When Shell announced final investment decision (FID) on its Prelude floating liquefaction natural gas (FLNG) unit in May 2011, it was meant to be the start of an era. An era that would herald the development of stranded gas fields at lower costs. However, 12 years on, the supposed flood of new units has instead been a trickle and only five FLNG units with 12.1 mmpta of FLNG capacity have commenced commercial operations.

Whilst Shell’s enthusiasm pre-FID of the Prelude unit in 2009 meant that it signed a 15-year master agreement with Samsung Heavy Industries (SHI) and Technip for the design, construction and installation of FLNG units under a generic “design one, build many” solution, the supermajor declined to conceptualise any additional unit. The challenges surrounding Prelude have been well-documented, including construction delays, cost overruns and ongoing operational challenges, while weakened market conditions halted additional investment from the supermajor. Several other FLNG projects previously under consideration have also failed to progress to FID, including the Kumul FLNG and Western LNG Projects off the coast of Papua New Guinea, Steelhead LNG’s Kwispaa LNG Project (Canada) and Main Pass Energy Hub off the coast of Louisiana in the US Gulf of Mexico. Whilst all these projects had various reasons for not progressing, an overarching theme was development cost and project financing.

Despite this, there have been success stories with units sanctioned after Prelude. This includes the successful redeployment of Petronas’ PFLNG Satu from the Kumang Cluster development offshore Malaysia, where it commenced operations in 4Q 2016 to the Kebababgan field in 2019 without drydock. Other producing units include Golar LNG’s FLNG Hilli Episeyo (Cameroon), Petronas’ PFLNG Dua (Malaysia) and Eni’s Coral Sul FLNG unit (Mozambique).

Although FLNGs offer cost efficiencies compared to onshore alternatives, project operators have typically opted to wait for the right conditions to progress these multi-billion-dollar projects. With gas prices hitting record highs in 2022 and a desperate need for Western nations to pivot away from Russian gas, the time is nigh for the stuttering FLNG industry to fully bloom.

Africa to dominate near-term FLNG investments but opportunities abound in the Americas

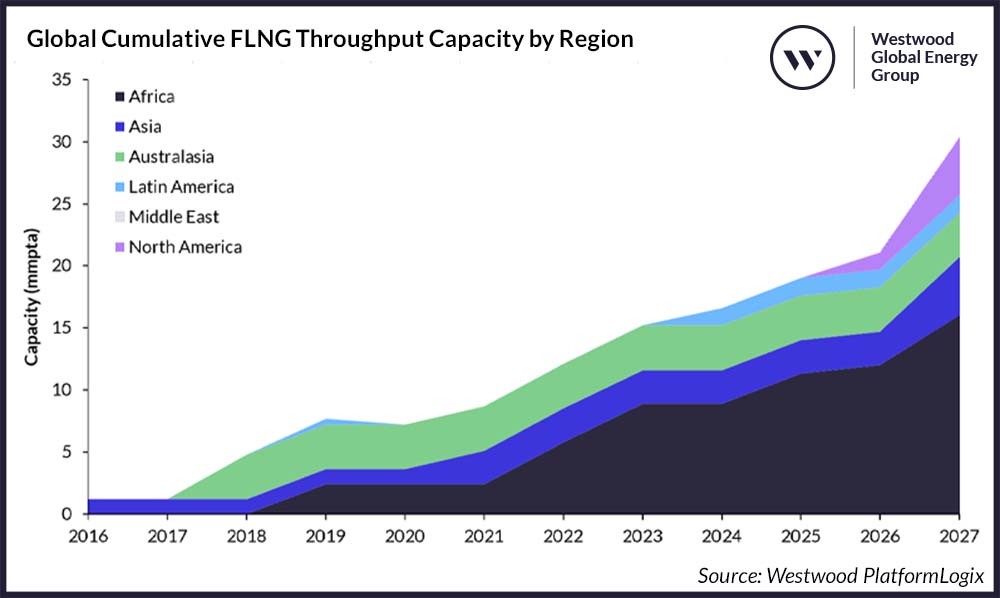

With increasing energy demand and the challenges of energy security, the need for gas to meet the immediate and medium-term energy demand is driving investments in the FLNG market, given the role gas will play in transitioning to a low-carbon energy future. In view of FLNG investments in 2022 and planned investments expected over the 2023-2027 period, Westwood anticipates 18.3 mmpta of additional FLNG capacity onstream by 2027, with an associated engineering, procurement and construction (EPC) award value of US$13 billion. A further 36.5 mmpta is anticipated onstream post-2027 from FLNG units sanctioned over 2023-27, with an EPC value of US$22 billion.

Global Cumulative FLNG Throughput Capacity by Region

Source: Westwood PlatformLogix

Africa will account for 56% (10.2 mmpta) of additional FLNG capacity onstream over the 2023-27 period. Four FLNG units destined for the region are currently under construction / reactivation. The Golar LNG-owned Golar Gimi FLNG unit destined for BP’s Tortue project offshore Mauritania is scheduled to be the first unit delivered in the region over the forecast period and will commence production in 4Q 2023. However, the first LNG cargo exported is not expected until 1Q 2024. The Eni-owned Tango FLNG unit purchased from Exmar Group in 2022 is scheduled to start-up in December 2023 at the Marine XII block offshore the Republic of Congo, whilst a second FLNG unit currently being constructed by Wison Heavy Industry is expected to be installed in the same block by 2025.

In Gabon, Perenco recently sanctioned a 0.7 mmpta FLNG unit to be deployed at the Cap Lopez Oil Terminal LNG off the coast of Gabon, whilst UTM Offshore’s FLNG unit to be installed in OML 104 offshore Nigeria is scheduled to be sanctioned in 2024, with JGC currently carrying out front-end engineering and design (FEED) studies. However, UTM is yet to finalise a gas sales agreement with the block owners, ExxonMobil and Nigerian National Petroleum Corporation (NNPC). Other proposed units anticipated to be sanctioned in Africa over the forecast period include a second unit at Eni’s Area 4 development offshore Mozambique and BP’s Yakaar-Teranga and BirAllah gas discoveries offshore Senegal and Mauritania respectively. It is pertinent to state that Golar LNG recently secured an option to acquire a 148,000 m³ moss-design LNG carrier for a 3.5 mmtpa MKII FLNG conversion. If the unit acquisition completes in 2Q 2023 as planned, Westwood anticipates that the converted unit could be deployed offshore Africa, with Golar stating that yard availability is confirmed for 2025 delivery and advanced EPC negotiations are underway.

Global FLNG Throughput Capacity Status by Region

Source: Westwood PlatformLogix

In the US, Delfin Midstream plans to install four floating vessels producing up to 13.3 mmpta. However, despite the completion of FEED studies by Samsung Heavy Industries and Black & Veatch in 2020, Defin is yet to reach FID and has been granted four one-year extensions to begin construction of the onshore metering, compression and pipeline facilities. In September 2022, Delfin announced a total of 2.5 mmpta long-term supply agreement, which it claims is required to begin construction for the first FLNG unit currently planned to commence this year. Aside from NFE’s plans to host liquefaction plants on converted jack-up rigs and fixed platforms, the US-based LNG player has entered into master service agreements with Sembcorp Marine for the engineering and conversion of two Sevan cylindrical drilling units (Sevan Driller and Sevan Brazil) to FLNG units, including the fabrication and integration of LNG topside modules.

In Canada, 17.5 mmpta of LNG capacity is in the planning phase across three projects. However, Westwood does not anticipate any Canadian projects to commence commercial production before 2028. In other regions, the use of an FLNG unit is being considered for Chevron’s Leviathan gas field offshore Israel and Transborder Energy’s LNG project off the coast of Australia. However, there have been significant delays in deploying these units, with Chevron still evaluating alternative concepts for increasing its gas capacity from the Leviathan project.

Overall, LNG supply growth is expected to rise significantly, especially from the US and Qatar. The current risk is that this will lead to an oversupply in the market and push out riskier and higher cost projects. This means that FLNG developments must focus on its differentiator to compete – including its speed to market and flexibility. Furthermore, the use of FLNG units to develop massive gas reserves offshore Mauritania, Senegal, Tanzania and Mozambique is also perceived to be more favourable compared to onshore alternatives, as it represents a lesser security risk to IOCs.

The outlook for LNG generally looks bright in the coming decade, as it has a vital role to play in Europe, principally to offset the fall in Russian piped gas following the invasion of Ukraine. At the same time, the increase in coal-to-gas switching and further industrialisation in Asia (primarily India and China) creates a key growth opportunity for LNG. The significant drive to develop renewables and other New Energies (such as Hydrogen) in Europe and more mature Asian markets (including the traditional LNG demand markets of Japan, Korea and Taiwan, as well as China), could represent a downside risk for the sanctioning of additional FLNG capacity post-2030.

Mark Adeosun, Director – SubseaLogix & PlatformLogix

[email protected]