This insight is excerpted from the executive summary in the first of a series of thematic reports produced by Westwood and available to WindLogix subscribers as part of our enhanced coverage of commercial and investment themes in the offshore wind sector. The report examines how the offshore wind support mechanism landscape has changed over the years, as well as the dynamics and pressures that have driven, and continue to drive, these changes.

The story so far

Offshore wind has historically been dependent on government subsidies, and this is still the case for the vast majority of projects, although support levels have generally declined over the past 10 years as project economics have improved due to economies of scale. Even ‘zero subsidy’ projects usually receive some indirect financial support, often in the form of the grid operator funding the construction of the export cabling.

Most subsidies take the form of a revenue stabilisation mechanism, with the government ensuring that the developer receives a fixed (or minimum) price per unit of power it provides to the grid, regardless of the prevailing market price. As the share of offshore wind and other renewables in the electricity mix has grown, governments have increasingly focused on designing subsidy mechanisms that are highly integrated into the merchant power market in order to avoid the creation of a bifurcated marketplace.

At the beginning of the offshore wind industry, most subsidies were ‘relatively’ modest, with governments tapering support during the 2000s. However, this slowed investment in capacity and new subsidy mechanisms were designed with the primary purpose of encouraging private sector investment by stabilising future project revenues. The most prominent of these new subsidies was the UK’s Contracts for Difference (CfD) scheme, with similar schemes implemented in a number of other countries in the following years.

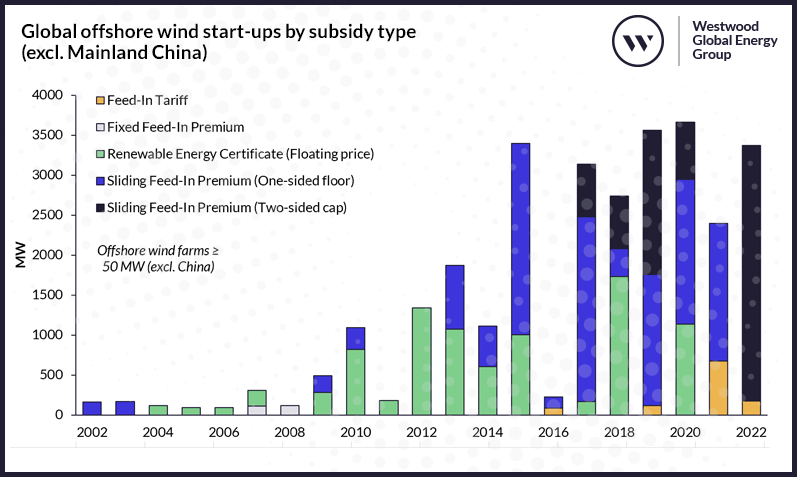

Global offshore wind start-ups by subsidy type (excl. Mainland China)

Mainland China data omitted here for analytical clarity; is featured elsewhere in report

Source: WindLogix, Westwood Analysis

These new subsidy mechanisms were successful in growing demand to invest in offshore wind projects. This increased competition, combined with the economies of scale provided by advancements in turbine technology, empowered governments to reduce support levels, often facilitated through reverse auctions. Given current inflationary conditions, it is unclear if developers will be able to continue to reduce their requirements for subsidy.

Wants and needs

Offshore wind subsidies have generally been subject to two masters, viz national energy policy and the financial needs of projects. The latter of these is relatively straightforward, with governments having been able to reduce the amount of subsidy on offer as the economics of offshore wind projects have improved and competition for subsidy has increased. Whether this can continue is, however, another story. Even the much touted ‘zero subsidy’ projects have benefited from some form of reduction in financial burden by the government.

National energy policy is a more complicated issue. When governments have wanted to stimulate investment in offshore wind, they have done so by providing (comparatively) more generous subsidies. Offshore wind must, however, also compete against other technologies, which may rise and fall in popularity. In the UK, offshore wind benefited from significant government backing at the same time that onshore wind became increasingly controversial due to objections over land use. In the US, offshore wind competes with well-established onshore wind and solar industries, and offshore projects have tended to receive their greatest backing from coastal communities with local industries that stand to benefit, and from proponents of faster progress towards climate goals. Mainland China has, by contrast, offered substantial support to offshore wind projects in recent years, but has now terminated these programmes in the expectation that offshore wind becomes competitive with other well established renewable generation sources.

Going through changes

Many offshore wind subsidy programmes have proven remarkably effective at stimulating investment in recent years, but there are, inevitably, new challenges and opportunities emerging. Perhaps most importantly, governments continue to push for further reductions in subsidy while developers see limited returns on investments, and much of the supply chain remains under severe financial pressure. This comes at the same time there is the challenge of repeating the successes of the past decade in the fixed bottom sector of floating wind.

As the power mix shifts and offshore wind accounts for a greater share of generation, subsidy recipients and designers will have to adapt to new circumstances and greater regulatory scrutiny. Farms that previously received subsidy and were insulated from the wholesale market may face merchant tails that take place in a new power market paradigm, with more storage, more Power-to-X and more interconnection between countries. Developers will have to continue to monitor their commercialisation strategies closely as the wholesale market evolves around them.

For access to the full report, WindLogix and underlying data, please contact [email protected].

Peter Lloyd-Williams, Senior Commercial Analyst – Offshore Wind

[email protected]