December 2025

November brought renewed policy momentum to the European hydrogen market, with steps taken to support the securing of reliable long-term offtake agreements. In this edition of Hydrogen Compass, we examine how the EU’s new Hydrogen Mechanism, strengthened low-carbon policy, and targeted fiscal measures in the UK signal a developing policy focus on revenue certainty and market acceleration. However, these advances come amid mixed signals on the ground. Developers are advancing new projects even while high-profile cancellations, such as BP’s H2Teesside project, highlight competition for land from other infrastructure, underscoring both the progress and fragility that has defined Europe’s hydrogen build-out.

The next edition will be published in January. In the meantime, if you have any comments or feedback, please do reach out to Jun Sasamura ([email protected]).

Policy and funding support continue across Europe

Policy supporting greater offtake certainty

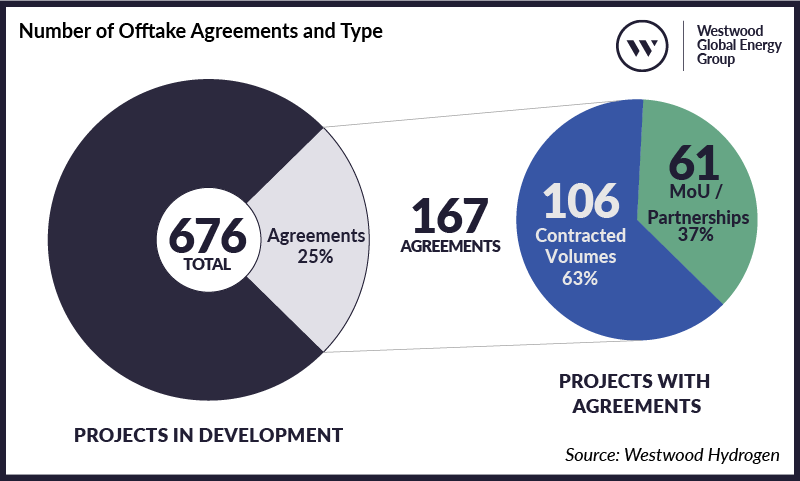

Policy developments in November provided meaningful steps toward addressing one of Europe’s most persistent barriers to scaling hydrogen: securing long-term offtake agreements. Without visibility on future revenues, project financing remains incredibly difficult, and today only 25% of announced projects in Europe[i] have a confirmed offtake agreement or MoU/partnership.

Number of Offtake Agreements and Type

Source: Westwood Hydrogen

Existing mechanisms, such as Germany’s H2Global, have begun to bridge the gap between producers and offtakers, and the EU has now moved to expand this support. The European Commission launched its first call for supply offers under the Hydrogen Mechanism, a matchmaking platform first introduced in July 2025 as part of the European Hydrogen Bank. This platform aims to connect producers of renewable and low-carbon hydrogen with credible EU-based offtakers, helping to convert early demand signals into bankable offtake agreements.

The initial call for interest is open until 2 January 2026, with anonymised summaries of supply offers to follow on 19 January. Running until 2029, the mechanism will also give participants access to financial instruments and support early-stage offtake agreements required for auction participation.

According to data from Westwood’s Hydrogen Projects solution, most offtake agreements are electrolytic (72%), while the remaining 28% are CCS-enabled. This dominance reflects both European regulatory emphasis on electrolysis to date and offtakers’ focus on renewable hydrogen to meet their decarbonisation goals.

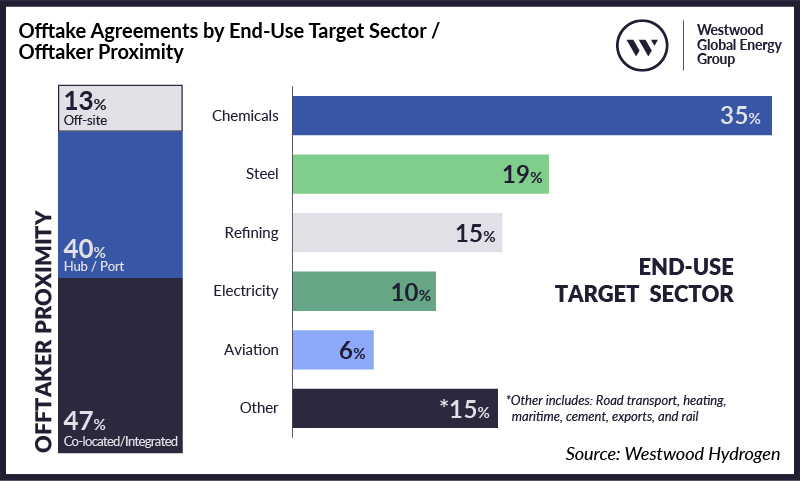

Offtake Agreements by End-Use Target Sector / Offtaker Proximity

Source: Westwood Hydrogen

When considering proximity, 47% of projects with offtake agreements are where supply and demand are co-located, demonstrating the benefits of leveraging existing processes and demand on the same industrial site. Another 40% are concentrated in hubs and ports, where shared infrastructure and proximity to multiple users support commercialisation.

Chemicals (35%), steel (19%) and refining (15%) are the largest offtake sectors, together making up over two-thirds of all agreements. This concentration shows that early renewable and low-carbon hydrogen adoption is occurring primarily in existing, hard-to-abate industrial use cases rather than new applications.

Additional policy and regulatory developments

The EU’s Delegated Act on low-carbon hydrogen became law in November, providing long-awaited clarity for CCS-enabled hydrogen and for grid- or nuclear-powered electrolysis that falls outside the Renewable Fuels of Non-Biological Origin (RFNBO) definition. The Act also extends low-carbon classification to ammonia, methanol, e-fuels, and other syngas-derived products. Taking effect on 11 December 2025, the legislation marks a pivotal moment for EU hydrogen policy, offering greater regulatory certainty for alternative production pathways and helping to address criticism that RFNBO rules alone are too restrictive to support market- scale-up.

The UK also introduced a practical measure to support hydrogen development last month. The Autumn Budget confirmed that electricity used for electrolytic hydrogen will be exempt from the Climate Change Levy (CCL) from spring 2026, pending parliamentary approval. With the levy set to rise to £8.01/MWh, the exemption removes a key cost disadvantage for electrolytic hydrogen relative to CCS-enabled production, whose natural gas feedstock is already exempt.

Project developments continue in November

Following an active October, developers further advanced hydrogen projects across Europe in November, with progress ranging from project commencements and FIDs to electrolyser installations and new project and contract announcements. However, this positivity was tempered by BP’s decision to withdraw its 1.2 GW CCS-enabled project due to land competition from a proposed large-scale data centre. The cancellation has introduced new uncertainty, highlighting the risk that hydrogen projects could face growing competition from other infrastructure developments, particularly as data centre expansion accelerates across Europe.

Key European Project Watch

Source: Westwood Hydrogen

[i] Westwood’s Hydrogen solution currently covers Belgium, France, Denmark, Germany, Ireland, Italy, the Netherlands, Norway, the UK, Spain, Portugal, Sweden and Finland.

Jun Sasamura, Manager – Hydrogen

[email protected]