During the first half of 2017, there were over 15 mines permitted or approved by Texas regulators. The sand rush of 2017 turned investor eyes towards the frac sand business. Private capital supports many of the new companies entering the West Texas sand market.

The summer of sand

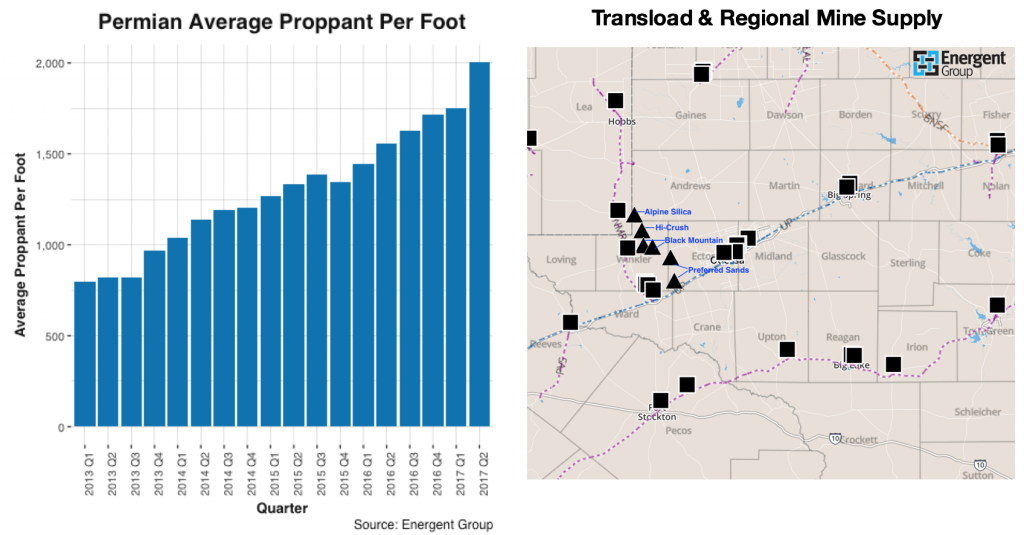

Frac sand companies aggressively leased and acquired positions in the heart of the Permian Basin in (and around) Winkler County Texas.

The large public companies, like US Silica, Hi-Crush, and Fairmount Santrol announced mines coming online from October 2017 to Summer of 2018. According to Hi-Crush, the mine’s nameplate capacity is 3 million tons. Fairmount Santrol announced annual capacity of their Winkler mine at 3 million tons of primarily 100 mesh sand.

Unimin, Preferred Sands, and several other private companies are securing positions in the frac sand rush. Preferred Sands, for example, will open three mines in Texas during 2018 bringing 9.6 million tons of capacity, based on company filings. According to a Unimin press release:

Unimin expects the plant to be operational by early 2018, and has received commitments from customers to support the investment. This project follows several other capacity expansions at key facilities which will be commissioned in 2017.

First mover advantage and long term contracts are particularly important as companies seek key positions near the Delaware and Midland Basin within the Permian. Vista Sand will open the first unit train capable transload facility in Pecos Texas. This small town in west Texas will become the logistics hub for the Delaware Basin.

More trucks, transloads & logistics

The local in-basin sand mines will not require rail cars to transport the sand to transload facilities. Instead, each mine will be prepared with truck load-out capabilities. Trucking prices have already increased 35% from August 2016 to August 2017. With additional mines expected in 2018, frac sand companies are locking in longer term contracts for logistics.

The Permian Basin is now approaching 2,000 pounds of proppant per lateral foot.

In the Permian, there is little worry about sand demand slowing. The frac sand plateau is not happening across all basins. Although companies are reporting E&P’s using less sand, those E&Ps are likely not in the Permian.

However, questions remain for frac sand producers:

- How much of the planned nameplate capacity will come to fruition in 2018?

- What mines have the capital and patience to compete in a crowded market?

- What completion design trends may impact today’s planned nameplate capacity?

- Are E&Ps evaluating frac sand alternatives due to increased frac sand spend?

- Who will make strategic acquisitions for capacity, pricing, and distribution advantages?