Introduction – Why Survey the S-92 Fleet?

Recent months have been a busy time for the offshore helicopter sector as the financial distress of helicopter owners and operators has weighed heavy on the minds of those in the business and kept industry commentators particularly busy. Autumn is also a hectic period for conferences, and amongst the discussions in panel sessions and coffee breaks, there is consensus that, whilst E&P companies have seen a return to profitability, there is a fundamental problem in the industry of over-supply. However, when looking at the Large segment (which, based on MTOW, is typically defined as including the S-61, S-92, H215/225, Mi8), there seems to be little consensus on exactly what can be done about it, or, indeed, just how over-supplied it is.

“One of my contacts told me there are over 100 idle S-92s… I think that’s impossible” – Helicopter Leasing Executive

“All we need to do is scrap the rotorcraft that are over 15 years old” – E&P Company

“We think the market is very close to balance”– Leading Global Helicopter Operator

It is a little perplexing that the variety of views on this subject is so wide… or perhaps it isn’t, as whilst finding the data isn’t impossible most parties have ‘skin in the game’, one way or the other. The helicopter operators and leasing companies are owners of these units and have an incentive to not talk down the market and talk down the value of their assets at the same time. On the other side, helicopter manufacturers have invested vast sums of money and many years of effort in designing, building and certifying the next generation of aircraft, including the ‘super-medium’ units from Leonardo, Airbus and Bell. The narrative from these companies is that the super-medium rotorcraft can perform most of the duties of a heavy helicopter at lower acquisition and running costs, with the latest standards in safety, comfort and efficiency. Most aviation data providers are aviation focused (not pure-play oil and gas), covering tens of thousands of rotorcraft and billions of fixed wing passenger journeys so keeping a close and accurate tab on offshore S-92s can hardly be expected.

Our Approach

The basic questions are therefore:

- Is the market over-supplied? How many S-92s are actually flying regularly on offshore personnel transfer journeys?

- Are there measures that would bring the market back into equilibrium? Are these required, or will the market correct itself?

The above questions seemed to us at Westwood to be questions that were worth answering… we have a very detailed demand model that forms the basis of our annual World Offshore Helicopter Market Report, where we model activity ‘bottom-up’ from a platform by platform, rig by rig, approach. On the supply side, we have access to several data sources that can be interrogated to understand the actual nature of what is happening in terms of helicopter utilisation.

The approach, therefore, was to work one-by-one through the fleet list of heavy rotorcraft (we used FlightGlobal for the purpose of identifying the units) and examine recent usage (FlightRadar and FlightAware data were examined for each unit) and then set this against the Westwood demand-side data.

None of the data-sets were 100% consistent, as you might expect when examining a very small subset of a rotorcraft population of over seventy thousand. There were examples of helicopters listed as stored in one dataset that it transpired were flying regularly, and vice versa with supposedly active units stored in locations such as Poland.

Consequently, we cross-referenced this data by reaching out to key helicopter operators/owners to verify and sense-check any unclear areas of the data. Our findings were also shared with Sikorsky, which tracks utilisation of each unit, for comment. We are grateful for the support and input we received from the Sikorsky and the major S-92 operators.

(Further potential limitations of the analysis are set out as a footnote to this article.)

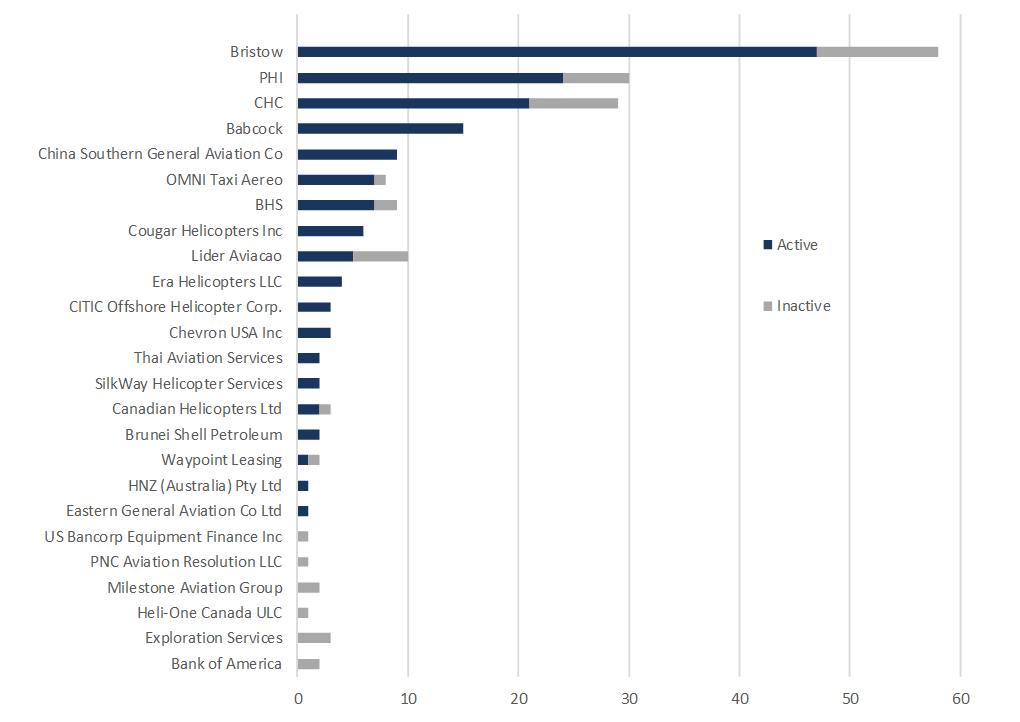

Utilisation of the S92 Fleet is Currently 78%

Having reviewed 209 offshore S92 units we concluded that 162 have flown in December up to the point in time of this analysis (i.e. between 1st and 18th December). This gives a utilisation figure of 78%. The leading operators are Bristow, PHI and CHC. Based on the available data, we note that Bristow have the highest number of inactive units. It is expected, however, that Bristow will return some of these units to lessors, and Bristow report that “We intend to further reduce aircraft rent expense through lease returns” in the Form 10-Q posted on 9th November 2018.

Figure 1: Active S-92 by Operator (Grouped)

Source: Westwood Global Energy Analysis

Operators commented that overall S-92 utilisation has been robust, despite the oil industry downturn, which is function of the performance of the unit and particularly so as the only real alternative to the H225 units, many of which have not returned to the market since 2016.

“The S-92 is a superb helicopter, it meets all of our most-demanding requirements and is a very reliable and proven machine” – Leading Global Helicopter Operator

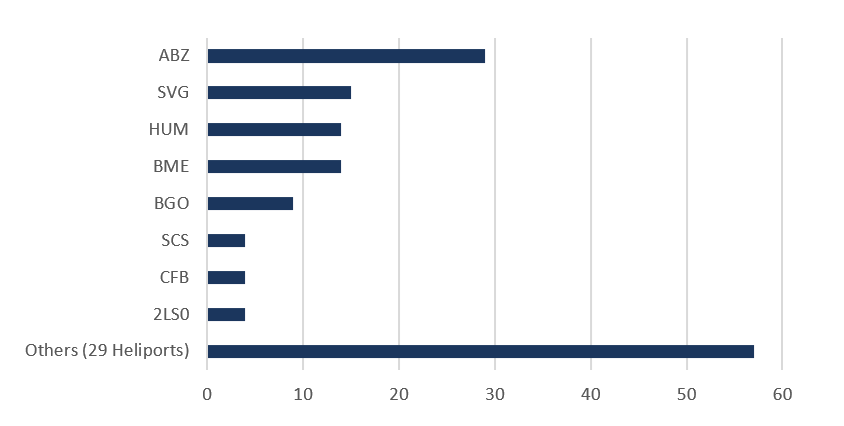

Aberdeen Is the Busiest Heliport in the World for S-92 Operations

A total of 5,335 S-92 flights were identified. To avoid any ambiguity, a ‘flight’ is defined as a take-off followed by a landing, so a journey from a heliport to land on a helideck at a platform and then fly back to the heliport would count as two flights.

As of the 18th December, nearly a fifth (19.3%) of the active fleet were working from Aberdeen (ABZ). Stavanger (SVG) accounts for 10% and Houma-Terrebonne (HUM) in Louisiana, USA and Broome International in Australia each account for a further 9%.

Figure 2: Active S-92s by Location as of 18th December 2018

Source: Westwood Global Energy Analysis

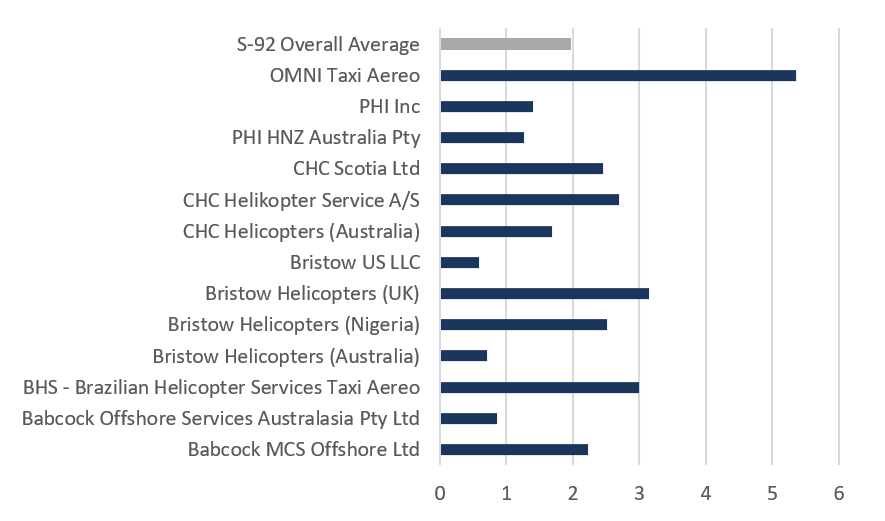

Some S-92s Are Being Used Very Intensively

We have heard anecdotally in the market that a smaller number of aircraft are being used but worked harder. We do not have a historic reference point to compare to, however, it is evident, particularly in Brazil and the North Sea, that some units are being used very intensively with some recording over 100 flights over the 18-day period. Averages for selected companies are shown below. The 150 active S-92s completing 5335 flights over the 18-day period equate to an average of two flights per day (note that twelve units are identified as flying but without specific data on individual flights.) Data provided by Sikorsky show overall offshore flying hours for the S-92 increased by 7.5% in 2018 to reach over 154,000 hours flown.

Figure 3: Average S-92 Flights per Active Aircraft per Day (1st– 18th Dec 2018)

Source: Westwood Global Energy Analysis

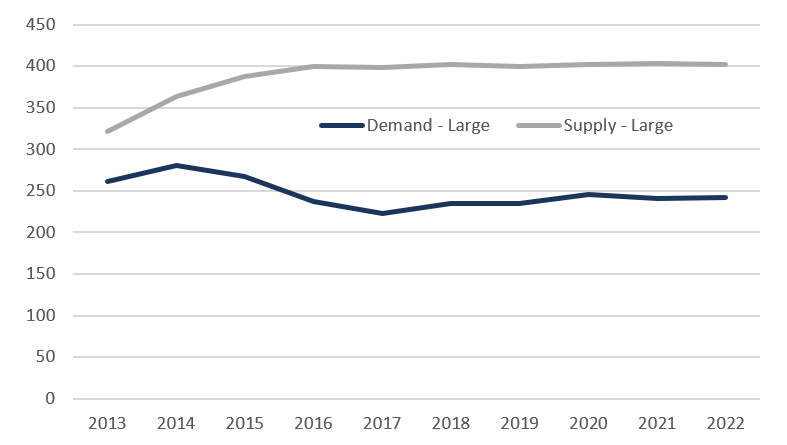

The Global Supply / Demand Balance Picture

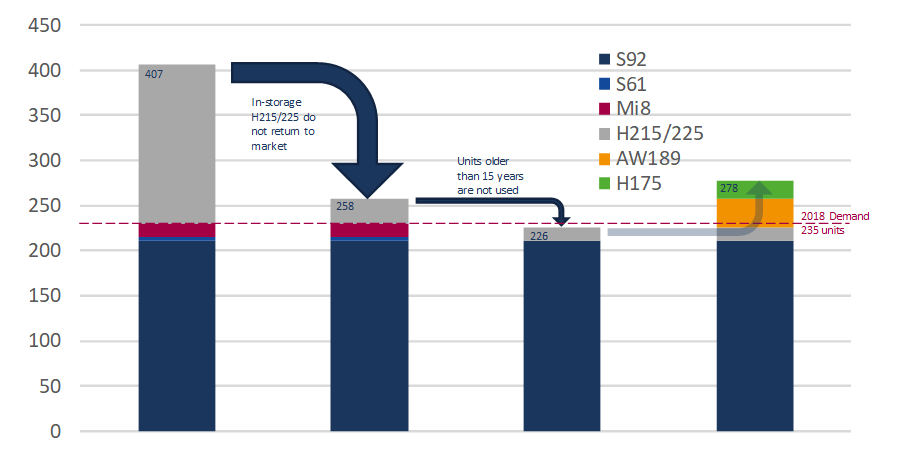

Defining the overall large market as H215/225, S-92, S-61 and MI8 aircraft, there are, according to FlightGlobal a total of 407 rotorcraft in the offshore fleet. The Westwood demand model puts large helicopter requirements at 235 in 2018, giving an implied utilisation of 59%.

Figure 4: Large Helicopter Supply / Demand

Source: World Offshore Helicopter Market Forecast 2019-2023, Westwood Global Energy

Examining the supply-side in more detail, it is possible to see how the market can reach equilibrium, based on the historic definition of the Large segment:

Figure 5: Large Helicopter Supply Reduction Scenarios

Source: Westwood Global Energy Analysis, FlightGlobal Fleet Data

We note that removal of out-of-service H215/225 and removal of older units (it is understood that none of the Mi8 or S62 are active on crew change duties in any case) brings the effective supply down to 226 units (vs a modelled demand of 235 units) and would require full utilisation of the S-92 fleet. However, some of the newer ‘Super Medium’ aircraft such as the AW189 and H175 are likely to find roles in missions that were previously serviced by large helicopters. This could take the supply to as many as 278 units.

Conclusions

– S-92s remain a favoured helicopter in the market with operators highlighting the versatility and reliability of the unit as the key strengths.

– Despite the oil industry downturn, the utilisation of the S-92 offshore fleet is currently 77% based on a survey of the fleet completed 1st December

– 18th December 2018. A total of 47 units in the ‘active fleet’ had not flown over this period.

– 25 of the S-92s owned by the top three operators appear not to have flown in the period analysed. Whilst some may be offline for maintenance or in place for backup purposes, the assertion by the likes of Bristow (in addition to the rumours in the market) that there are further units to be passed back to lessors appears to be supported by the data for all three of the leading helicopter operators.

– Sikorsky data show increased total flying hours for the S-92 in 2018 – up 7.5% on 2017. This (combined with the data from our analysis) is in line with the speculation in the industry that the operational fleet is being flown harder, rather than re-activating out-of-service units.

– Overall utilisation in the Large Helicopter segment is seemingly low at 59%, however, it is not thought likely that the out-of-service Super Puma units will return to service and furthermore the Mi8 units and S-61 are not considered to be competitive with the S-92 or super-medium units. (We note that some Super Puma units are in-service and currently working in Brazil and Asia.) If none of the out-of-service Super Puma units return AND only units under 15 years old are used, then the market returns to equilibrium.

– However, some of the newer ‘Super-Medium’ units coming into the market are likely to pick up work that was previously being performed by S-92 and H225 units and this presents a risk of a material growth in the effective supply. Given that these units are very new into the market, it is not yet clear the impact they will have on the demand for S-92s.

Footnotes

The analysis covers a limited time span – are there seasonal factors at play?

Yes, particularly in the North Sea where installation and drilling activity is likely to be higher in the summer months than it is during December.

Is the overall supply definitely 209 units in crew transfer or could other factors skew the total?

The approach was to start with the FlightGlobal designation for the units and then correct when other data was available. A number of units listed as crew transfer subsequently transpired to be SAR units. We also understand that a number of Norwegian units are dual purpose SAR/crew transfer. In this analysis the total for the S-92 crew change fleet was within 5% of value provided by Sikorsky therefore the potential error it is not considered likely to be material to the analysis.

Surely some of the units not flying are in maintenance or serve as backup?

Yes. Helicopter operators were reluctant to confirm which of the non-flying units were in storage or in maintenance on a unit-by-unit basis. At least 24 units are understood to be stored however and furthermore there are units that are technically in-service but are awaiting to be returned to lessors. The units awaiting return have to be returned in a pre-agreed condition which will include repainting and maintenance – some operators may not be in a position to carry out this work at the present time.

Steve Robertson, Director, Head of Oilfield Services

[email protected] or +44 (0)1795 594734

Steve will be presenting at Helicopter Investor, London at 2.40pm on Thursday 31st January

S-92 Image, Ned Dawson.

Sikorsky, a Lockheed Martin company, delivered its 300th production S-92® helicopter to Era Group Inc. at the 2018 Helicopter Association International Heli-Expo.