Energy Transition – Framing a business case for hydrogen in Northwest Europe

Hydrogen has both enormous potential but also an uncertain future. As we noted earlier this year, even though the sector is in its infancy, the global pipeline of more than 200 large-scale hydrogen projects is worth more than $300 billion – equivalent to three fifths of 2019 upstream spending. However, the debate on hydrogen’s potential differs in each region of the world – reflecting the different decarbonisation challenges and economic development opportunities they face.

In this insight, we review the status of hydrogen in Northwest European countries, unpack the barriers to the growth of the industry, and discuss the factors that will influence the future role or ‘business case’ for hydrogen in Denmark, Germany, the Netherlands, Norway and the UK.

Northwest European Context

The Northwest region is leading the deployment of hydrogen (and associated CCUS) projects in Europe. The current pipeline of projects around the North Sea reflects the will of governments and existing energy market leaders to protect relevant value chains, such as that of natural gas, while exploring the opportunities of renewable power beyond electrification.

While this has resulted in an increasing support for the upstream (producing) side of the value chain, when it comes to hydrogen, downstream sectors play an equally important if not more significant role in the overall business case.

Renewable energy producers and oil & gas companies are among the key stakeholders in taking the leadership to integrate stakeholders across the value chain. However, while these synergies and collaborations have resulted in an initial pipeline of conceptual projects, only those with a strong facilitator have managed to move the most ambitious projects from concept to FID.

Hydrogen strategies and targets

Broad support for the hydrogen economy in Northwest Europe is reflected in the EU and UK hydrogen strategies that primarily focus on the supply side of this emerging market. The EU’s preference is in electrolysis based technologies (green hydrogen), while the UK strategy (initially) favours the production of blue hydrogen derived from natural gas with carbon capture technology.

In addition to these strategies, 22 EU member states and Norway launched the Important Projects of Common European Interest on hydrogen (IPCEI hydrogen) in late 2020 to support the development of the whole value chain of clean hydrogen in Europe. Similarly, the UK has been supporting the decarbonisation efforts of key sectors through different mechanisms, such as the Industrial Decarbonisation Challenge and the CCUS Cluster Sequencing Process. Access to public and private finance is also much improved across the value chain, partly to help de-risk the earlier stages of projects.

The result has been the emergence of national hydrogen strategies and roadmaps – typically with a 2030 timeframe. Years of research and knowledge-building from demonstration and pilot stages have now been translated into conceptual plans for large‑scale hydrogen production hubs, valleys and corridors.

The question countries and companies across the value chain are now asking is how to ‘tap into’ the opportunity? In Northwest Europe we are seeing a diverse set of stakeholders from the natural gas and renewable energy value chains, ports, industrial hubs etc all trying to make sense of this opportunity – resulting in an equally diverse set of (proposed) projects.

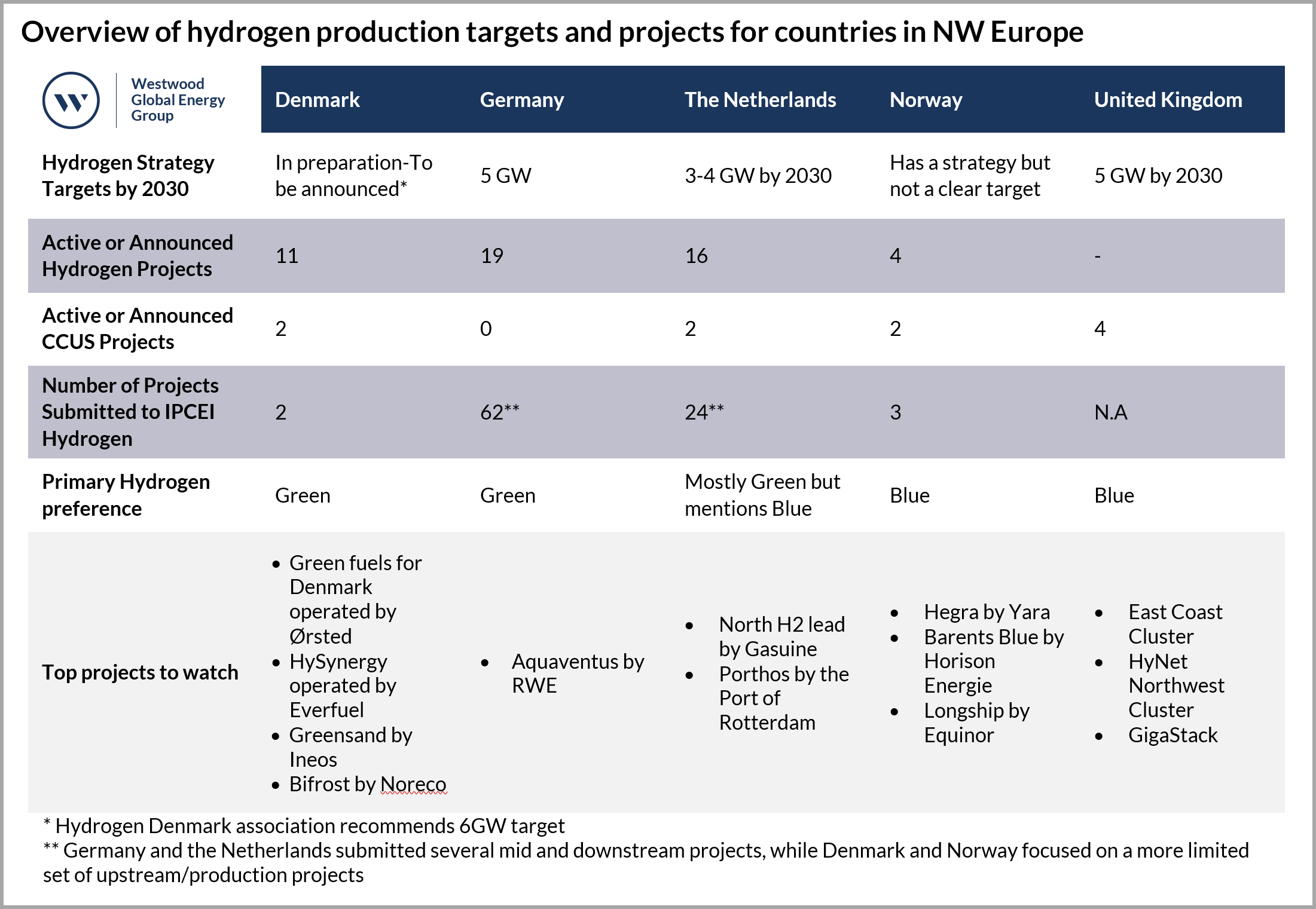

Table 1. Overview of hydrogen production targets and projects for countries in NW Europe. Source: Westwood Analysis

Collaboration to manage risk and complexity

Despite the broad support and a strong project pipeline, sizable barriers exist in turning vision into reality. While the current state of the hydrogen economy could be compared to the early stages of the development of renewable power, the hydrogen value chain is in fact significantly more complex. There are multiple stakeholders, regulatory, technical and commercial hurdles, as well as safety concerns, to overcome.

The biggest hurdles to overcome include the current high cost of green and blue hydrogen that does not make it an automatic economic alternative, as well as regulatory uncertainty around the standards for ‘low carbon’ hydrogen that create uncertainty for some of the most important blue hydrogen-based projects.

Governments have been working to fill policy gaps and provide confidence to investors and stakeholders involved, including harmonised standards, and proposed financial subsidies for the scaleup of electrolysers. But to manage this risk, the key theme that emerges in all projects is ‘collaboration’ among stakeholders, and the search for synergies across the value chain to overcome the barriers that limit the deployment of blue and green hydrogen to the current and future demand sectors.

Selecting the right route to commercialisation

The complexity of the hydrogen question is partly driven by the multiple potential uses of hydrogen in a country, and how these are ‘supplied’ – which will depend on the presence of an existing natural gas value chain, the availability of renewable power, as well as the sources and sinks for CO2.

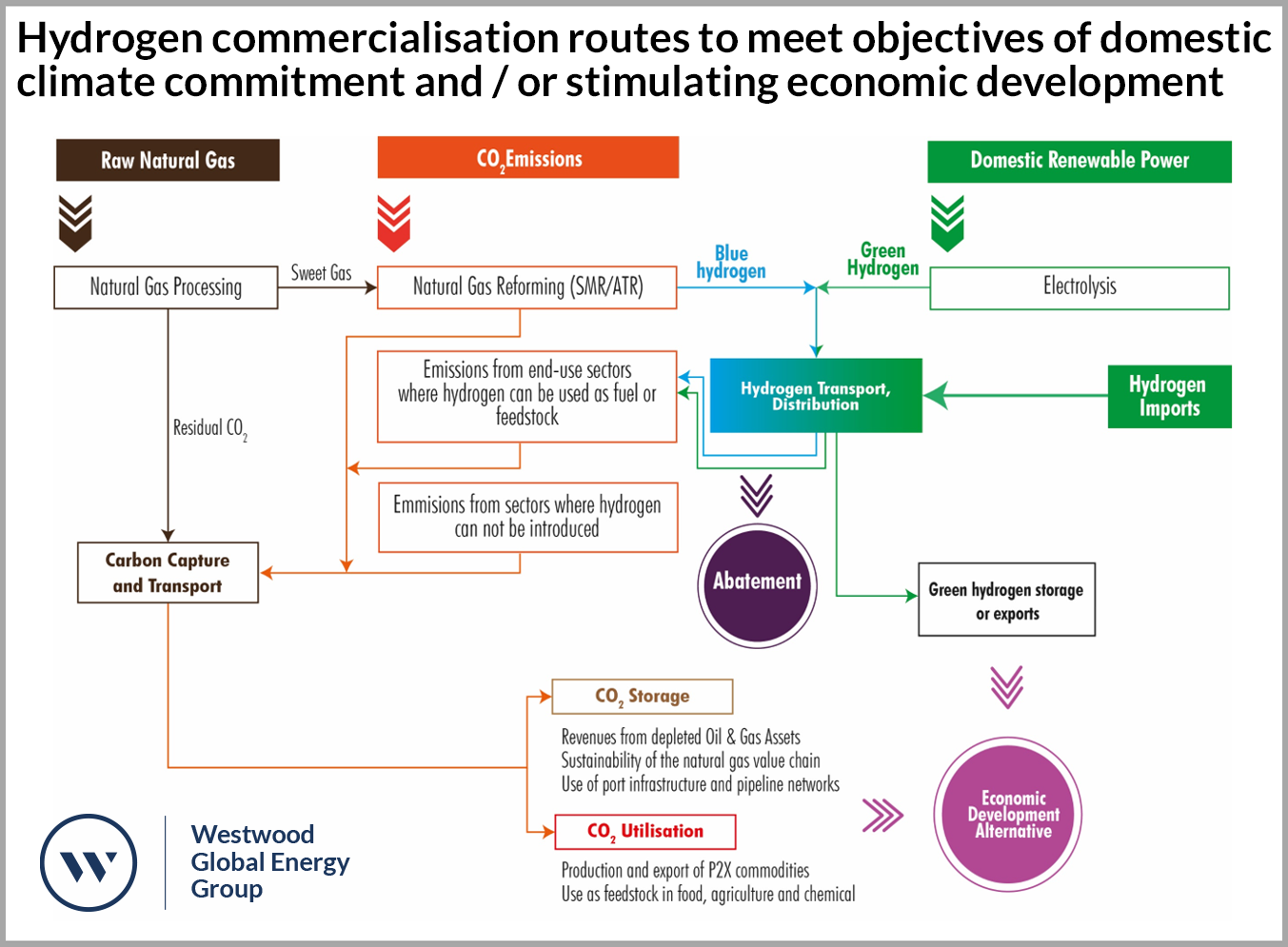

The strategic objective of a hydrogen project should be either to support a country in meeting its domestic climate commitments or stimulating economic development (e.g. exports). The schematic in Figure 1 highlights the breadth and complexity of the commercialisation routes for hydrogen.

Figure 1. Hydrogen commercialisation routes to meet objectives of domestic climate commitment and / or stimulating economic development. Source: Westwood analysis

The key challenge then is in selecting the right commercialisation route for each country. While cost is a consideration and strategic support by a country is essential three influencing factors have been identified to making a business case for hydrogen a reality:

- Matching the opportunity of hydrogen with a country’s needs

- Identifying synergies and collaboration opportunities

- Determining a business case facilitator

Acknowledging these influencing factors can help in the initial design of a project and move projects from concept to FID.

Matching the opportunity of hydrogen with a country’s needs

The versatility of the hydrogen molecule allows for its potential application in a wide range of sectors, including steelmaking, chemical processes, refining, and a broad spectrum of Power-to-X (P2X) commodities. Heating in homes and transport are also much discussed applications. Its versatility and possible outsized impact in supporting the decarbonisation of our economies has been hailed as a ‘game-changer’ for the road to net-zero.

The challenge to hydrogen is whether it is the appropriate decarbonisation solution, and if so, where its use should be prioritised. Consideration needs to be given to the following:

- Structural barriers: Some ‘hard to abate’ sectors would require a too significant structural change to make hydrogen a technically and / or commercially feasible option. In the steel sector for instance, to create a sizable (and economic) enough demand for hydrogen in their operations, European producers will likely have to abandon their Blast Furnaces and move to a Direct Reduced Iron (followed by Electric Arc Furnace) process.

- Alternatives: End-use markets are currently weighing up the various alternatives available to decarbonise their operations, whether it be electrification, hydrogen, CCS etc. The final ‘choice’ is not set in stone and will evolve. For example, The Athos CCS project in the Netherland was cancelled, after the project partner Tata Steel opted for Direct Reduced Iron route (with hydrogen as a reducing agent) to decarbonise its operations.

- Demand: Hydrogen markets face a chicken and egg dilemma. While countries like Denmark and Norway have the potential to produce hydrogen, the lack of clarity on its ultimate end-use potentially holds back the necessary investment in renewable (or natural gas) energy sources needed to support this. Imports can offer a solution, but again, clarity on the end use market is important to warrant this. Vice-versa, end use markets won’t develop until hydrogen is viewed an attractive alternative.

Identifying synergies and collaboration opportunities

Once the appropriate target end-use sectors have been selected and there is more clarity in the downstream part of the value chain, projects leaders (typically on the supply side) can determine which other stakeholders need to be involved and build synergies through collaboration. Aligning the stakeholders strengthens the business case.

For example, Denmark identified the transport sector as its main target for decarbonisation and therefore engaged with the biomass and waste-to-energy value chains, from where captured CO2 can be sourced and a P2X industry created (particularly in synthetic fuels). Projects are further engaging with district heating opportunities to generate additional revenues from residual heat. P2X exports can also provide an economic alternative for the excess hydrogen the country can produce.

In the UK, synergies are being created between key emitters (e.g. heavy industry, the power sector) and the oil & gas sector. This takes advantage of the availability of depleted oil and gas fields in the North Sea close to industrial sites (or ‘clusters’) for the generation of blue hydrogen and the storage of CO2.

Determining a business case facilitator

The initial effort of project leaders and governments looking to develop an opportunity for hydrogen requires a further element: a business case facilitator. Denmark offers a good example of this. The close collaboration of industry associations Wind Denmark and Brintbranchen (Hydrogen Denmark) – together known as the P2X Alliance – has provided a consistent and aligned voice for stakeholders in hydrogen and P2X. This has been essential in framing a business case for hydrogen in a country with low domestic demand, but with vast resources and the need to seek for economic alternatives to its oil & gas business. Several P2X projects owe their progress to this alliance. An overview of the Danish business case is provided in the Appendix (available in the PDF download).

Essentially a business case facilitator helps align a particular proposal/project with the government strategy to address its domestic emissions or create a new economic development opportunity. However, the facilitator also allows for a quicker and more focused identification of policy gaps in the value chain of a project. As a result, governments can develop financial and regulatory mechanism that meet the actual needs of a hydrogen or hydrogen and CCUS proposal aiming to effectively decarbonise prioritised sectors.

Conclusions

There is broad support for both blue and green hydrogen in Northwest Europe – backed-up by regional and country strategies and targets, as well as a strong pipeline of proposed projects.

Each country has its own unique context, objectives and approach in decarbonising its economy. Consideration needs to be given to all parts of the value chain to understanding what role hydrogen can play and how it can be commercialised.

The complexity associated with developing hydrogen projects can be managed by matching the opportunity of hydrogen with a country’s needs, identifying synergies and collaboration opportunities across the value chain, and crucially, determining a business case facilitator – that creates alignment and supports the development of country / project specific support mechanisms.

David Linden, Head of Energy Transition

[email protected]

Ricardo Grandas-Vargas, Research Analyst

[email protected]

To download this report as a PDF, which includes the referenced Appendix, please put your email in the field below and a PDF copy will be emailed to you.