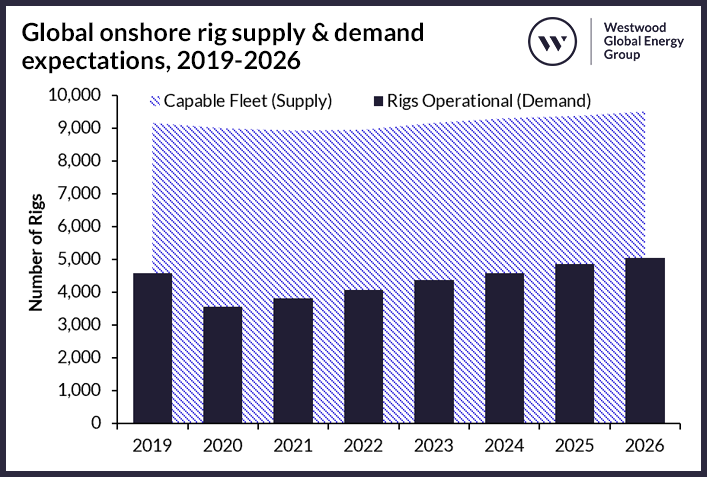

The outlook for onshore rig demand is improving with elevated commodity prices spurring increased drilling activity in many regions (from the lows of 2020 and 2021). Westwood expects to see a stronger increase in activity than previously forecast, however, operators remain wary of threats such as rapid changes in commodity pricing and the pricing of drilling materials such as drill pipe and frac sands.

Global onshore rig supply & demand expectations, 2019-2026

Source: Global Land Rigs, Westwood analysis

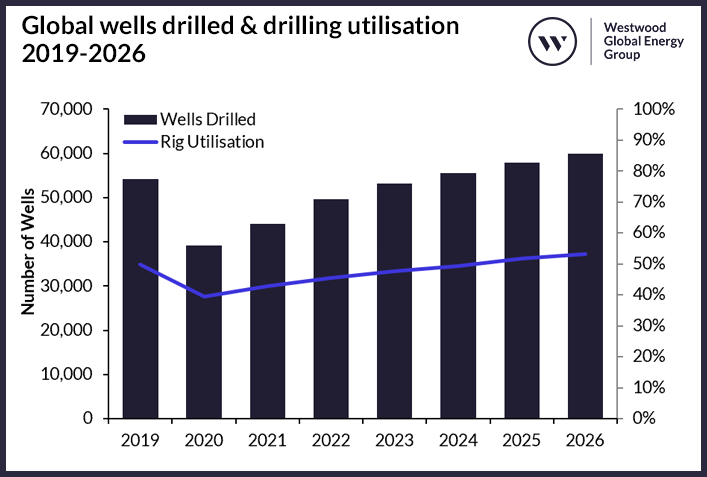

Westwood projects the number of wells drilled over the forecast period (2022-2026) to strongly increase year-on-year, reaching upwards of 60,000 in 2026, compared to c. 49,600 in 2022. Global drilling levels are expected to top 2019 drilling levels in 2024, which was not previously considered in Westwood’s outlook last year. The increase in wells drilled is forecast to lead to a year-on-year growth in the number of rigs operational. Westwood estimates that 4,070 rigs on average will be operational in 2022, growing to c. 5,050 by the end of the forecast, representing an increase of 24%.

Global onshore wells drilled & drilling utilisation, 2019-2026

Source: Global Land Rigs, Westwood analysis

Westwood’s global forecast is driven predominantly by a small number of countries with China, the GCC (Gulf Cooperation Council) countries, Russia and the US accounting for approximately 80% of forecast rig demand. China is likely to account for the greatest share of wells drilled and should see continued robust levels of drilling activity, while a strong growth in demand is also expected from the GCC countries. Russia, the third largest driller globally, is anticipated to see a decrease in the first year of the forecast before a slow recovery, however, Russian activity will depend greatly on the outcome of the war in Ukraine. At the other end of the spectrum, activity in the US is expected to make a strong return, as the US prioritises energy security and operators look to benefit from the high O&G prices.

Chinese NOCs that operate the country’s largest oilfields are aiming to increase both oil and gas production. This has led to increased activity in China’s significant shale oil deposits with Sinopec making a major shale oil discovery in July 2022 at the Subei basin, and PetroChina sanctioning an overall development plan for shale gas extraction at the Yang 101 block in the Sichuan basin, which could produce up to 5 bcm per annum by 2025 and 20 bcm per annum by 2035. This push in activity could see China drill up to 14,200 wells over 2022, increasing year-on-year to c. 16,100 in 2026 and ramping up rig utilisation to 90%.

Over the past year GCC countries have been a hotspot for contract awards as several member countries target an increase in production capacities. The leaders of this move are Saudi Arabia and the United Arab Emirates (UAE), who plan to increase their production capacities to 13 mmbbl/d and 5 mmbbl/d respectively. Saudi Aramco has begun investing in the Jafurah unconventional play. ADNOC, meanwhile, plans to spend $127 billion to increase its production capacity to 5 mmbbl/d by 2030, involving the drilling of thousands of wells utilising ADNOC Drilling’s rapidly expanding onshore rig fleet.

Rig contractors react to conflict in Ukraine

Russia’s invasion of Ukraine has had a significant effect on the global hydrocarbon industry, sending oil prices spiralling up to $127 per barrel in March 2022 after starting the year at $78 per barrel. Several operators and contractors have left Russian assets or abandoned rigs within the country. IOCs, BP, Shell and ExxonMobil announced plans to exit Russia following the invasion. BP cut ties with its 19.75% shareholding in Rosneft whilst Equinor will no longer invest in Russia and will exit its Russian joint ventures including the North Komsomolskoye oil field development project in West Siberia and 12 exploration and production licenses in Eastern Siberia. Shell ended its involvement in the Nord Stream 2 pipeline and exited its 50% stakes in the Gydan and Salym petroleum development projects.

International rig contractors also acted and altered their operations within the country. KCA Deutag suspended new investments and is evaluating options regarding its 21 rigs located in the country. The West has openly denounced Russia’s actions, sanctioning Russian O&G, cutting imports, and opening opportunities to other O&G exporting countries. The European Union (EU) has been a big importer of Russian O&G, importing 40% of its natural gas from Russia in 2021. In the face of reduced exports to the West, Russia has turned to China and India to sell its oil and gas. India’s oil imports from Russia surged to a record of around 950,000 bpd in June, a 15.5% increase on May.

Russia’s wells drilled are forecast to drop significantly from 2021 to 2022, decreasing 28% to c. 4,600 wells in 2022. This decline is expected to continue into 2023 before a slow recovery for the remainder of the forecast period, supported by the aforementioned demand from China and India. Whether this demand will be enough to fully make up for the decline in demand from Western Europe is yet to be seen. With the war in Ukraine ongoing it is difficult to gauge the future impact on drilling but, unless there is a significant change soon to end sanctions, it seems unlikely drilling activity will manage to stay at the levels from recent years. This could however lead to increased drilling activity in other locations as Europe looks for alternative sources.

In the US, Westwood forecasts activity to continue to rebound as operators take advantage of elevated oil prices to increase their free cash flow. Sanctions on Russian energy within the EU and other countries has increased demand for US LNG exports to Europe and elsewhere. Despite damage to the Freeport LNG facility in June 2022, the US was the world’s largest LNG exporter through 1H 2022. By year end 2022, the US will have added 2.4 bcf/d of export capacity.

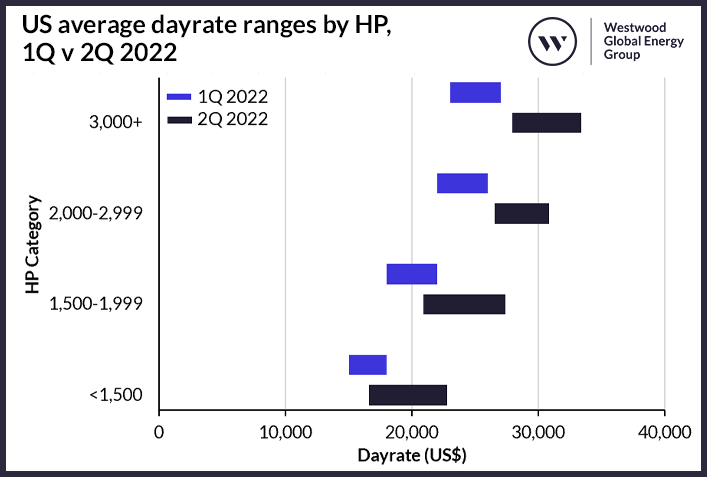

North America has been more reactive to the oil price increase, with contractors recently announcing a 25% and 35% increase in land drilling rig dayrates in the US and Canada respectively. Tier 1 rigs in the US are now demanding dayrates up to the mid-$30,000s. Contractors are also pushing more Capex budget towards reactivating Tier 1 rigs or upgrading M-rigs to Tier 1 to meet demand. Newbuild super-spec rigs would cost in the region of $30 million, whereas reactivation costs are about $4 million per rig.

US average dayrate ranges by HP, 1Q v 2Q 2022

Source: Global Land Rigs, Westwood analysis

Many contractors are reporting average daily rig revenues of c. $26,500 per day during 2Q 2022, which is up from the values of $23,000-$24,000 obtained in 1Q 2022. With the high spot prices for rigs and drilling equipment, contractors are still looking to keep contracts short to maximise revenues.

Overall, higher commodity pricing is driving significant recovery for land rig demand in 2022, which is expected to continue through to 2026. Activity in the US is forecast to return to pre-pandemic levels and rig demand is expected to be bolstered by shale play developments, with China, the GCC and Argentina at the centre of the action. Several regions are also benefiting from higher land rig dayrates, aided by increasing demand for higher specification automated equipment.

Todd Jensen, Analyst – Onshore Energy Services

[email protected]

For more information on how to access the eleventh edition of Westwood’s World Land Drilling Rig Market Forecast 2022-2026, click here.