A new study by Westwood Global Energy Group shows that 11 billion barrels of oil and 36 billion barrels of oil equivalent (boe) gas in 119 discoveries >100 million boe in size made between 2008 and 2016 is currently stalled with no progression towards development. This oil and gas, potentially, worth more than $65[1] bn and costing an estimated $24bn to discover, represents 40% of the volume found in high impact discoveries in the period. Where is this resource located? Why is it stranded and how big an opportunity does it represent?

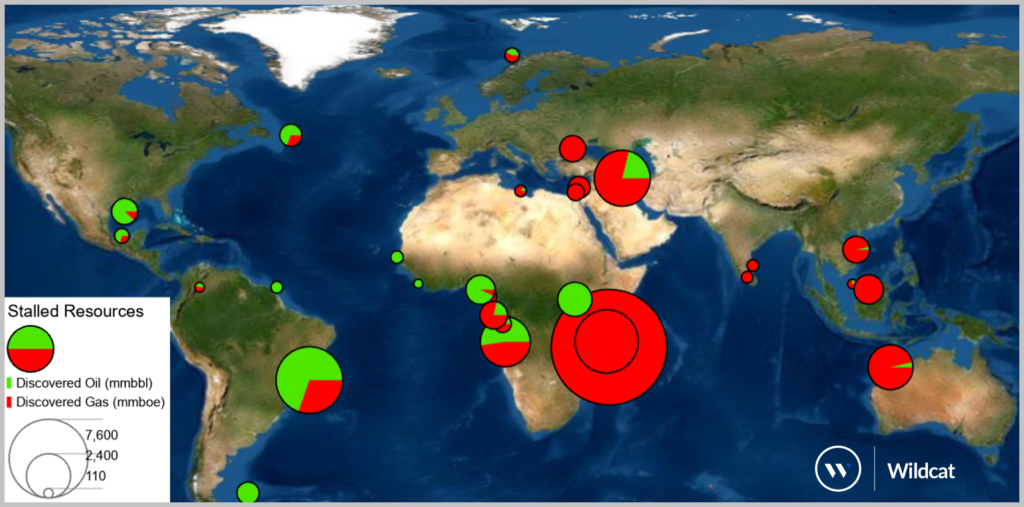

Location map of stalled resources in HI discoveries by country.

The largest volume of stalled gas is in the Ruvuma-Rufiji basin of Mozambique and Tanzania where 166Tcf was discovered between 2010 and 2015 yet only 38Tcf has shown any sign of progression and 128Tcf of gas remains stalled. Brazil has the largest stalled oil (and condensate) resource, estimated at 3.8 bnbbl in 19 HI discoveries in 5 geological basins. 16.5Tcf of gas remains stalled in Iraqi Kurdistan, 3bnboe of oil and gas (split 50:50) is stalled across the Kwanza and Lower Congo basins of Angola and 14Tcf of gas remains in the ground in the Browse and Carnarvon basins of Australia. More than 500mmboe are stalled in each of Nigeria, Malaysia, Gabon, Vietnam, USA, Romania, Uganda, Cyprus, Canada and the Falkland Islands.

Westwood has identified 26 different contributing factors for >100mmboe discoveries stalling. Above ground factors dominate, with the fiscal regime / gas terms in the host country, access to finance and portfolio prioritization being the most common. Subsurface factors include fluid composition, and reservoir quality and compartmentalisation.

In Tanzania for example, 14 deep-water gas discoveries clustered in five potential developments are stalled due to a combination of above ground and subsurface issues. The above ground issues are mainly related to protracted negotiations with the Tanzanian government on gas terms. Reservoirs are more compartmentalised than in neighbouring Mozambique with lower resource densities and higher development costs.

In the Santos basin of Brazil six discoveries are stalled mainly due to subsurface issues. The Jupiter discovery has large volumes of associated CO2 and development is possibly waiting on new CO2 handling technologies that be are being tested at Mero. Dolomita Sul, Bigua and Bem-Te-Vi pre-salt discoveries are smaller than the average in the play due to small trap size and low reservoir quality and so were low in the priority list for Petrobras who relinquished the discoveries

In Angola’s Kwanza basin seven pre-salt discoveries are stalled due to a combination of above ground and subsurface issues. The discovered hydrocarbons are gas rich, ~50% gas and only since 2018 have operators had the rights to the gas under production sharing agreements. The financial struggles of the operator Cobalt International and its subsequent replacement by Total didn’t help resource progression either.

Three key mechanisms have been identified that could break the log jam of stalled discoveries.

- Improved gas terms and gas market access: 36 bnboe of the total 47 bnboe of stalled resource is gas in gas, gas condensate or oil and gas discoveries. In many cases gas was not the pre-drill exploration target and despite significant volumes being found, either market access, export infrastructure, or the terms are not in place to progress the discoveries. Explorers need to think through the gas commercialisation options even when exploring for oil. Even when gas is the target, gas terms, a lack of ullage in existing facilities and domestic politics can still be barriers to development.

- Appraisal to unlock upside: 46 stalled discoveries have not yet been appraised and stalled discoveries not yet declared commercial have significantly fewer E & A penetrations on average, compared to fields which have received FID. There may be some hidden gems where additional subsurface data from appraisal drilling could unlock upside potential in some cases.

- Application of new technologies: 10 discoveries with 2.5 bnboe of resources are stalled due to subsurface challenges, which could be overcome with the application of new technologies including ultra-high pressure and temperature well completions in the Paleogene plays of the Northern Gulf of Mexico and CO2 handling in the Santos basin pre-salt play.

It is both surprising and concerning that 40% of the resource found in discoveries >100 million boe size made between 2008 and 2016 remains stalled, with no appraisal activity or indications of progression to FID since 2016. These stalled assets are an opportunity for companies with the means to unlock them. Equally, they are a reminder to explorers to focus on value, not only volume. Better gas terms and market access could unlock a huge stranded resource. In other cases, new operators with new thinking could make the difference.

[1] Assuming $1.2/boe for gas and $2/bbl for oil

Graeme Bagley, Head of Global Exploration & Appraisal

[email protected]

For more information on the new report, “Progressing resources to reserves – why are so many projects stalled?” contact [email protected].