This article was originally published in Offshore Engineer on 25 June 2024 and updated 04 July 2024.

Saudi Aramco’s ambitious post-Covid jackup fleet expansion programme, in which the operator looked to increase its fleet size from approximately 49 jackups in June 2022 to 90 in just two years, seemed a daring feat. But fast forward to March 2024 and the Saudi Arabian National Oil Company (NOC) almost met its target having 89 jackups at work.

To reach this target, the operator awarded 247.8 years of contract backlog during the period January 2022 to December 2023, with the majority of awards being three-to-five-year deals, and some even as long as a decade. The Middle Eastern operator took supply from all over the world, which meant not only Middle Eastern jackup utilisation increased, but so too did the global figure – jumping from 83% marketed committed utilisation in January 2021 to 94% by December 2023.

However, in January 2024 Saudi Arabia ordered Saudi Aramco to halt its oil expansion plan and to target a maximum sustained production capacity of 12 million barrels per day (bpd), 1 million bpd below a target announced back in 2020. Initially it was unclear if the NOC would cut any offshore rig capacity, but following multiple industry rumours, in early April the confirmation of various suspensions started rolling in, finally equating to 22 jackups across eight contractors to date.

Saudi Aramco Jackup Suspensions Overview

Source: Westwood RigLogix

*Only contracts that have been confirmed by the rig manager.

**ARO chose to terminate the remainder of its deal with Saudi Aramco and the rig has since been returned to owner Valaris.

For a full list of rig names and further suspension details access RigLogix.

Although the full terms and conditions of each suspension have not yet been disclosed, it is understood that the majority will be for up to one year apiece and at US$0 dayrate (or another mutually agreed standby rate). The original term of the suspended contracts will automatically be extended for a period equal to the suspension for each rig, preserving the remaining backlog, while the drilling contractors can also market the rig for other work during the suspension or to terminate the remainder of the contract.

Eight affected rig managers

Advanced Energy Systems (ADES), which provides the operator with its largest fix of jackups at 33 units in total was informed five would be suspended. China Oilfield Services Ltd (COSL) and Shelf Drilling will have 44% of their fleet on hire with the operator suspended (four units apiece out of nine). Saipem, which has seven rigs contracted to the operator, will see three units suspended, and Arabian Drilling with nine rigs on hire will also have three units idled. The three remaining companies – Borr Drilling, Egyptian Drilling Company (EDC) and ARO Drilling – were notified of one suspension each.

All these jackups have since begun their suspension periods, with the exception of one Saipem rig and two Arabian Drilling units that were still out working as of 04 July. Working utilisation of the Saudi Aramco jackup fleet has fallen from 100% in March to just 86%, with this anticipated to hit 80% by the end of July when the remaining rigs are expected to start their suspensions. Globally, marketed working utilisation fell from 86% to 82% between March and July 2024.

Furthermore, ARO Drilling-managed/Valaris-owned jackup Valaris 143, which only had approximately seven months remaining on its contract with Saudi Aramco, had its deal terminated by the rig manager. Upon dissolution of the contract, the bareboat charter agreement between Valaris and ARO was also terminated, and the rig was subsequently returned to Valaris.

Re-contracting confidence

However, it is not all doom and gloom. Of the remaining suspended jackups, three of the ADES rigs have already since been re-contracted for work outside of the region – one for work in Qatar, one for Egypt and another for operations off Thailand.

There appears to be confidence from most of the remaining affected rig managers about securing new deals. Borr Drilling, in its latest financial update, stated that it expects its one suspended jackup – Arabia I – to be redeployed in a different region before the end of 3Q 2024. Valaris also stated that it is already in talks with new operators for Valaris 143.

Shelf Drilling, meanwhile, believes it can secure work for three of its four suspended rigs, getting them back into operation before the end of 2024 at attractive dayrates and margin levels. Just last week, two of Shelf’s jackups – Main Pass IV and Shelf Drilling Achiever – were loaded onto a heavy-lift vessel and are understood to be bound for West Africa where new contracts may have been lined up for them. The fourth unit, Shelf believes, could also find new work next year.

Sources indicate that COSL has secured a job for one of its suspended units in Southeast Asia, due to begin in 1Q 2025. Meanwhile, Arabian Drilling has indicated that it is actively exploring opportunities to redeploy its units with other operators during the suspension periods.

In addition, Saipem revealed that one of its suspended jackups was already budgeted to complete its contract around the middle of this year and will be delivered back to the owner. Another unit will undertake planned maintenance and recertification during the suspension period, and the third will most likely be redeployed into a different geographical area substituting another rented unit to be subsequently delivered back to the owner.

Opportunities for redeployment

So where could these remaining idle rigs potentially end up, should their managers choose to bid them elsewhere? RigLogix records a total of 32 jackup requirements at a full tender or direct negotiation stage, that are due to begin in the next year should they move ahead.

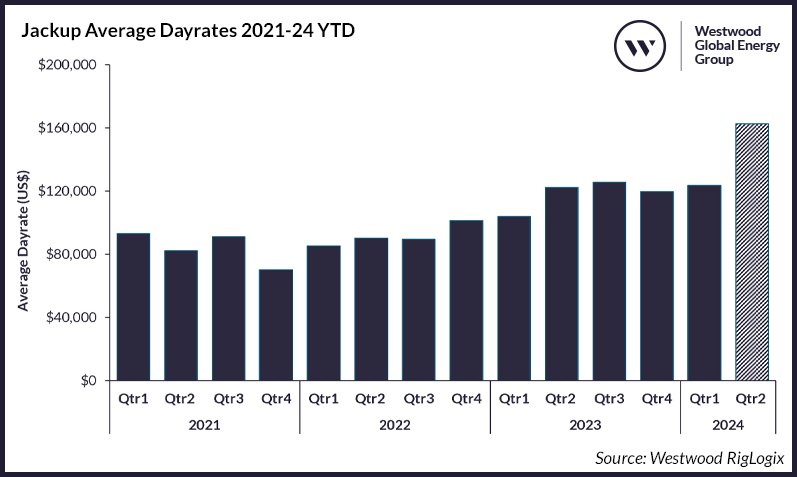

Jackup Average Dayrates 2021-24 YTD

Source: Westwood RigLogix

India, Southeast Asia and Africa appear to be offering up the lion’s share of potential demand days during this period. However, some rumours suggest that due to this new additional supply of jackup capacity in the market, we may see some operators that currently have active tenders out in the market look to cancel and re-tender as they may potentially be offered lower dayrates in the current environment. However, the upward trajectory of dayrates appears to be unaffected year-to-date.

Total remaining term on the suspended contracts comes to approximately 54 years of backlog, or 66 years including options. Of course, some of this has now been terminated and perhaps more will be in the future. It is unclear if those rigs that have been re-contracted outside of the region will return to finish their stints with the Saudi Arabian operator after their new commitments.

Teresa Wilkie, Director of RigLogix

[email protected]