This insight examines the results of key land rig contractors, the widening divergence between North American and Middle Eastern revenue, and how an increasingly uncertain geopolitical backdrop could shape the year ahead.

North American domiciled contractors dominate

All major public land rig contractors have now reported their 2025 financial results, with 4Q 2025 revenue averaging $3.54bn, up 1% quarter‑on‑quarter and in line with the 2025 average. Full‑year revenue totalled $14bn, down 3% year‑on‑year and marking the first annual decline since 2020, reflecting a year in which oil prices averaged $69, down from $81 in 2024. The weaker price environment constrained international revenue growth, leading to a decline in North American revenue.

Figure 1: Select Land Rig Contractor Revenue 2019-2025

Source: Westwood Global Land Rigs, Corporate Financials

Of the six land rig contractors which recorded over $1bn revenue in 2025, five are American-domiciled companies. Helmerich & Payne (H&P) leads the group, having topped quarterly revenue tables since 4Q 2022. Its acquisition of KCA Deutag, completed in January 2025, pushed its 2025 revenue to $3.3bn, 25% higher than 2024, and expanded its international fleet from 27 rigs in September 2024 to 131 a year later. The deal was driven largely by H&P’s ambition to deepen its presence in the Middle East, where it now operates 77 rigs, or 59% of its international portfolio.

Nabors, in second place, undertook a smaller expansion with its March 2025 purchase of Parker Wellbore. The acquisition lifted its average quarterly revenue to $653mn across 2Q–4Q 2025, up from $617mn between 1Q 2024 and 1Q 2025. Both H&P and Nabors have used these deals to broaden their international exposure during a period of weakened oil prices and operator efficiency drives, both of which weigh heavily on the core North American market.

ADNOC Drilling is the only non‑North American firm among the top six. It has held third place since 2Q 2024, with an average quarterly revenue of $498mn. Strong utilisation across the UAE has underpinned this performance, supported by the company’s role in Turnwell Industries, a joint venture set up to advance unconventional development. Revenue has climbed from $1bn in 2019 to $2bn in 2025 – a 102% increase and well ahead of any North American-based rival. ADNOC Drilling also made a series of high-profile moves in 2025, including buying a 70% stake in SLB’s Oman and Kuwait rig fleets in May 2025, as well as a similar deal with MB Petroleum Services in Oman in late 2025. This, along with a contract to begin drilling operations in Jordan, highlights the company’s goal of expanding further and becoming a regional powerhouse.

Figure 2: Select Land Rig Contractor Revenue Comparison

Source: Westwood Global Land Rigs, Corporate Financials

Diverging US & Middle Eastern contracting markets

With 2025 oil prices 14% below 2024 levels, the difference between the regions was laid bare: North America remains beholden to short‑term price swings, while the Middle East, especially the core Gulf Cooperation Council (GCC) countries of Kuwait, Oman, Saudi Arabia and the UAE, are anchored by long‑term contracts.

Figure 3: North America & Middle East Rig Revenue 2019-2025

Source: Westwood Global Land Rigs, Corporate Financials

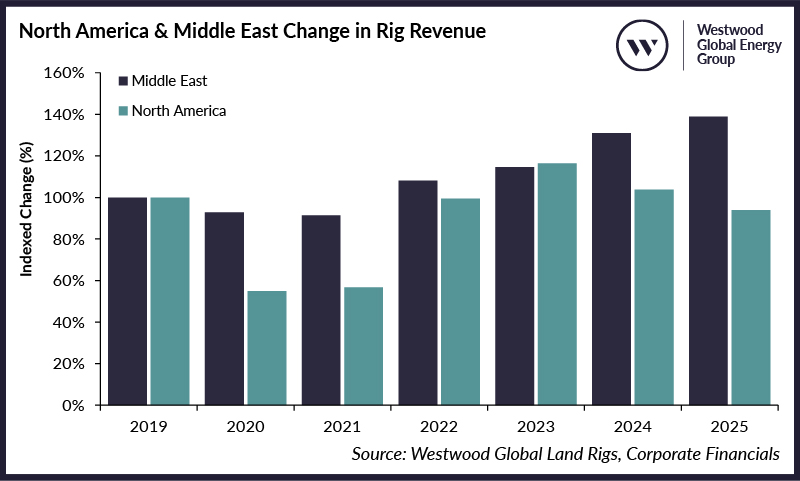

As Figure 3 shows, North American revenue remains closely tied to oil prices, with changes in commodity prices generally feeding through to contractor earnings after a lag of approximately six months. The most recent US revenue peak in 1Q 2023 followed the oil‑price high of $114 in 2Q 2022. As prices have fallen, the pattern has persisted: by 4Q 2025, North American revenue slipped to $1.2bn, 26% below its peak, broadly mirroring the 33% drop in oil prices over the same period. The Middle East, by contrast, has moved in the opposite direction, with revenue rising 31% between 1Q 2023 and 4Q 2025. Taken together, the data illustrates the sharply diverging fortunes of the two regions since 2019.

Figure 4: North America & Middle East Indexed Change in Rig Revenue

Source: Westwood Global Land Rigs, Corporate Financials

Beyond commodity prices, the US, which accounts for 78% of North America’s rig fleet, has been squeezed by operator consolidation, tighter budgets and efficiency gains, resulting in idled, relocated or scrapped rigs. Canada has offered only partial relief: the TMX pipeline’s commissioning in 2024 and rising LNG demand have boosted activity, but not enough to offset the decline in the US Lower‑48, where rig counts have averaged about 550 since 2020, far below the 1,200 average of 2000–2019.

High‑quality, modern rigs have provided some protection for contractors. Operators increasingly demand rigs capable of drilling deeper laterals, equipped with advanced monitoring systems and strong performance records. Firms with high‑spec fleets and digital capabilities, including AI‑based drilling tools, have been best placed to benefit, supported by performance‑linked contracts and higher average dayrates.

Middle East revenue, meanwhile, benefits from some of the world’s highest dayrates coupled with a preference for long‑term contracts (typically five to ten years across the GCC), helping to shield contractors from commodity price swings and enabling regional revenues to rise even as Brent prices fell. This has been boosted by a growing focus on gas drilling, something that has helped support activity even as OPEC+ related output restrictions impacted drilling in conventional oil plays.

An uncertain picture for the year ahead

2026 was expected to extend the Middle East’s lead over North America, with limited upside for oil prices and North American operators setting conservative capex budgets. Furthermore, the region’s strong run of rig contracting was also set to continue, helped by a ramp‑up in Saudi Arabia, as Aramco issued restart notices in 4Q 2025 and in the first two months of 2026, beginning a reversal of suspensions that began in April 2024 following the decision to pause plans to increase oil capacity. At its peak, these suspensions sidelined around 85 onshore rigs, with the number of suspended rigs expected to steadily decline over the course of 2026.

Instead, the outlook has shifted sharply. The US–Israeli war with Iran has driven a major oil price spike and, although exact figures are unknown, has triggered numerous rig suspensions across Iraq, Kuwait, Saudi Arabia and the UAE – a sudden shock to the Middle Eastern land rig market, which is unlikely to ease until a peace treaty or long-term cease fire is achieved.

Continued higher prices could, however, prompt US Lower‑48 operators to reconsider their conservative 2026 budgets, as they did in 2022, raising the prospect of idle rigs being reactivated and North American revenues improving. The situation remains highly fluid: a peace deal with Iran could see rigs across the core Middle Eastern markets return to work quickly, though this will remain dependent on the damage to both midstream and downstream assets.

In the US, a sustained period of elevated oil prices could begin lifting revenues as early as the second half of 2026, reflecting the market’s rapid responsiveness. Should demand materially increase within the Lower‑48, the issue for US rig contractors is likely to shift from the presence of long‑idled rigs to how swiftly those units can be brought back into service.

Ben Wilby, Manager – Onshore

[email protected]

Michela Francisco, Onshore Land Rig Analyst

[email protected]