Macro uncertainty means short term oil price volatility in the $50-80 per barrel range

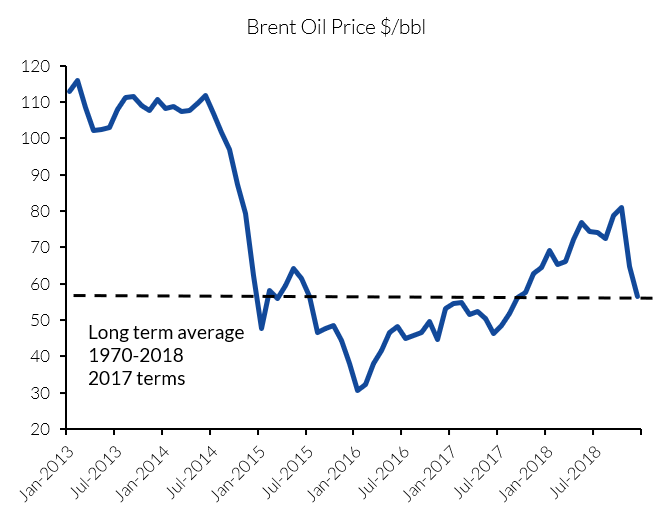

The oil price recovery that began in early 2016, and which gathered momentum in the second and third quarters in 2018, faltered in the fourth quarter with prices regressing back towards the long-term average of $56/bbl. Oil and gas demand has never been higher with the IEA reporting demand growing 1.3 million barrels a day to over 100 million barrels a day for the first time in 2018.

Figure 1: Brent Oil Price $/bbl

Source: Westwood Analysis

Supply more than kept pace with demand in 2018. The US led the charge with production growing a remarkable 1.9 million barrels a day to 11.7 million barrels a day during the year. Political uncertainty abounds at present in all regions and this together with the biggest physical oil market ever, points to continued short term volatility in the $50-80 per barrel Brent range. If demand keeps rising a supply crunch will eventually drive prices higher than this band given the low levels of capital investment since 2015, but probably not in 2019. If demand growth falters, then the current over supplied market could last longer.

E&P companies remain cautious with capital investment up an average 8-10%

Larger E&Ps were in rude financial health in 2018, particularly in Q3 when they were enjoying $75 per barrel average revenues with breakeven costs at $40-50 per barrel. Free cash easily covered dividends and capex and share buy backs were again in vogue. Nonetheless, caution in boardrooms remains with the focus more on sustaining profitability and dividends rather than accelerating growth. Expect modest Capex increase in 2019 of 8-10%.

The energy transition to a low carbon future continues to vex the larger companies but actions so far lag the words – will a Supermajor break ranks in 2019 and really chart a different course?

For now, US tight oil remains popular for its flexibility and optionality when deploying capital – it can be switched on and off depending on the oil price and returns are quick. Sceptics remain regarding its long term potential and expectations are high for shale to lead future supply growth. Could 2019 be the year when cracks appear in the technical underpinnings of the growth story as the sweet spots are drilled out?

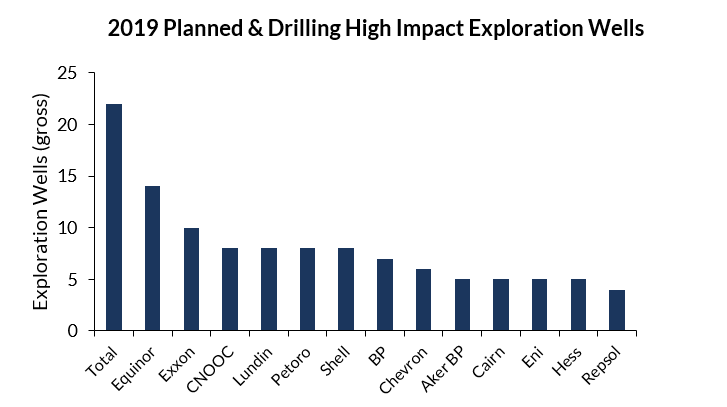

Conventional deepwater is fighting back, stimulated by exploration success, particularly in Guyana where over 5 billion barrels has been found since 2015 with breakeven oil prices in the $30s per barrel. It shouldn’t be underestimated the influence of Guyana on the exploration community, even though only Exxon, CNOOC and Hess are benefiting directly so far. The number of risky deepwater frontier wells increased from 6 in 2016 to 21 in 2018 though only 2 made commercial discoveries and both were in Guyana. In 2019 the company to watch is Total who is planning to drill by far the highest number of impact wells in 2019 at 22, of which 8 are frontier play tests. The regions to watch are NW Europe and Central and South America with 22 high impact wells each. Watch out for a new deepwater oil play emerging in 2019 as new play models are tested.

Figure 2: Number of high impact wells each company is participating in planned and drilling 2019

Source: Westwood Wildcat

An early stage recovery for the offshore oil field services but limited price inflation

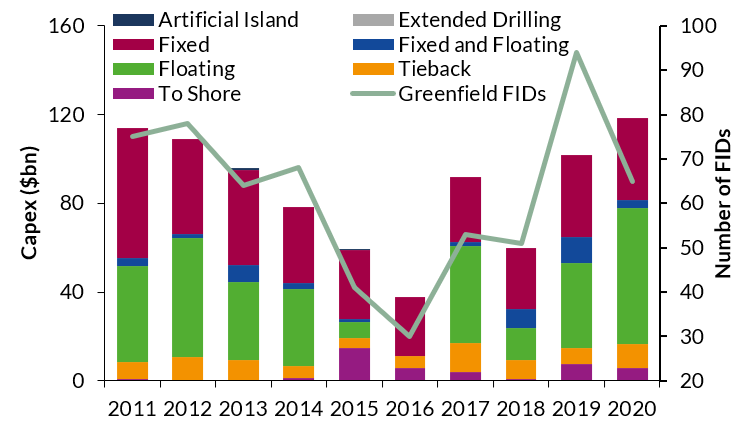

The 51 offshore project sanctions in 2018 was slightly down on 2017 but was still significantly up on 2015/16. Further progress is expected in 2019 with FIDs increasing significantly with up to 90 possible. This will bring some relief to the hard-pressed supply chain still struggling with overcapacity in most asset classes and many suppliers struggling with commercial terms. Expect to see increased contracting in 2019 but limited price inflation.

Figure 3: Sanctioned Capital Expenditure (Year of FID) by Development Type

Source: Westwood Sectors

Dr Keith Myers, President, Research

[email protected] or +44 (0)20 3794 5383