Whilst explorers are used to the roller coaster ride of oscillating oil prices and the associated changes in investment levels, the period 2018-2022 covered by the 2023 State of Exploration report has seen the context in which the industry operates change significantly and frequently.

By the end of 2022 a degree of balance appeared to have been reached between the three vectors of the energy trilemma, referring to the balance between security, affordability and environmental sustainability. There is now a wider recognition among policy makers of the role that oil and gas production, and hence exploration, plays in the transition to a net zero economy.

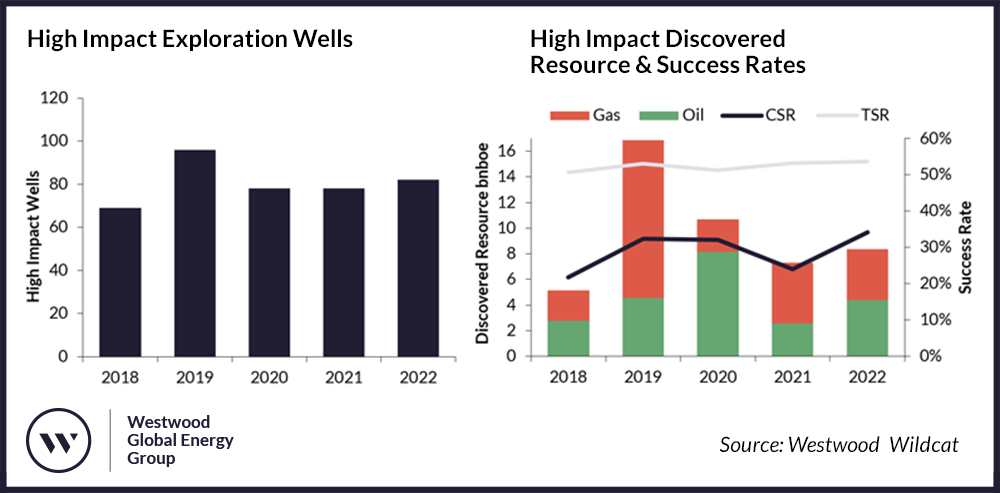

Historically, the level of high impact exploration drilling has correlated to the previous year’s oil price. This correlation shows signs of breaking. High impact exploration drilling in 2023 is expected to be broadly in-line with the previous year, rather than the ~50% increase the average oil price of ~$100/bbl in 2022 would have suggested. Exploration drilling continues but the focus is changing.

So, what are the key themes that have emerged from the last five years and what are the implications for the future State of Exploration?

Key Messages

- High impact exploration drilling levels were maintained in 2022 and performance improved, with discovered resource increasing 16% and commercial success rates increasing 10 percentage points to 34%. The improved success rates were driven by better emerging play performance, whilst the discovered resource was helped by large frontier discoveries in 2022.

- High impact exploration continues to be dominated by Supermajors and NOCs, with ExxonMobil, TotalEnergies, CNOOC, Equinor and Shell being the most active explorers 2018-2022. CNOOC and BP discovered the most resource at >3bnboe net, whilst CNOOC and Hess delivered the highest commercial success rate at >60%.

- The Venus discovery and opening of the Orange Basin coincides with a short term revival in frontier exploration, and frontier exploration commercial success rates were at record highs in 2022 reaching 25%. However, a fast follower strategy has generally not worked for emerging plays, with 90% of resource in plays opened since 2013 found by those in frontier acreage at the time of discovery.

- High impact oil and gas discoveries both take a median time of ~12 years from initial licence award to first production. 55% of the high impact oil resources and 40% of the high impact gas discovered since 2008 is in production or has been sanctioned for development whilst 18% of the oil and 48% of the gas discovered remains stalled, showing no signs of progression.

- Supermajor exploration acreage has almost halved from 2017 to 2022, with companies focusing in on core areas, new geology in proven basins and infrastructure led exploration.

- The industry is likely to keep exploring at current levels at least through to 2030 to sustain production and create portfolio options in the light of uncertain future demand, with short cycle, low cost, low emissions intensity barrels being particularly prized along with gas for European markets.

For more information on how to access The State of Exploration 2023 report, click here.