The US Unconventional industry continues to see increasing completion intensity per well. This is driving spectacular production growth but there are hints that industry is reaching the technical limits of what is possible. The latest Energent analysis casts some light on recent trends and the outlook for 2019.

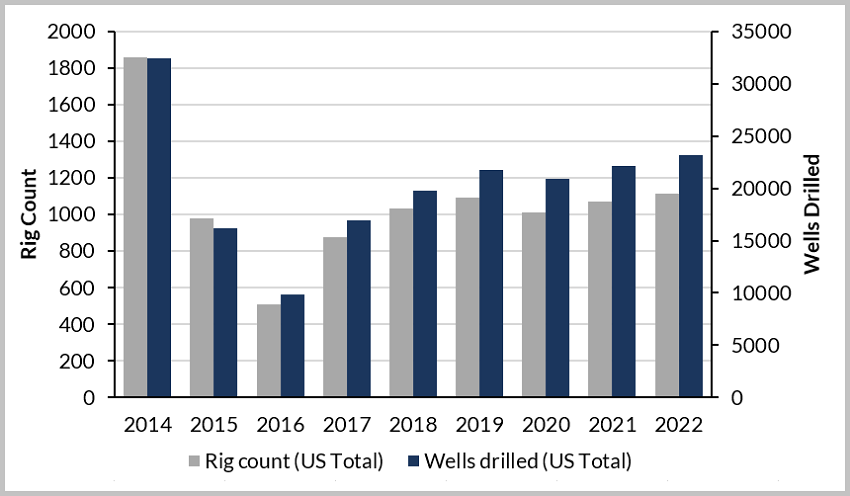

Oil prices appear to have stabilized in early 2019 following a dramatic slide between October and December of 2018 and US operators are showing little sign of reducing drilling programs in the short term. In a $60/bbl WTI oil price scenario, drilling will increase 8% to over 20,000 wells this year, according to Westwood’s new U.S. Drilling and Completion Q4 2018 Outlook. Figure 1 shows Westwood’s annual forecast from 2019 through to 2022 for rig count and wells drilled considering a base case oil price scenario of WTI increasing to $67 in 2020 and up to $70 in 2022.

Figure 1: US Land Rig Projection 2014-2022. Historic rig counts are based on Baker Hughes rig counts.

Then Westwood forecasts future rig counts using ratio of wells drilled per rig and expected future drilling activity.

Source: Westwood Energent data and analysis, GE Baker Hughes Rig Count Data

Potential volatility in oil prices could disrupt drilling and at WTI prices of $52/bbl, WTI growth in 2019 will likely stall. However, aside from the headline macro story, there are currently some key regional and technical factors at play.

While current bottlenecks in the Permian are forcing some operators in the Delaware basin to flare gas to keep the oil flowing, other basins are ramping up activity, especially the Eagle Ford, Williston and MidCon. The drilling activity in the Williston increased by 36% Y-o-Y in 2018, while the Eagle Ford and MidCon increased by 43% and 23%, respectively.

In 2018 the US active land rig count was up 17% overall. Operators will continue to adopt “spudder” rigs to drill the vertical portion of the well and a high-spec rig to drill the horizontal to gain efficiencies and reduce costs. An average pad consists of 4.7 wells in the DJ-Niobrara basin and 3.1 wells in the Williston. Westwood anticipates further adoption of multi-well pad drilling and factory drilling in the Permian and MidCon.

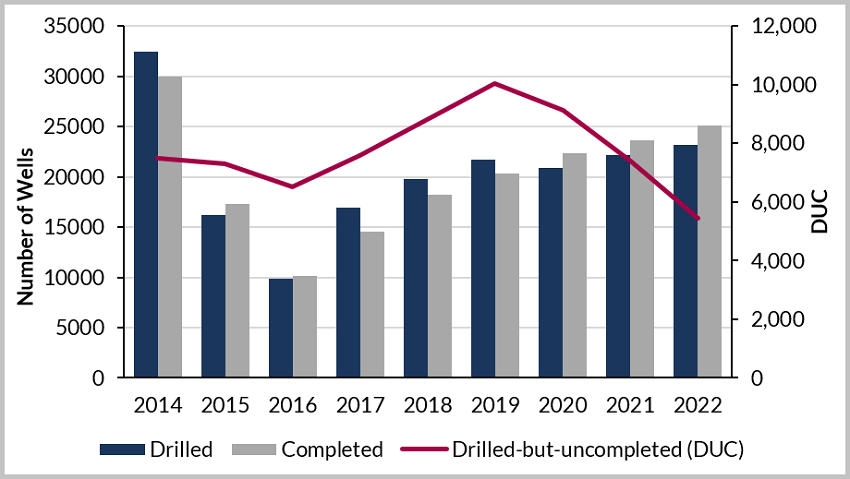

Westwood expects a fall in rig and well count in late 2019 as operators start drawing down the drilled-but-uncompleted wells (DUCs) they have been building since mid-2016. The full effect will take place when the additional take-away capacity comes online in the Permian—bringing new oil and gas off-take capacity of 1.4 mmbpd and 4 bcfpd, respectively. Westwood expects to see total US DUC inventory reaching a peak of 10,300 in Q3 ’19, then gradually decline to 4,600 by 2022 as the completion activity outpaces drilling.

Figure 2: US DUC Projection 2014-2022. DUC count is calculated using cumulative sums based on the level of drilling and completion activities.

Source: Westwood Energent data and analysis

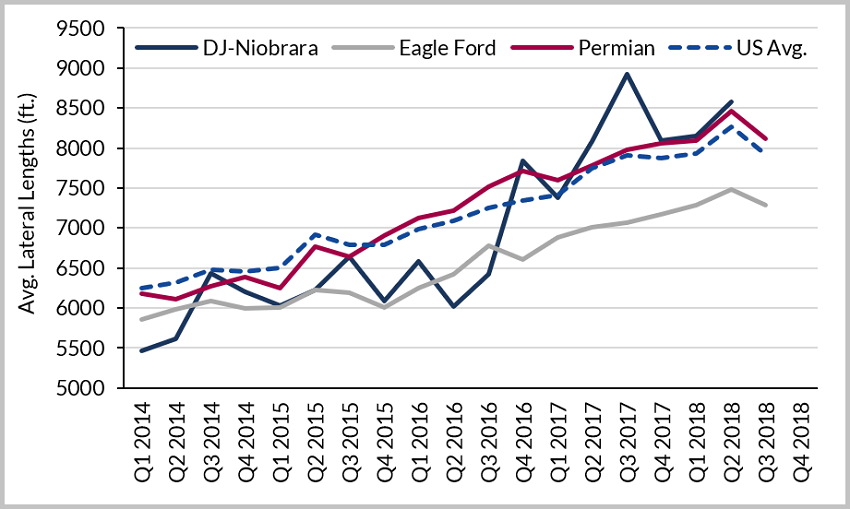

Are lateral lengths and proppant intensity reaching their limits?

Westwood analysis shows that the US average lateral length increased by 4% (300 ft.) Y-o-Y in 2018 compared to 8% (560 ft.) in 2017, suggesting that operators may be reaching technical, acreage, or economic limits. In the DJ-Niobrara, it sharply decreased from 21% (1,400 ft.) increase to 3% (240 ft.) increase in 2018. Similarly in the Eagle Ford, average lateral length only increased by 5% (320 ft.) in 2018, compared to 8% (520 ft.) in 2017. Lastly, the Permian basin also increased 5% (370 ft.) in 2018 compared to 6% (460 ft.) in 2017.

Figure 3: Basin-by-basin average lateral length 2014-2018. Quarterly averages calculated using the entire stock of wells drilled in each quarter.

Source: Westwood Energent data and analysis

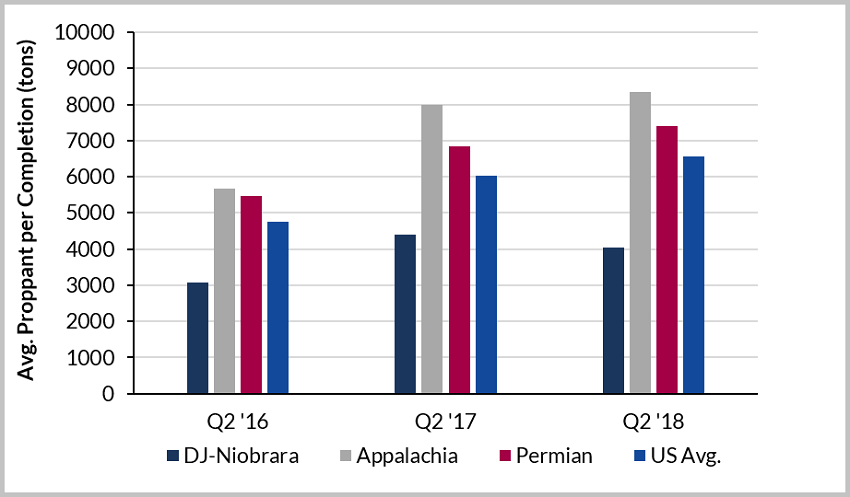

US pressure pumpers are also slowing the rate of increase in frac sand per well. The US average increased by 9% (530 tons) Y-o-Y in 2018 compared to a 27% increase (1,260 tons) in 2017. Looking more closely at the individual basins, the Permian increased by only 8% (550 tons) in 2018 compared to 26% (1,400 tons) in 2017. The change was even more dramatic in Appalachia where it dropped from a 41% average increase (2,300 tons) in 2017 to a 5% increase (360 tons) in 2018. An average well in the DJ-Niobrara basin used 8% less sand (-340 tons) in 2018 compared to 2017.

Figure 4: Basin-by-basin Average Proppant per Completion Y-o-Y Comparison.

Source: Westwood Energent data and analysis

Assuming a $60-70 WTI oil price range over the next few years, completion activities look set to grow through 2022 in the US. Late 2019 will be an inflection point for the US DUC inventory as operators start drawing down their DUC inventories as they begin to adopt less aggressive drilling program guidance. Finally, slower increases in average lateral length and completion intensity for horizontal wells implies that the frac sand demand may not increase as quickly as some expect.

James Jang

Analyst, Westwood Global Energy

[email protected]

+1 713-714-4885