The State of Exploration report is published at a time which may come to be seen as a watershed moment in the global energy industry. The drop in oil demand and crash in the oil price associated with the Covid-19 pandemic combined with the reality of the energy transition underway has made many oil and gas companies rethink the strategy of their entire business. Exploration is a part of that. The 2016-2020 period, covered in this report, saw exploration activity levels beginning to rebound after the oil price crash of 2014.

Then things changed.

Exploration in 2020 actually proved more resilient than many expected, with the HI well count down 26% and discovered volumes down only 3.5% year on year, a much better outcome than was imagined in the middle of the year. 2021 is expected to see a similar well count, as wells deferred from 2020 for operational and budgetary reasons are drilled.

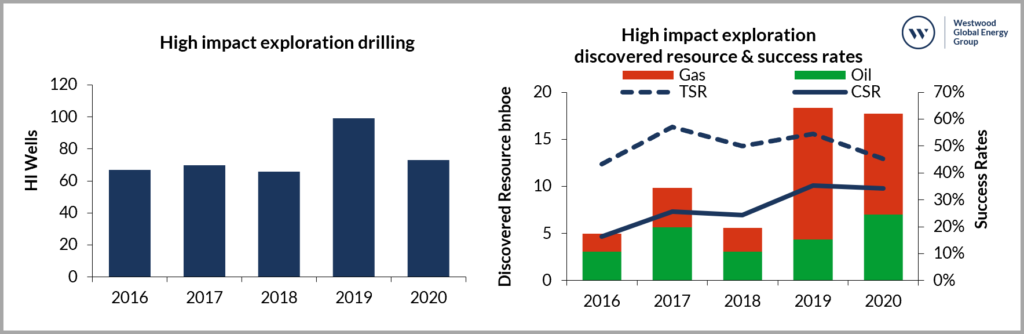

High impact exploration drilling, discovered resources and success rates 2016-2020

Looking further ahead, the past may not be the best guide to the future. Exploration is under scrutiny as never before given falling future oil and gas demand projections under net zero carbon emissions scenarios.

So, what are the key themes that have emerged from the last five years and what are the implications for the future State of Exploration?

High impact exploration in 2016-2020 delivered 56bnboe of discovered resource split 41% oil and 59% gas, with 91 commercial discoveries >100mmboe. Overall discovered resource fell only 23% compared to 2011-2015, despite 46% fewer wells. However, 42% of the volume was in 12 discoveries in Russia and Iran in 2016-2020, and excluding these countries the overall decrease would be 53%.

Less drilling but stable performance in 2020, with high impact wells down 26% to 73 in 2020 but commercial success rates stable at 34%. Total discovered resource was 17.7bnboe, down by only 3.5%, buoyed up by giant discoveries in Russia at Vikulkovskaya and Ragozinskaya in the South Kara Sea, and West Irkinsky onshore Western Siberia. Outside of Russia, the largest discoveries were at Tuna in Turkey and Kwaskwasi in Suriname.

The company landscape is increasingly dominated by Supermajors and NOCs, as the contribution to activity by the medium and small sized companies fell to only 19% of high impact well equity in 2020 vs 34% in 2011-2015. Nine of the 10 most active explorers in 2021 are expected to be Supermajors or NOCs, with the five Supermajors alone expected to take 29% of high impact well equity.

Emerging play options are shrinking, with over 50% of emerging play wells planned for 2021 in Suriname-Guyana. Frontier drilling levels are anticipated to remain low in 2021 and frontier commercial success rates remain challenging at 6% in 2016-2020. New emerging oil plays are likely to be in proven basins and limited in scale – no significant new oil play has been discovered since Liza in 2015.

Cycle times reducing and Infrastructure led exploration (ILX) drilling increasing, with the average time from high impact discovery to FID halving since 2008 to less than three years, and ILX accounting for more than 50% of the exploration budget in 2016-2020. An ILX led exploration strategy has proven to be more predictable than one with less ILX, but discoveries have been an order of magnitude smaller.

70-90 high impact exploration wells are expected to complete in 2021, with activity weighted to the second half of the year and roughly 50% of the wells located in Mexico, Brazil, and Suriname-Guyana. Some of the key wells to watch include Venus offshore Namibia, Pelles offshore Canada, Cutthroat offshore Brazil and Silverback, which is currently drilling in the US GoM.

This is a critical time for exploration without question, with the IEA’s recently released road map to net zero in 2050 concluding that under this scenario no new exploration or project sanctions will be needed to meet future oil and gas demand, laying down the challenge for policy makers and industry as we head towards COP26.

The State of Exploration report found no evidence of a systematic change in industry exploration strategy yet in response to the Energy Transition in the 2016-2020 period, nor in plans for 2021. There has, however, been an increasing focus on shorter cycle exploration set in train following the 2014 oil price crash.

The industry will need to digest the IEA’s new modelling and decide how to respond. In the meantime, explorers will have to focus even more on short cycle, low cost, lower emissions oil and gas opportunities.

For more information on how to access the State of Exploration 2021 report, click here.

Jamie Collard, Senior Analyst

[email protected]