Westwood’s latest report for Offshore Energies UK (OEUK) provides a detailed assessment of the UK’s domestic gas production and its role in supporting energy security. It is designed for policymakers, operators and industry stakeholders, highlighting how sustained domestic production underpins reliable supply, supports jobs across the UK, and reduces reliance on imported LNG.

Download a free copy of the full Westwood OEUK report, here.

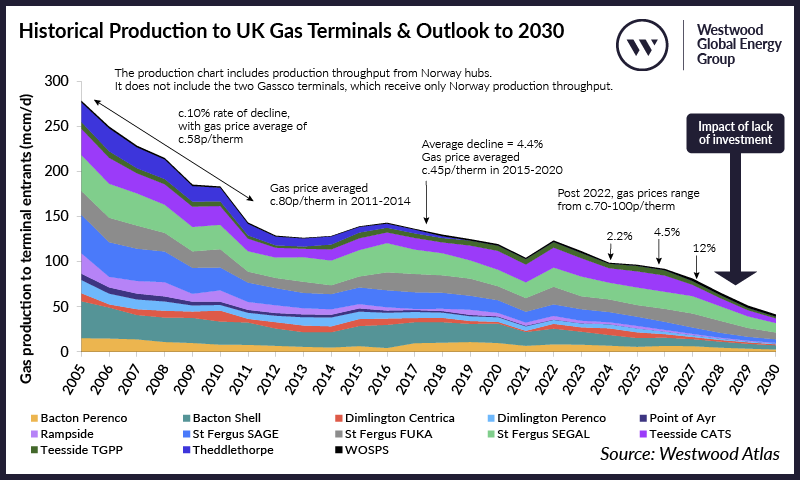

Domestic gas remains critical

Natural gas will continue to play a central role in the UK’s energy system for the foreseeable future. NESO’s 10-year forecast shows demand at 53.6 bcm in 2026, easing only slightly to 53.3 bcm by 2035 – demonstrating its ongoing importance for heating and power generation.

UK produced gas still supplies a substantial portion of national demand. Based on NSTA statistics, UK domestic production accounted for 43% of annual gas supply between 2020 and 2024. Norwegian imports, predominantly piped imports, accounted for 35%, LNG, primarily from the US and Qatar, accounted for 21% and <1% from other sources. If the contribution from domestic production falls, increased LNG imports will be needed to fill the supply gap. Domestic gas remains important for three fundamental reasons:

- Economic contribution: The sector supports 115,000 UK jobs[1] across offshore operations, supply chains and onshore terminals. Early field and terminal closures threaten employment, skills and decades built industrial capability, which will impact the associated tax receipts from both companies and individuals.

- Lower emissions intensity: UK produced gas has a GHG emissions intensity of 28 kgCO₂/boe – far below LNG imports at 85 kgCO₂/boe[2]. Newer UK field developments have an even lower emissions intensity, aligning more with Norwegian piped gas, which 8 kgCO₂/boe.

- Energy security: Domestic production arrives at UK terminals for supply into the UK National Grid. LNG imports must be bought on a competitive global market, and supply could be disrupted by international geopolitics.

Historical Production to UK Gas Terminals & Outlook to 2030

Source: Westwood Atlas

A system under pressure

Despite its value, the UK’s ability to sustain domestic production is being challenged by lack of investment which is the result of current fiscal conditions. Maintaining UK gas and oil production is challenging, but since 2013 the sector arrested the steep rate of decline prevalent since 2001 through continued investment. Production rates are again entering a steep decline with investment sentiment at an all-time low resulting from a fiscal policy to maintain a windfall tax in non-windfall price conditions. The Energy Profits Levy (EPL) was introduced in June 2022, when the oil price was US$122.7/bbl and gas prices were rising to a record high of 451 pence/therm in August 2022. The EPL adds 38% to the base tax of 40% for E&P companies in the UK and is currently legislated to remain in place until 31 March 2030, despite both oil and gas prices returning to normal levels – US$65.4/bbl and 88 pence/therm in January 2026.

The drop in investment is evidenced by a significant drop in development drilling. The NSTA data shows that 41 development wellbores spudded in 2025, down from the 74 in 2020. No exploration wells spudded in 2025, a statistic not seen since 1964, and many new field developments are being delayed. Without ongoing investment, production decline rates are accelerating meaning that many hubs could face premature cessation.

Impact of Reduced Investment – Fields Ceasing Production to 2024. Note: This does not take into account the economics of maintaining pipeline infrastructure.

Source: Westwood Atlas

This decline is made more fragile by the UK’s highly interconnected infrastructure. UK gas production arrives at 12 onshore processing terminals, located across the UK from Shetland to Bacton, supporting regional jobs, skills and supply chain capability. Most fields rely on both gas and liquids export systems, meaning the health of oil infrastructure directly affects gas flows. In 2025, 75% of gas throughput volumes were produced from fields which also relied on a liquids pipeline system. If key liquids infrastructure closes early, linked gas production may also be forced to shut down, risking a wider “house of cards” effect.

External factors add further pressure. Norway remains a dependable partner, but its basin is maturing, with two of three official future production scenarios showing steep post 2026 decline. The UK cannot assume future shortfalls will be offset by Norwegian imports. Meanwhile, limited gas storage – just 3.1 bcm, or 10–16 days of demand – leaves the UK exposed to winter peaks and global market volatility.

Opportunities and the path forward

Despite these challenges, significant opportunity remains across the UK Continental Shelf. Subsurface potential exists from mature Southern North Sea fields to large undeveloped West of Shetland resources, such as the Northern Gas Hub. Recent discoveries – including the 2023 Pensacola find – show that new areas still hold promise. There are opportunities in the subsurface to improve the production outlook for the UK. These would make business sense for investment with the right fiscal conditions. The limiting factor for the UK is not geology but investment conditions. With global portfolios to prioritise, investors require predictable and competitive terms to commit capital to UK developments.

Maintaining domestic supply is essential to a balanced energy supply. Gas demand will remain significant throughout the 2030s, even as renewable capacity expands. Without renewed investment – supported by a competitive tax policy – UK output will decline, increasing the reliance on LNG imports, raising emissions and losing UK jobs, at a time when the country is behind target for the ramp-up of its renewable energy sector.

Sustaining domestic production, while accelerating renewable energy growth, offers the most secure, lowest carbon and most economically resilient path for the UK. The opportunity is clear: with the right conditions, domestic gas can continue to protect jobs, underpin energy security, and therefore support a managed, dependable transition.

Yvonne Telford, Research Director – Northwest Europe

[email protected]

Matthew Belshaw, Senior Analyst – Northwest Europe

[email protected]

Download a free copy of the full Westwood OEUK report, here.