HM Treasury’s Oil and Gas Price Mechanism (OGPM) aims to replace the Energy Profits Levy (EPL) with a permanent regime to target windfall revenues. While the move promises fiscal clarity, there are concerns regarding the proposed threshold gas price. The unrealistic threshold means that the EPL will likely remain in place until March 2030. Getting the new baselines right is essential to unlocking investment and future value from the UK sector.

Alongside the Autumn Budget, HM Treasury published its OGPM Consultation – Summary of Responses document, outlining the Government’s plans for a permanent fiscal regime to target windfall revenues generated with high oil and gas prices. The permanent OGPM will replace the EPL when it ends, be that on 31 March 2030, or earlier should the Energy Security Investment Mechanism (ESIM) be triggered.

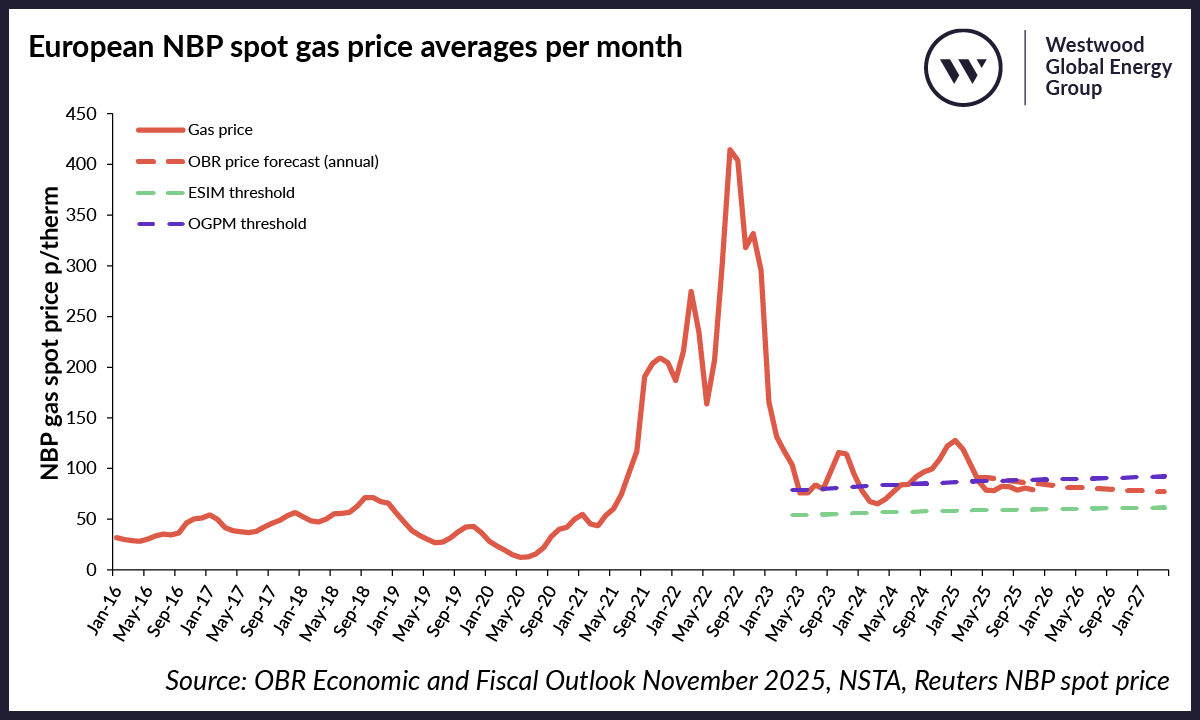

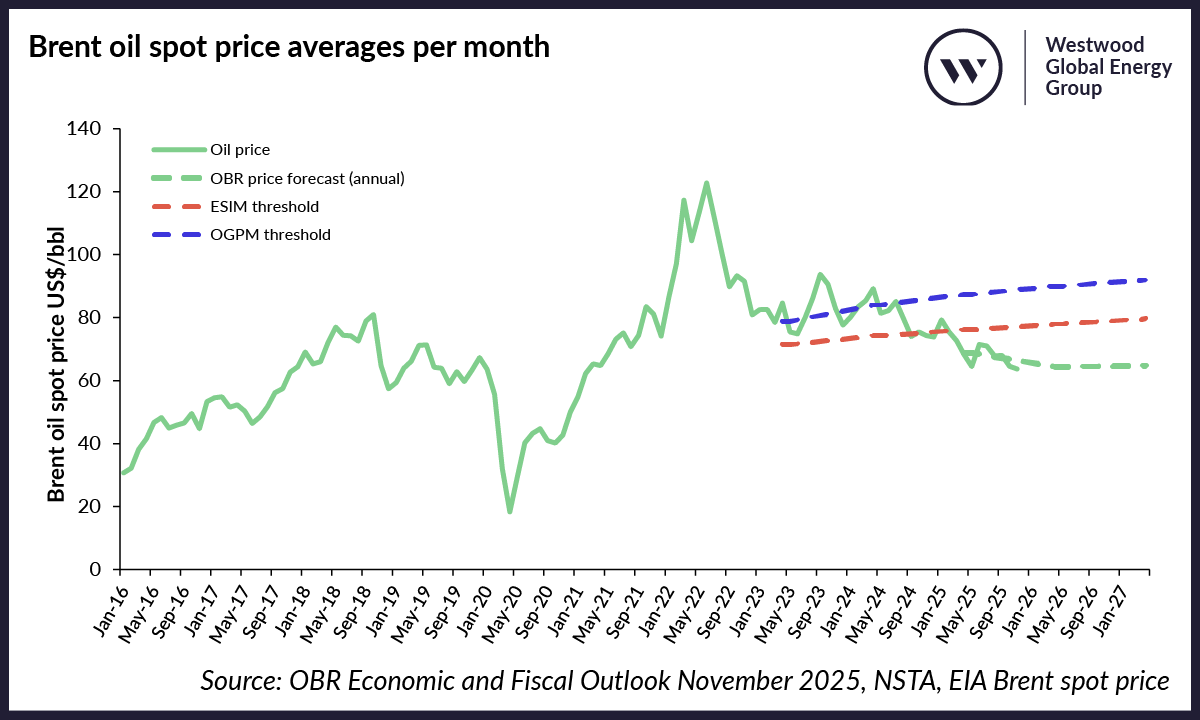

Under current EPL regulations, the ESIM will trigger the end to the EPL if six-month average prices for both oil and gas fall below the respective ESIM thresholds. For 2025/26, these thresholds are US$74.21/bbl for oil and 57p/therm for gas. For reference, the OBR forecasts an annual average oil price of US$68.79/bbl for the same period, below the threshold. Its gas price, however, is 91p/therm, well above the ESIM threshold meaning the EPL remains in place. This is not because gas prices are currently high, it is because the threshold was set too low to be reflective of the globalisation of the gas market due to the rise of LNG. As a result, the UK oil and gas sector is still paying a windfall tax on windfall prices that do not exist.

The OGPM is positive as it will only be in place during periods where the oil and gas prices are above the recommended thresholds, in effect only taxing the ‘windfall’ revenues. The OGPM will also therefore provide fiscal clarity and more stability going forwards, which will enable companies to better plan business decisions. The Government has opted for a Revenue-Based Mechanism (RBM), which taxes excess revenue from oil and gas sales, rather than a Profit-Based Mechanism (PBM) which was preferred by many respondents and would have taxed profits.

Figure 1: European NBP spot gas price averages including the ESIM and OGPM thresholds and the OBR price forecast, adjusted for inflation using CPI. Source: OBR Economic and Fiscal Outlook November 2025, NSTA, Reuters NBP spot price

Figure 2: Brent oil spot price averages per month including the ESIM and OGPM thresholds and the OBR price forecast, adjusted for inflation using CPI. Source: OBR Economic and Fiscal Outlook November 2025, NSTA, EIA Brent spot price

However, concerns remain over proposed thresholds. For the 2026/2027 period, the thresholds will be US$90/bbl for oil and 90p/therm for gas. The oil threshold is broadly in line companies’ high price scenarios and is 40% higher than the OBR’s forecast price for 2026/2027. For gas however, the threshold is lower than the OBR’s price forecast for 2025/2026 and only 11% above the OBR’s price forecast for 2026/2027. This price forecast relies on assumptions of a gas supply glut to enable reduction in prices. As it stands, the gas price could enter ‘windfall conditions’ cyclically when gas prices rise with harsh winter conditions.

There is also significant disparity in the ESIM and OGPM thresholds. The OBR forecasts that gas will remain above the EPL ESIM threshold but below the OGPM threshold, on an annual basis, until the scheduled end of the EPL in March 2030. Using the government’s new definition of ‘windfall conditions’ defined by the OGPM thresholds, the oil and gas sector fell out of ‘windfall conditions’ in April 2024, on a six-month average price basis. Since then, gas prices have been below ‘windfall conditions’ for 10 out of 20 months. Oil has been outside of ‘windfall conditions’ for 19 months. Despite this, the EPL is still being applied to company profits.

Why does it matter?

The OGPM is to be a permanent fiscal mechanism to address excess profits caused by erroneously high oil and gas prices, as happened following Russia’s invasion of the Ukraine. It should be built upon a robust mechanism with a realistic baseline threshold which is representative of genuine high price scenarios. The assumptions for setting the price thresholds should be evidence-based, for clarity and understanding. Getting these thresholds right must be the foundation for building a future permanent tax regime, to help unlock investment to maximise recovery and social economic value from the UK basin.

Yvonne Telford, Research Director – Northwest Europe

[email protected]

Matthew Belshaw, Senior Analyst – Northwest Europe

[email protected]