Westwood’s Offshore Drilling Rigs Senior Analyst, Teresa Wilkie on what to expect from a changing Northwest Europe market following a change in the demand supply balance.

Since the oil price crash in 2014, the global mobile offshore drilling unit (MODU) market has suffered through a rig demand collapse, which coupled with a vast oversupply of units resulted in dismal utilisation and dwindling day rates.

The Northwest Europe MODU market, especially off Norway, has shown recent signs of utilisation improvement, due to a more stable oil price, an uptick in development and exploration and appraisal (E&A) activity, as well as a substantial number of older rigs being permanently removed from the fleet. The combination of increasing demand and decreased supply has resulted in rising day rates, most notably in the 6th-generation Norwegian semisub market. New fixtures for rigs in that segment have improved to the point that rates are now among the highest in the world.

Although much of the rig demand for 2019 drilling campaigns in the region has already been secured, Westwood Intelligence (analysis of; RigLogix, Atlas and Sectors data) shows that there are 3,808 days of unfulfilled rig demand this year, i.e. where operators have drilling plans but no rig. There are currently 6,066 days of available rig time so this does not appear to be a problem, however, deficits in 2019 supply become apparent when it is broken down into individual sub-segments.

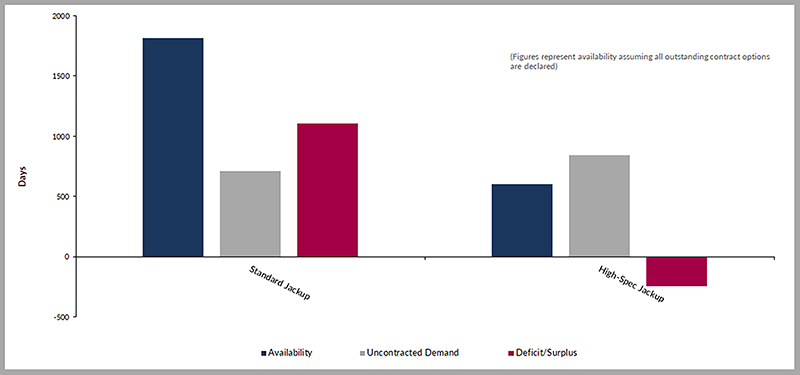

Figure 1: Remaining 2019 Northwest Europe Unawarded Jackup Supply Vs Availability.

Sources: Westwood RigLogix, Atlas, Sectors

Figure 1 shows that there appears to be plenty of standard jackup supply to cover the remaining 710 days of unfulfilled demand for the remainder of this year. The majority of this is plug and abandonment (P&A) work in the southern portion of the UK North Sea.

Uncontracted demand for the high-specification jackup segment totals 841 days which, when considering free rig time, leaves an undersupply of 241 rig days this year. As a result, operators that require a modern and more capable jackup may struggle to secure such a unit for work in 2019 as the market is considerably tighter. Remaining demand for high-specification jackups this year consists of both E&A and development drilling campaigns off the UK, Norway, Netherlands and Denmark.

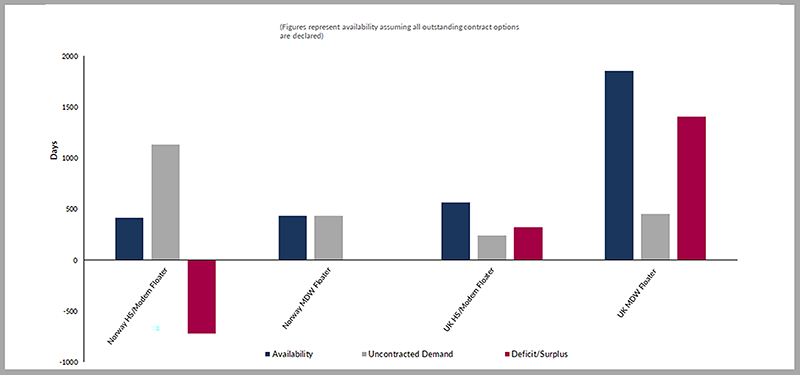

There are some clear similarities with the supply and demand balance for jackups and the region’s floating rig (semis and drillships) fleet. Figure 2 shows the Norwegian modern, high-specification floater segment will have the largest rig deficit in 2019, with a shortage of 719 days forecasted. The standard/mid-water fleet in Norway will also be extremely tight this year with supply and demand virtually equal. Supply of other modern, high-specification units typically used in the UK, will also tighten further, with only a handful of rigs showing free time this year. However, there is a surplus of standard UK mid-water units due to lower demand and a continued supply glut. The remainder of 2019 floating rig demand is mostly a combination of development and E&A drilling programmes offshore Norway and the UK.

Figure 2: Remaining 2019 Northwest Europe Unawarded Jackup Supply Vs Availability.

Sources: Westwood RigLogix, Atlas, Sectors

Operator preference for premium assets are now driving demand in Northwest Europe. Many oil companies want deeper rated, more modern rigs that provide winterization, greater drilling efficiencies and less downtime that will help reduce overall project costs.

Drilling contractors are aware of a looming undersupply of top-tier assets and are acting accordingly. Several have already successfully secured lucrative Northwest Europe contracts for units that had previously been located outside of the region, including newbuilds still in Asian shipyards. Other rig owners like Diamond Offshore have taken the reactivation route, bringing back older, cold-stacked rigs for mid-to-long-term campaigns in the area. More relocation into the area and further reactivations are likely, as operators look ‘outside the box’ to fulfil requirements.

Some additional attrition during the remainder of the year is anticipated but is unlikely to have much impact on overall availability or day rates. The rigs that are candidates for the scrap heap are older (typically over 35 years old) and less capable and have been stacked for some time. However, much of the future rig demand in this region is for more modern, higher-specification units, so the fate of these older rigs will have little influence on activity in the market.

Rig demand in the winter months generally influences utilisation in this region, but this seasonality factor is expected to be less in 2019. As rig availability during favoured spring and summer periods continues to disappear, operators will have little choice but to carry out work during harsher winter months. Jackup and floating rig utilisation will continue to creep up throughout the year, which will result in a further northward movement in day rates, especially in the undersupplied UK and Norwegian sectors.

For jackups, rates for standard units are expected to remain stifled by a continued supply surplus. However, owners of high-specification units will continue to test pricing as the gap between supply and demand is much narrower. Day rates for the Norwegian semi market are expected to continue to be fixed over US$300,000, while deepwater floaters in the UK sector will exceed US$200,000 from the recent range of US$120,000-US$160,000. This has been demonstrated by the recent contract signing for semi Transocean Leader, which was secured by Premier Oil UK at US$245,000 for a campaign beginning in early 2020.

MODU demand in Northwest Europe will undeniably exceed availability this year, however undersupply will be somewhat confined to the more modern and technically-capable segments of the market. Therefore, any operators that are lucky enough to secure time on a high-specification jackup or semi this year must expect to pay a premium for the privilege.