In the 2000’s national oil companies (NOCs) investing abroad were viewed as new competition to the international oil companies (IOCs). NOCs began acquiring international assets, whether to bolster security of supply for their growing economies, for energy diplomacy or simply to generate new profit streams abroad capitalizing on their domestic capabilities.

Westwood research shows that NOCs have participated in 270 high impact exploration wells outside of their home country since 2008. This is around 23% of the global high impact well total[1]. The 9 most active NOCs have spent a combined US$7bn and discovered a net commercial volume of ~6bnboe.

Though NOCs have retrenched exploration investment alongside the IOCs since the oil price crash of 2014, Qatar Petroleum (QP) has bucked the trend, building an international portfolio from scratch. It has participated in three high impact commercial discoveries already in 2019, two of which were high risk frontier discoveries opening new plays. Given QPs success and also that of CNOOC in Guyana, will other NOCs step up investment in international exploration?

Source: Westwood Analysis

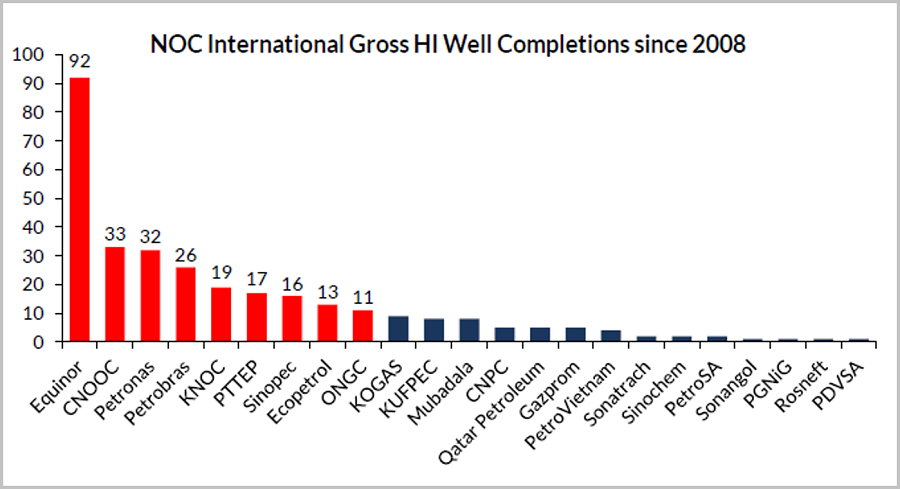

Equinor and CNOOC lead the way

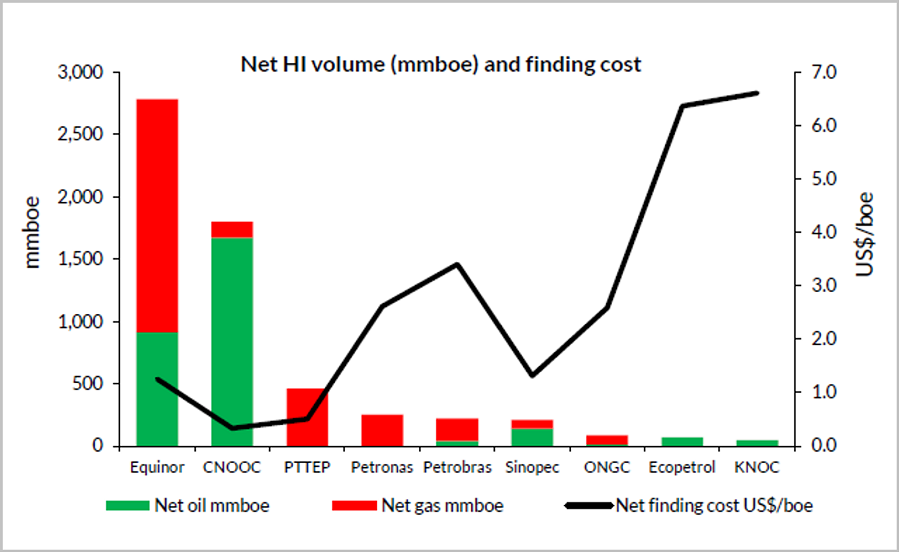

Equinor was by far the most active international NOC explorer, drilling 92 exploration wells in 16 countries outside of Norway with a focus on offshore East Africa, Eastern Canada and in the US GoM. Equinor also discovered the biggest net volume (2.8bnboe), unsurprising given the large number of international wells it has drilled.

In terms of success rates and finding costs, CNOOC led the pack whilst Ecopetrol of Colombia and KNOC of Korea were the least successful. CNOOC’s impressive 54% commercial success rate and $0.3/boe finding costs have been driven by its 25% equity stake in the frontier Stabroek block offshore Guyana which it acquired from Exxon. Stabroek has subsequently delivered over 6 billion barrels of oil equivalent discoveries.

Source: Westwood Analysis

Will QP and CNOOC success trigger another NOC’s to increase their international footprint?

Several of the NOCs have not participated in significant international high impact drilling programs for a number of years and for many of them, international exploration has not added material commercial reserves. Whilst some NOCs (KNOC, Sinopec, Petrobras) are reducing their international footprint, others (CNOOC, Petronas, PTTEP) are becoming more active internationally, and none more so than QP.

QP has just farmed into deepwater Namibia, which follows 2019 entries into Guyana, Kenya and Morocco, having already entered Argentina, Brazil, Mexico, Mozambique and South Africa in 2018. The company’s international exploration program has got off to an impressive start, with three commercial discoveries in South Africa, Cyprus and Guyana from its first four wells in 2019.

QP has used its cash and its relationships to access attractive acreage with competent operators. The company is set to be the most active international high impact NOC explorer through the end of 2021, participating in up to 20 wells at a level comparable to that of the Supermajors. It will be interesting to see whether QP’s early success – combined with CNOOC’s achievements offshore Guyana – will spur other NOCs with deep pockets to become active international explorers.

Vikesh Mistry, Senior Analyst

[email protected]

+44 (0)20 3794 5384

[1] High impact wells are defined as either targeting 100 million barrels of oil equivalent or a frontier play with follow up potential