January 2026

This special edition of Hydrogen Compass offers a focused outlook on the European hydrogen landscape for 2026. It examines the policy and funding signals to watch across the EU and UK, highlights the projects most likely to reach commissioning, and reflects on what 2025’s final investment decisions revealed about project bankability.

Navigating 2026: European hydrogen outlook

In 2026, the European hydrogen market is expected to face similar structural barriers that have slowed progress in recent years. The market remains selective, with offtake uncertainty remaining the primary constraint on investment and limited bankable demand available beyond a small number of industrial anchor projects.

Regulatory clarity is still incomplete, driven by delayed and uneven RED III implementation, evolving RFNBO interpretations, and uncertain implications of the EU Low-Carbon Delegated Act. Funding schemes continue to underpin momentum even if timelines and criteria are not perfectly aligned, yielding a selective pipeline entering 2026.

As highlighted in our Hydrogen Retrospective, 2025 showed progress is uneven and non-linear. FIDs continued, funding frameworks evolved and projects advanced, setting the context for a pragmatic, selective and opportunity-led 2026.

What to expect in 2026

2026 brings pivotal EU and UK hydrogen policy and funding signals. The following table summarises what we are awaiting and the potential impact we could see this year.

| Area | Milestone to Watch | What We Are Waiting For | Potential Impact |

| UK Policy | UK hydrogen strategy revision | Potential update to 10GW target, delivery priorities, and clarity on HAR3 and HAR4 | Greater visibility on long-term demand outlook and direction of UK supporting mechanisms |

| EU Policy | EU hydrogen strategy revisions (by year-end) | Potential revisions to RFNBO definitions and/or deployment targets | Improved regulatory alignment with market realities; reduced compliance risk for developers |

| EU Policy | EU Low-Carbon Delegated Act | Clarity on eligibility and role of low-carbon hydrogen | Expanded addressable market and increased flexibility for project developers |

| UK Funding | HAR 1 progress | Conversion of 11 projects (~125MW) and £2bn+ revenue support into FIDs and construction starts | Signals deliverability of UK support framework and near-term capacity build-out |

| UK Funding | HAR 2 | Progression of 27 shortlisted electrolytic projects to contract awards | Conformation of continued UK funding pipeline and competitive project selection |

| UK Funding | HAR 3 | Decision on launch timing and design | Indicates UK commitment to sustained hydrogen scale-up beyond early rounds |

| EU Funding | 3rd EHB auction | Allocation of €1.3bn including first time support for both RFNBO and non-RFNBO electrolytic hydrogen | Broadens eligibility, increases addressable project pipeline, and signals greater policy flexibility at EU Level |

| EU Funding | EU matchmaking mechanism | Effectiveness in pairing supply with demand | Potential reduction in offtake risk and acceleration of project development |

| German Funding | H2 Global | Deployment of ~ €3bn total budget through further contract award | Improved revenue certainty and bankability for supported projects |

| EU Funding | IPCEI | New approvals or follow-on funding rounds | Support for large-scale, integrated hydrogen value chains |

2026 Policy and Funding Watchpoints

Source: Westwood Hydrogen

Against this backdrop, Europe’s first wave of large-scale electrolytic hydrogen could materialise in 2026, led by a few government-backed projects.

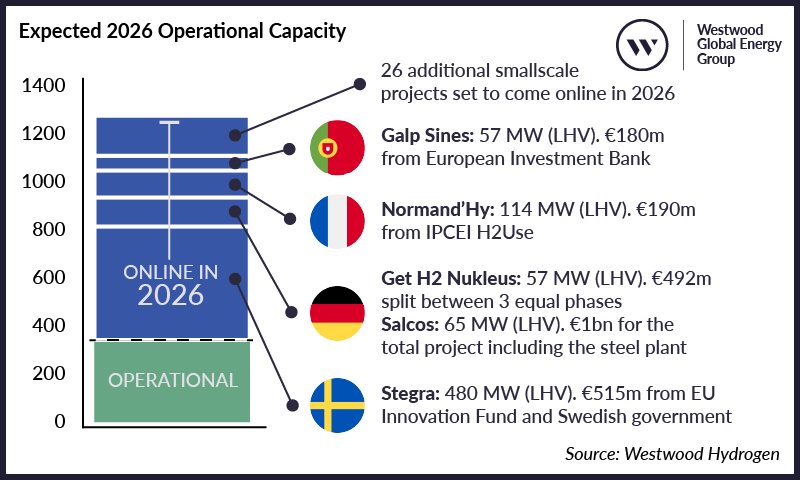

Projects expected to commission in 2026

Source: Westwood Hydrogen

By end-2025, Europe had 333 MW(LHV) of electrolytic hydrogen in operation. A further 943 MW has taken FID and targeting start‑up in 2026, which would lift operational capacity to 1.28 GW, a 283% jump and Europe’s first time above the gigawatt threshold. 2026 is when large‑scale projects should finally come to fruition.

This step‑change will be concentrated and policy‑led. Around 82% of 2026 additions come from five projects, collectively backed by €2.0–2.1bn in public support. While much of this funding also underwrites wider industrial transformation, it underscores the reality that Europe’s early scale will be delivered by a handful of capital‑intensive, subsidised flagship projects.

What 2025 FIDs can tell us

FID activity in 2025 provides a useful counterpoint to the scale due online in 2026. 13 hydrogen production projects passed FID, representing around 450 MW of electrolyser capacity. Only two exceeded 20 MW: Air Liquide’s 200 MW ELYgator in the Netherlands and Repsol’s 100 MW Cartagena in Spain. The remaining projects clustered in the 5–20 MW range, typically linked to local industrial, mobility or maritime demand.

Public support was central to these investment decisions, with at least nine of the 13 projects securing grants or state aid. Projects that progressed were also integrated directly with transport, storage or direct end-use, reducing offtake risk in the absence of mature hydrogen infrastructure.

Even as 2026 is expected to deliver the first GW-scale operational pipeline, new investment remains cautious and selective, favouring demand-secured, publicly supported projects.

Jun Sasamura, Manager – Hydrogen

[email protected]