently announced reforms which will come into force over the coming years and includes:

- Net Zero aligned Cap: Setting the UK ETS cap to be consistent with net zero. In line with prior commitments, the net zero cap will be implemented from 2024. To ensure a smooth transition to the net zero cap, additional allowances will be released to the market between 2024 and 2027 to ensure that there is no sudden drop in allowance supply between 2023 and 2024.

- Maritime transport, Waste Incineration and Energy from Waste sectors added to ETS: Subject to further consultation on the details of implementation, the scheme intends to expand the scope of the UK ETS to include domestic maritime by 2026, and Energy from Waste and Waste Incineration in 2028 (preceded by a two-year phasing period from 2026-2028).

- Aviation free allocations to be phased out: On the basis there is minimal risk of carbon leakage from the aviation sector, there will be no free allocation for the aviation sector for the 2026-2030 allocation period.

- Expanding the scope of the scheme: CO2 venting from upstream oil and gas industry will be included within the scheme from 2025, referred to as Process Emissions.

In this insight, Westwood reviews the impact some of these reforms, in particular the inclusion of Process Emissions, could have on the offshore oil and gas industry. The analysis leverages data available in Westwood’s Northwest Europe E&P product, Atlas.

Prefer to read offline? Download the PDF here.

UK ETS: Background

The ETS follows a Cap and Trade principle – capping the total level of certain greenhouse gas emissions that can be emitted by sectors covered by the scheme. This limits the total amount of carbon (or its equivalent) that can be emitted. Participants in the ETS are required to obtain allowances equivalent to their annual emissions under the scheme. These can be bought throughout the year in regular auctions or by trading on the secondary market. By creating supply and demand for emissions allowances, an ETS establishes a market price for CO2. As the cap decreases over time, this provides a signal to decarbonise at the pace and scale required to keep emissions at or below the cap.

The scheme further incentivises decarbonisation through a process of buying and selling emissions allowances. Companies that are successful in reducing their emissions can sell unused allowances to other firms. To ensure a company retains its operations within the UK and does not move its operations to countries with less stringent carbon pricing (Carbon Leakage), certain industries receive some allowances for free. The provision of free allowances means an operator needs to buy fewer allowances to cover their emissions, in effect, reducing the carbon price they pay.

The UK ETS applies to regulated activities in energy intensive industries and the power generation sector which result in greenhouse gas emissions, including sites where the total rated thermal input of its combustion units exceeds 20MW. Certain routes within the aviation sector also fall under UK ETS regulations.

Inclusion of Process Emissions from CO2 venting

For the upstream oil and gas sector the EU ETS, and subsequently the UK ETS, previously focused on CO2 emissions generated through the combustion of fossil fuels. In the offshore sector, this was typically a result of the combustion of diesel or natural gas for the purpose of power generation or CO2 generated because of flaring. CO2 that was inherent in natural gas and removed through gas stripping, a process referred to as gas sweetening and required in some circumstances to meet sales gas specifications, has previously been exempt from the UK ETS.

The latest reform will include vented CO2 from the gas sweetening process that is released to the atmosphere either via vent or unlit flare (referred to as Process Emissions) within the UK ETS from 2025. The threshold for inclusion of an installation into the UK ETS for this policy will be 1,000 tonnes (t) of CO2 per annum.

The UK ETS Authority does not intend to provide any additional free allocation of UK allowances to facilities which will be impacted by the change, on the basis that there is likely to be minimal financial impact on the sector and it does not anticipate that this policy will lead to carbon leakage. According to the UK ETS Authority’s response to the consultation, this addition will introduce an additional 0.4 Mt CO2 per annum from the upstream oil and gas sector. For comparison purposes, in 2020 the estimated total CO2 emissions priced within the UK ETS from the upstream oil and gas sector (both onshore and offshore) was 14.9 MtCO2 (Table 6.1, Developing the UK Emissions Trading Scheme, UK ETS Authority, published March 2022).

The impact of Process Emissions on offshore oil and gas hubs

With emissions and ETS prices fully integrated within Atlas, Westwood can conduct rigorous analysis on the impact hydrocarbon prices and emissions performance is having at a field, hub, basin, country and company level.

The UK ETS Authority believes there is likely to be minimal financial impact on the sector. While at a sector level this may be the case, facilities which carry out gas sweetening will see a financial impact. In the offshore oil and gas sector the only hub which carries out gas sweetening offshore and vents a significant volume of CO2 is the Elgin & Franklin Hub. Westwood has assessed the impact the change will have on the hub and concluded that while the increased emissions charge is not insignificant, the impact on the hub’s economics is minimal.

The Elgin and Franklin facilities came online in 2001 and the processing hub was one of the largest HP/HT (High Pressure / High Temperature) installations in the world. The Elgin Franklin complex currently consists of four wellhead platforms (Elgin A, Elgin B, Franklin & West Franklin), with the Elgin A WHP linked to the Elgin PUQ (Process, Utilities and Quarters) platform by a bridge and the Franklin WHP linked by a subsea pipeline. The PUQ is in effect a gas refinery, with gas processing and gas sweetening facilities onboard producing sales quality gas. Gas from Elgin/ Franklin is exported to the Bacton terminal in Norfolk via the Shearwater Elgin Area Line (SEAL) pipeline. Liquids are exported via the Graben Area Export Line (GAEL) pipeline and Forties Pipeline System (FPS). The PUQ was designed to process 547 mmscfd (15.5 Mm3/day) of gas and 175,000 bbl/day of liquids.

The gas treatment facility on the PUQ includes gas sweetening and gas dehydration, with CO2 removed during the sweetening process vented to atmosphere via the sour gas vent. In 2022, this process accounted for 116 ktCO2 (Environmental and Emissions Monitoring System (EEMS) database). At an assumed allowance cost of US$100/t of CO2, this would have been equivalent to US$11.6 million. For comparative purposes, Westwood estimates this to be a c. 7% increase in OPEX charge.

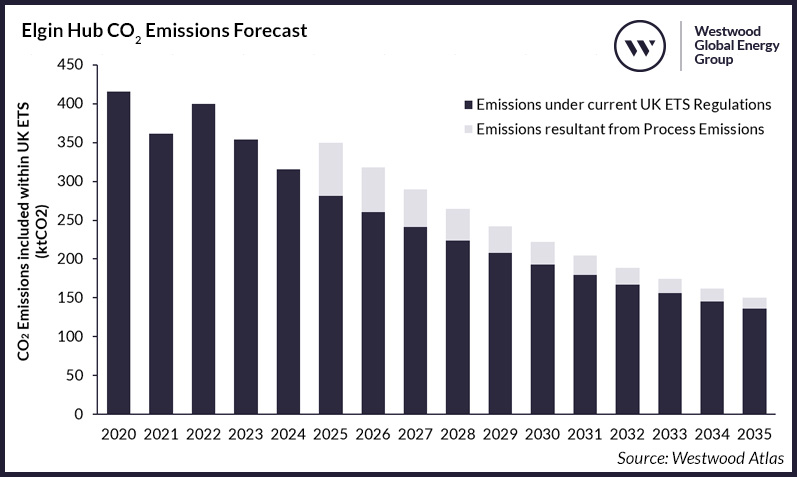

Under the updated regulation, these Process Emissions will now be included within the UK ETS from 2025 and Westwood has modelled the impact of this regulation change. In Westwood’s Base Case price assumption model, the Elgin & Franklin processing hub is expected to cease operations in 2035. Figure 1 shows the expected CO2 emissions forecast for the hub that are included within the UK ETS, with the additional CO2 emissions resultant from Process Emissions highlighted. The impact of Process Emissions is expected to reduce over time due to the declining gas profile and consequently the additional emissions charge in 2025 is significantly lower than the Elgin PUQ would have experienced had the change came into effect from 2023.

Assuming an allowance cost of US$100/t of CO2, Westwood predicts the inclusion of Process Emissions in Elgin will result in an additional emissions charge of c. US$38 million over the remaining operating period, a c. 40% increase (Westwood’s Base Case price assumption model, factoring in free allowances allocated to the Elgin PUQ). In isolation this is not an insignificant figure, however it is less than 2% of the expected OPEX charge over the same operating period.

At US$125/t of CO2 the additional emissions charge increases to US$47 million over the same operating period, <2.5% of the OPEX charge.

Figure 1: Elgin Hub CO2 Emissions Forecast. Source: Westwood Atlas

Further developments to the UK ETS that could impact the oil and gas sector

As part of the consultation on the UK ETS, the Authority asked for early policy thinking regarding the inclusion of methane (CH4) emissions from the upstream oil and gas sector. In its latest update, the UK ETS Authority advised that no decision had yet been made, and that it will consult on any changes in due course. With a CO2 equivalent 28 times higher than CO2 (IPCC Fifth Assessment Report, 2014 (Table 8.7, page 714)), inclusion of methane could have an impact on the upstream oil and gas sector. Total reported methane emissions from the offshore oil and gas industry in 2022 was 23.2 kt (EEMS database), of which 54% is from gas venting and 27% is from flaring. At US$100/t of CO2e this is equivalent to US$65 million.

There is the added complication that methane emissions are traditionally difficult to estimate, especially from flaring. To calculate methane emissions from flaring the typical approach is to estimate the methane volumes based on known volumes of flared gas, referred to as an emissions factor (kgCH4/kg flared gas). The emissions factor in turn has been estimated based on assumed combustion efficiency (methane destruction efficiency) at the flare tip, with industry standards recommending 98% (EEMS-Atmospheric Emissions Calculations Issue 1.810a). However, ongoing research suggests that methane emissions resultant from flaring may be higher than currently estimated and the 98% combustion efficiency could be overly optimistic, with average combustion efficiencies as low as 85% being considered (Energy Environ. Sci., 2026, 16, 295).

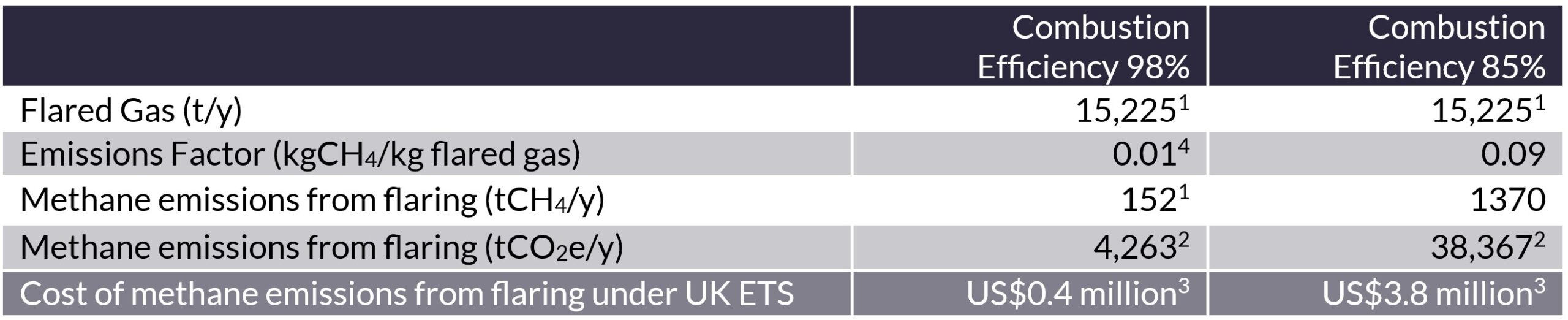

To understand the impact of this potential change, Westwood has included the different scenarios in its Elgin & Franklin hub model. In 2022, the hub reported a total of 1,053 tCH4 of methane emissions, with 152 tCH4 from flared gas and 781 tCH4 from gas venting (uncombusted methane). Total flared gas reported was 15,225 tonnes. A review of the numbers suggests the operator has estimated the methane emissions based on EEMS guidelines which recommends that in the absence of a monitoring system, the default emissions factors for gas flaring of associated gas should be 0.01 kgCH4/kg flared gas (EEMS-Atmospheric Emissions Calculations Issue 1.810a). At US$100/t of CO2e and a CO2e for methane of 28 this would equate to an annual charge of US$0.4 million based on 2022 reported values.

However, a combustion efficiency of 85% could results in an emissions factor of c. 0.09 kgCH4/kg flared gas. If applied to the Elgin & Franklin hub this would result in methane emissions from flaring being 9x higher and an annual charge of approximately US$3.8 million.

Table 1: Potential annual emissions charge associated with methane emissions from flaring on Elgin & Franklin hub under different combustion efficiency scenarios

Source: Westwood analysis

1 2022 Reported values for Elgin PUQ in EEMS

2 Based on methane GWP = 28 kgCO2e/kgCH4

3 Assuming US$100/t of CO2e

4 Default emissions factor for gas flaring of associated gas (EEMS 1.810-Atmospheric Emissions Calculations Issue 1.810a)

Total reported methane emissions from the UK offshore oil and gas industry in 2022 attributed to flaring was 6,365 tCH4. Westwood estimates that if the 2022 reported values were recalculated assuming an 85% combustion efficiency, the equivalent annual emissions charge associated with methane from flaring would be US$160 million. There is a need to further understand the combustion efficiency of methane and currently operators in the UKCS are estimating methane emissions in line with the recommended guidance, however, this does demonstrate the significance of the calculation method if methane emissions were to be introduced into the UK ETS.

Conclusion

The inclusion of Process Emissions from vented CO2 in the oil and gas sector is expected to have minimal financial impact on the offshore oil and gas industry. Elgin & Franklin is the only hub that will see a significant increase in its annual emissions charge. In comparative terms to the hub’s financial performance, the change is minimal.

Of greater potential impact to the oil and gas sector would be the inclusion of methane emissions in the UK ETS, which has the potential to impact every hub. Westwood has demonstrated the impact is particularly sensitive to the combustion efficiency assumed when calculating methane emissions as a result of gas flaring. The UK ETS Authority advised it will continue to review the policy regarding the inclusion of methane emissions and consult on any changes in due course.

Stuart Leitch, New Energies Research Manager

[email protected]